DXY has broken out and has the ears pinned back as EUR tumbles:

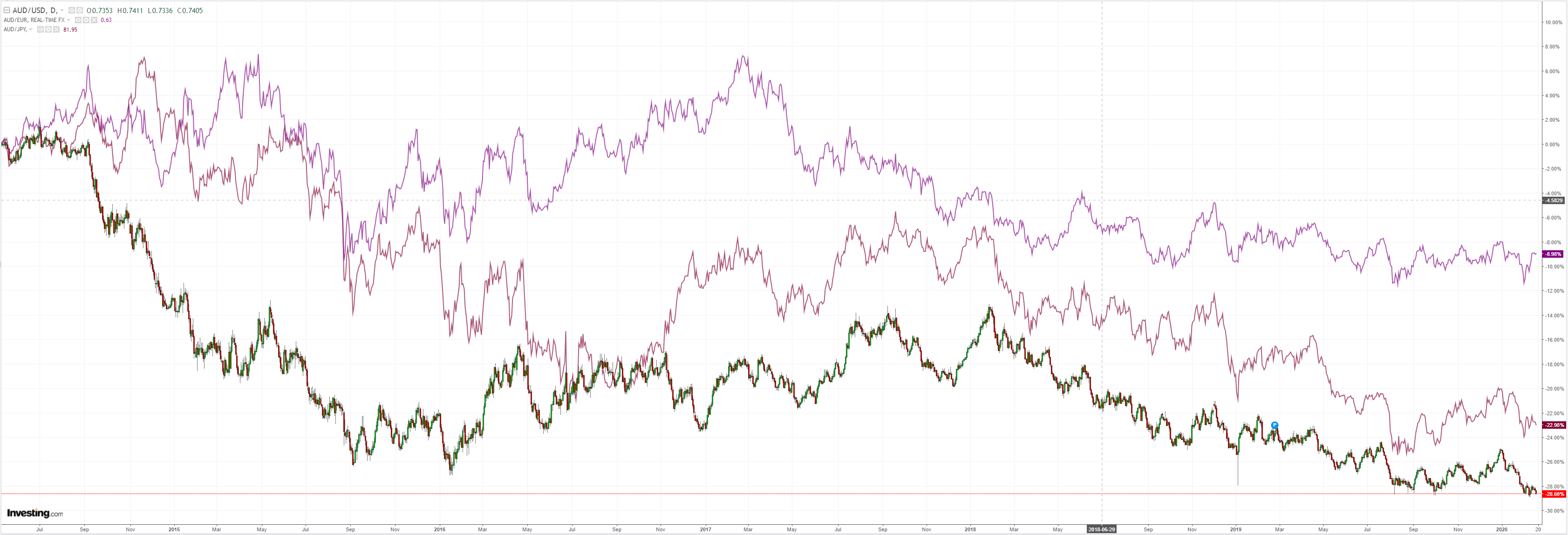

The Australian dollar held on at the brink again. It has a horribly bearish descending triangle chart but its benefitting from “buy the dip” a la US stocks:

Advertisement

EM forex was even weaker:

Remarkably, gold is runnig hand-in-hand with DXY:

Oil is still trying but is literallly sloshing all over the floor:

Advertisement

Metals were hit:

