DXY is booming again as EUR crashes:

The Australian dollar is strong but DXY saved its blushes:

Gold is hanging but must at risk as DXY rampages:

Oil caught a bid:

And metals:

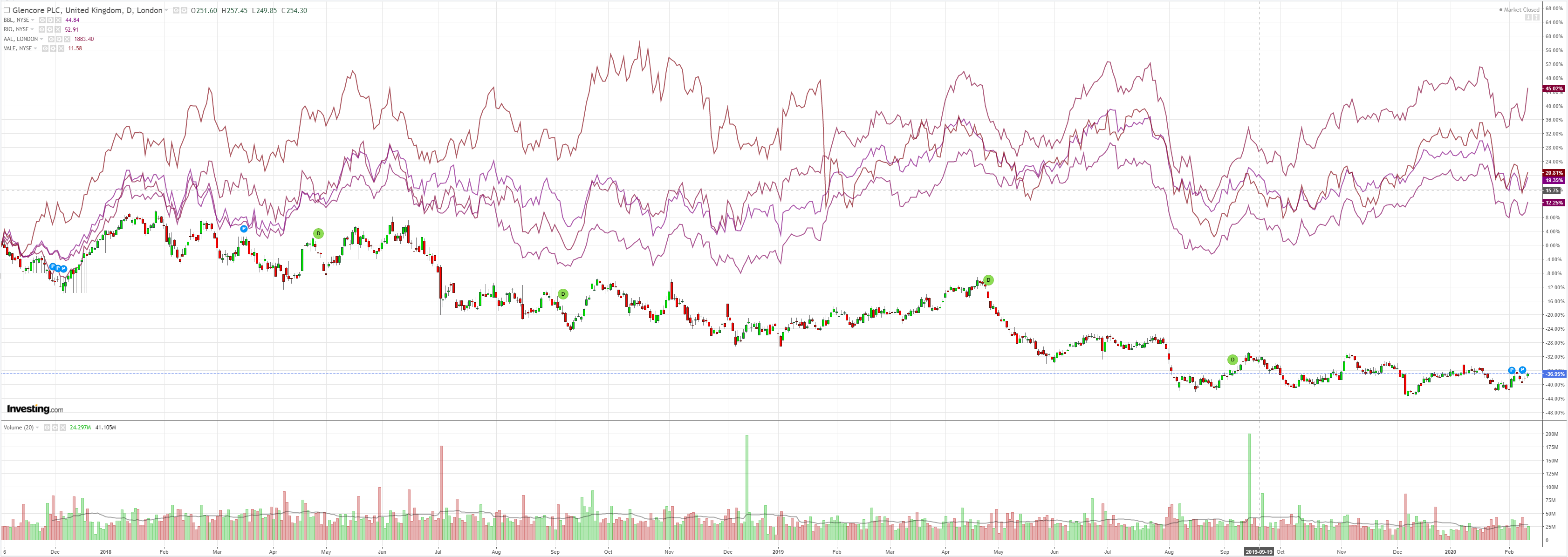

Plus miners:

And EM stocks:

