Coronavirus is material for Australia, with Chinese exports worth 8.8% of GDP

The coronavirus outbreak has seen UBS downgrade its global GDP outlook. Indeed, among the most (indirectly) exposed economies are Australia & NZ, given China is by far their largest trading partner. Australian exports to China have grown significantly, by ~20% y/y for decades. In 2003 when SARS hit, export values were only $11bn, or 7% share of total exports, worth just 1% of annual GDP. But in 2019, exports to China hit a record ~$175bn, or ~35% share of total exports, worth ~8.8% of GDP. This is far above most other major economies at a 1-3% share of GDP.

UBS expects ~30% drop in services exports to China; Q1 GDP now -0.1% q/q

Across a few months during SARS in 2003, total Australian exports values (to all countries) fell ~13%, with services -8%, & a likely larger fall for exports to China (albeit perhaps partly also dragged down by the Iraq war). Indeed, the number of total visitor arrivals (from all countries) dropped by 16% in just 3 months to mid-2003; while arrivals from China collapsed by 38%. UBS China’s economics team expects a 30% slump in China’s total outbound travel in 2020, with the Q1 contraction more severe. So a 30% fall for Australian services exports to China wipes $6bn from GDP, or 0.9% off annual growth, a plausible downside risk scenario. Given Australian q/q GDP has been rising by only ~$2½bn q/q, we now think Q1 GDP growth is likely to be negative, even with arguably still optimistic assumptions. 1) We assume a decline in total exports in Q1 of 2% q/q, driven by a ~30% q/q slump in Chinese services exports, with little decline elsewhere. 2) We allow for some offsetting boost to GDP in Q2 from ‘deferred’ arrivals lifting growth, albeit this is relatively small given most services are ‘lost activity’: you don’t take two holidays to make up for a cancelled one; and many of the 134k Chinese temporary students who miss the start of semester may not return in Q2. 3) We also include some offset from lower imports as Australians substitute overseas for domestic holidays, but there will still likely also be a hit to domestic demand as virus fears simply lead Australians to go out less than otherwise. 4) We assume no negative hit to Australian goods exports to China (or any country), or other supply disruptions.

UBS downgrades Q1 GDP (again) to -0.1% & 1.5% y/y; still downside risk

Overall, we downgrade our Q1 GDP forecast (again) to -0.1% q/q & 1.5% y/y (was 0.2%, 1.8%), the weakest since the GFC. Given the impact of coronavirus is worse than SARS, we still have downside risk & Q1 could be ~-0.5% q/q. We also cut 2020E to 1.7% y/y (was 1.9%), probably below consensus; with 2021E unrevised at 2.5%. Our Q4-20 forecast of 1.9% is far below the RBA’s rebound to 2.7% (& 3% in 2021).

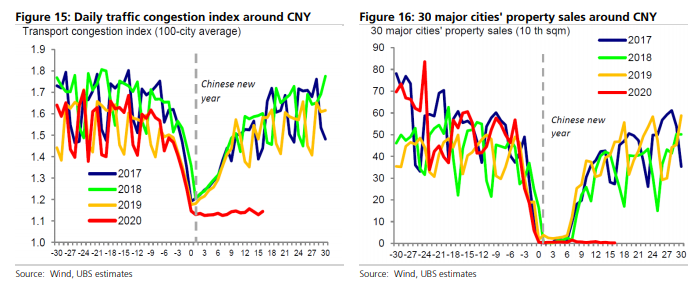

Some sanity at last. The danger is that the hit to Chinese steel implicit in those real estate numbers is material enough that a terms of trade shock lands in Q2 as well setting us up for two quarters of negative growth.

That is, recession.

Meanwhile, iron ore and the Australian dollar run higher…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.