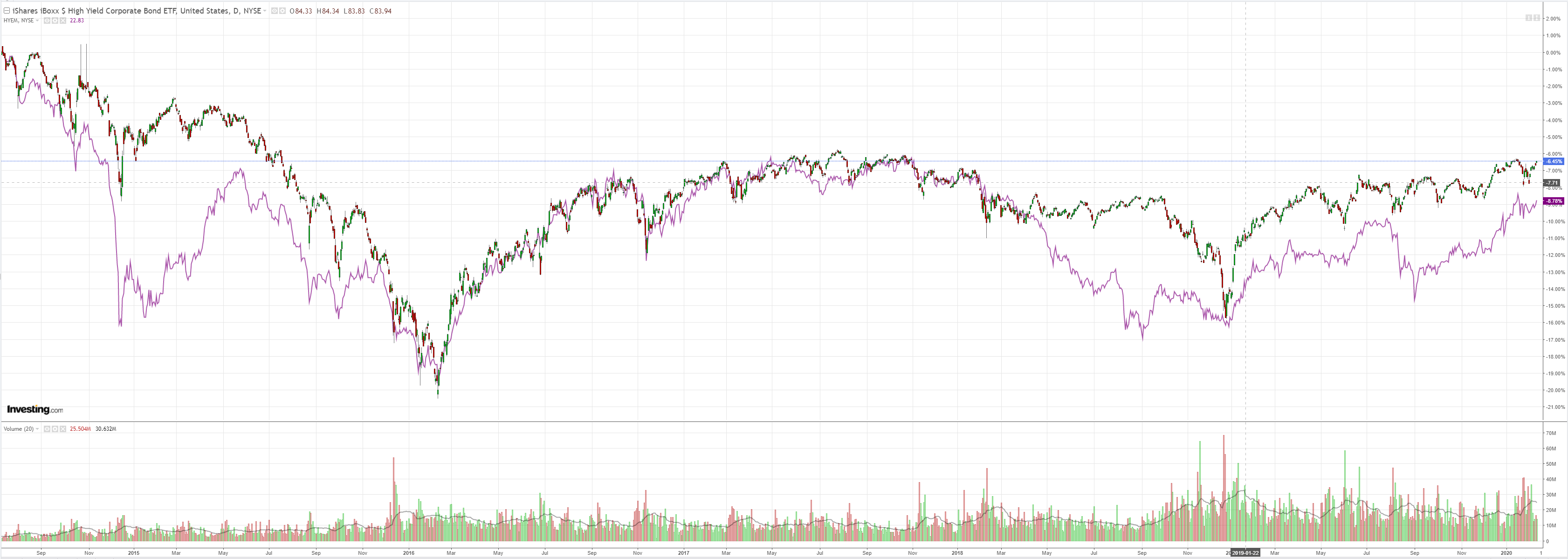

Having discounted zero, junk is off and running:

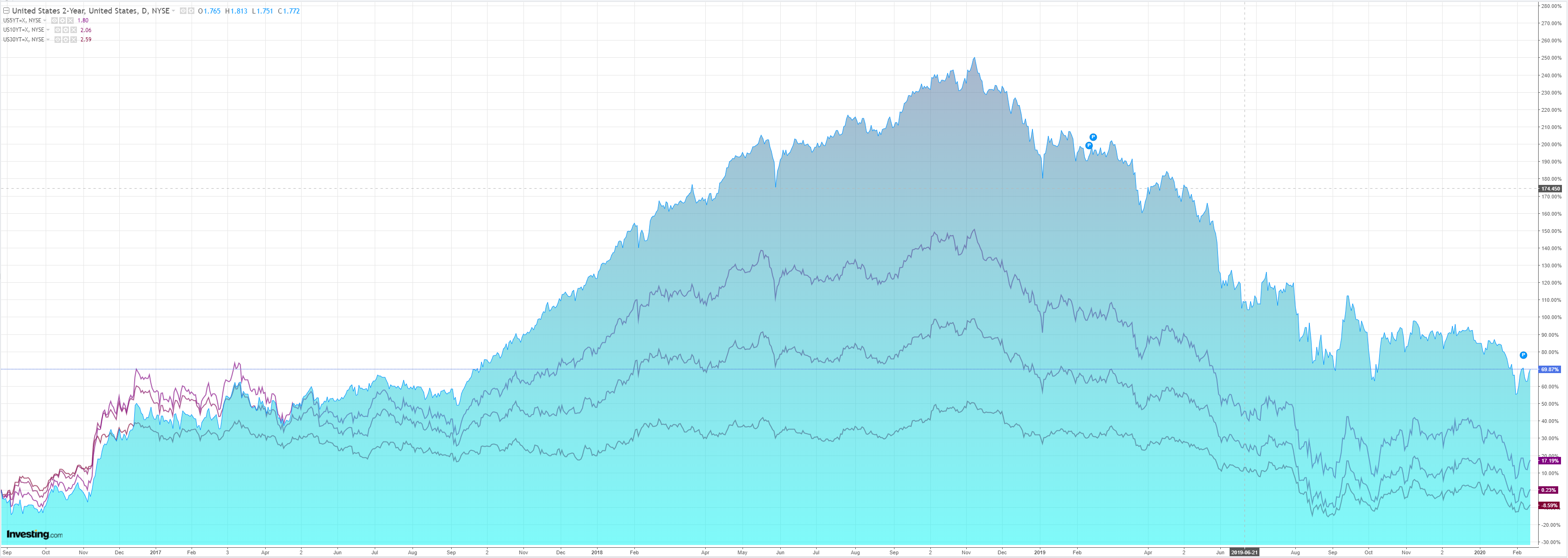

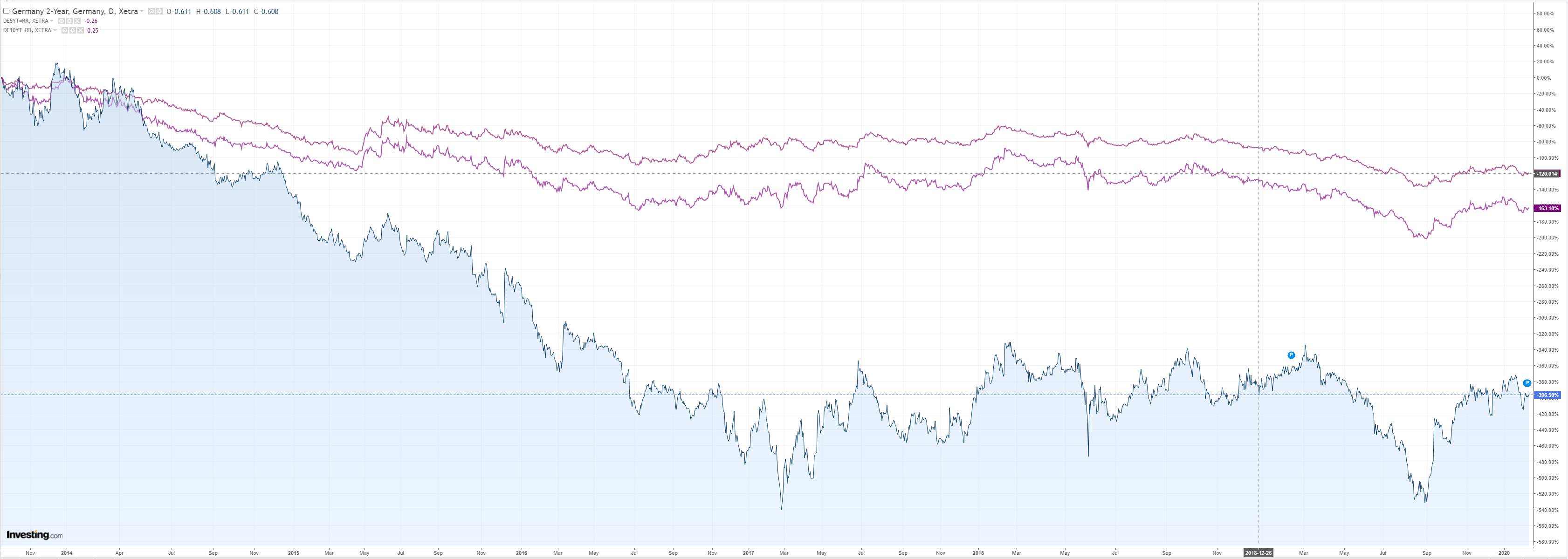

Bonds were bashed:

Stocks euphoric:

Westpac has the data wrap:

Event Wrap

Eurozone Jan. industrial production reflected the weakness in national releases, contracting 2.1%m/m (est. -2.0%m/m), with the annual rate well below expectations at -4.1%y/y (est. -2.5%y/y).

Event Outlook

RBNZ Governor Orr will speak to the Parliament Select Committee this morning following yesterday’s release of the February MPS.

RBA Governor Lowe will be on a panel at the Australia–Canada Economic Leadership forum, 11:15am AEDT.

US CPI inflation is expected to remain above 2.0% on an annualised basis. The headline rate is expected to lift, but the core rate should remain around 2.3%yr.

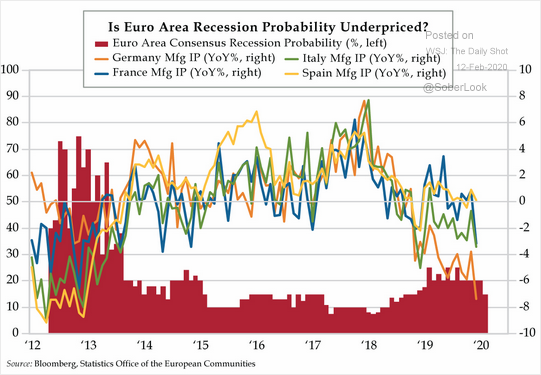

And Europe will only get worse as the virus shock lands on its export model risking outright recesssion:

As the US consumer parties on:

Driven by solid wage growth and cheap energy:

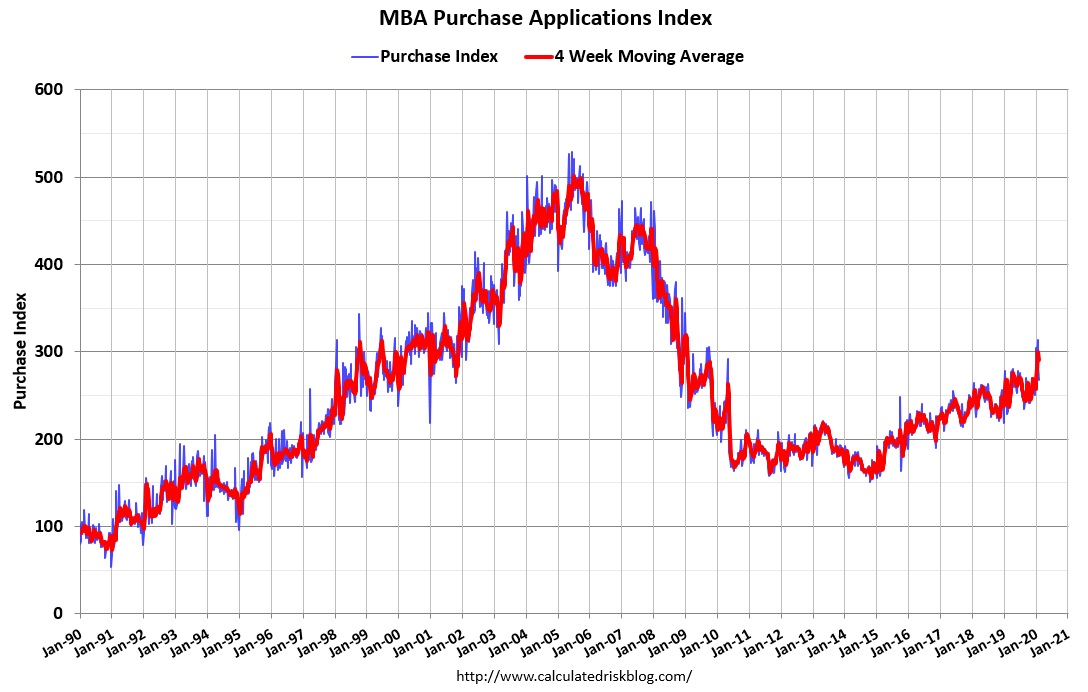

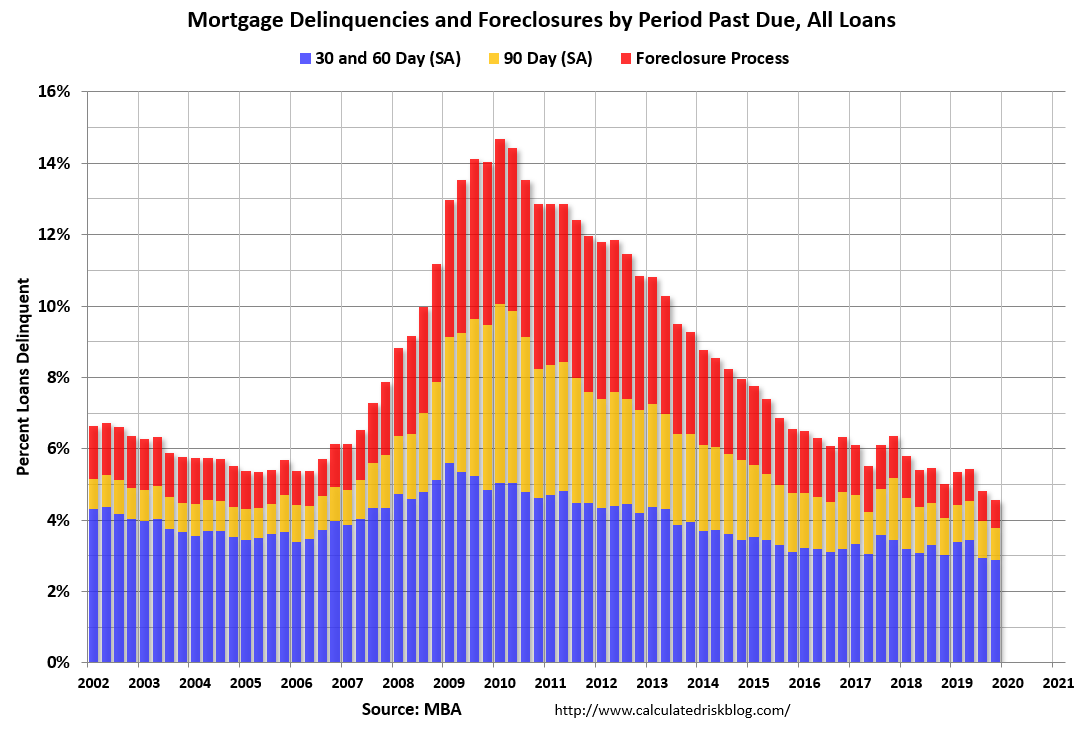

Cheap mortgages:

Booming houses:

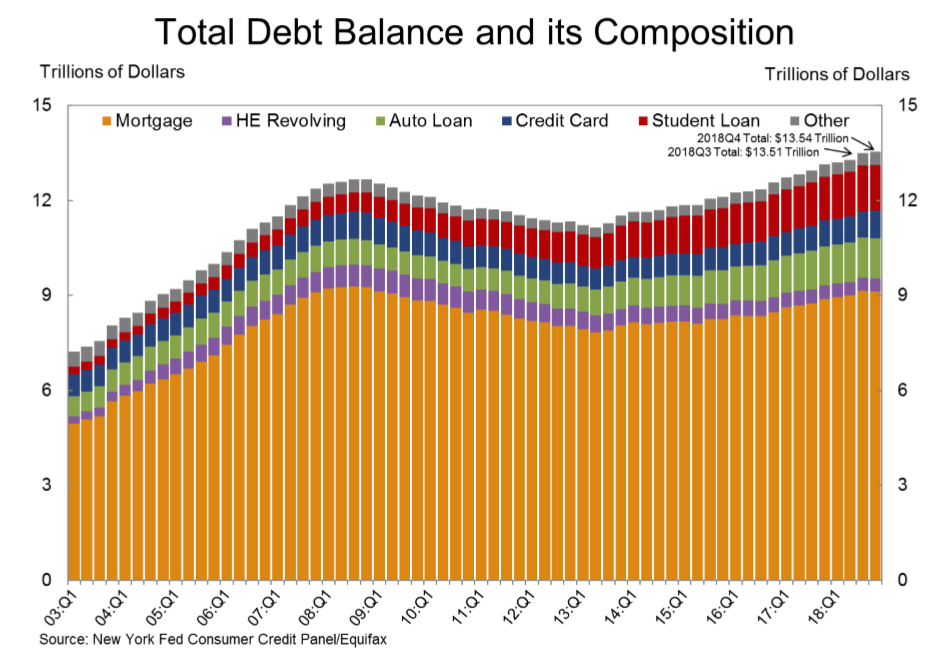

And releveraging:

The US consumer is in rude health.

We can be thankful that the runaway USD will cap the AUD as the RBA dithers.