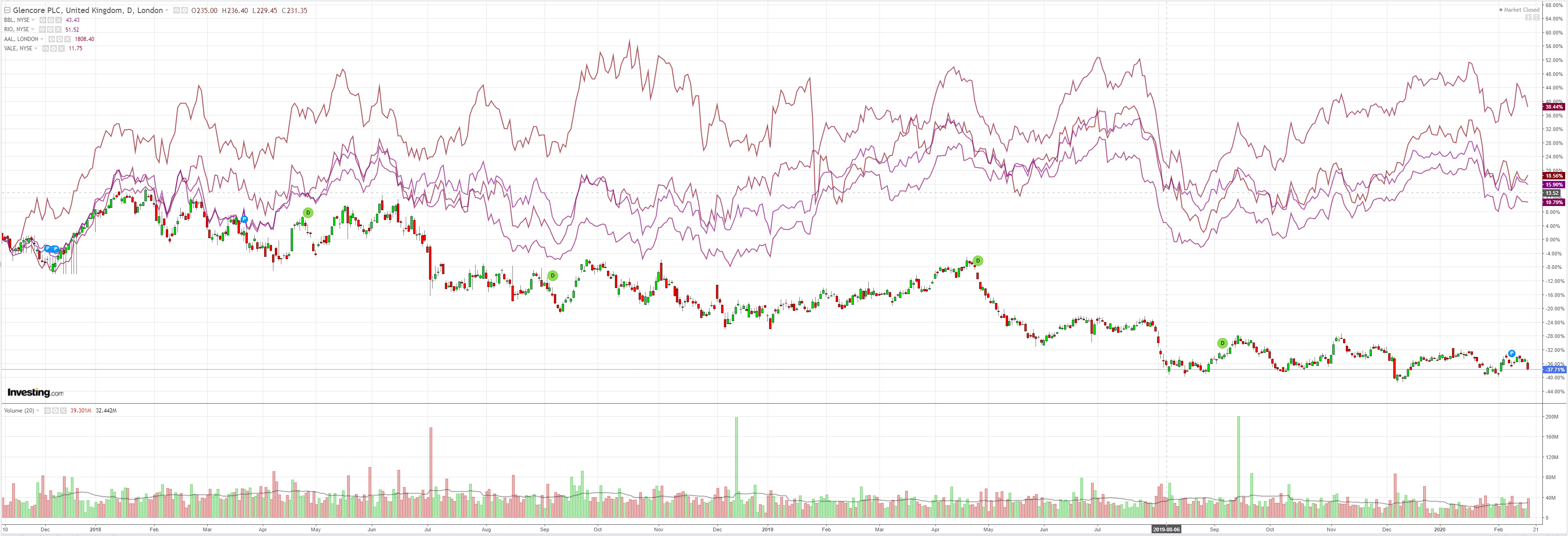

Miners fell:

Advertisement

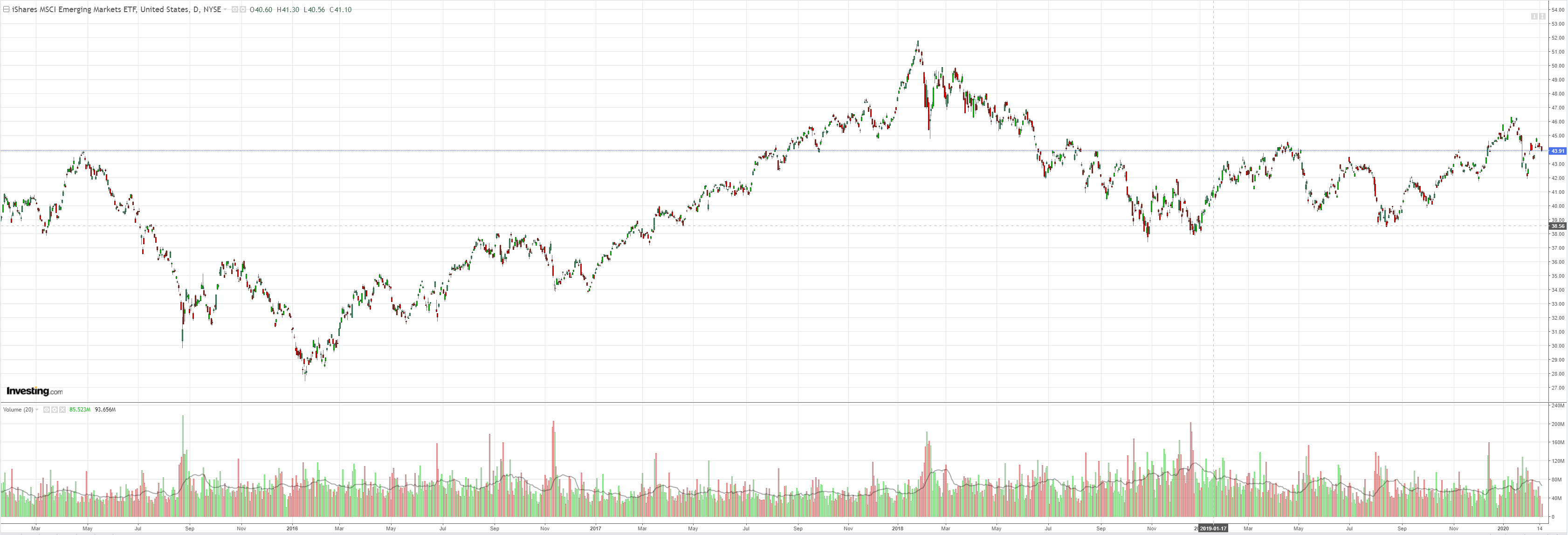

EM stocks too:

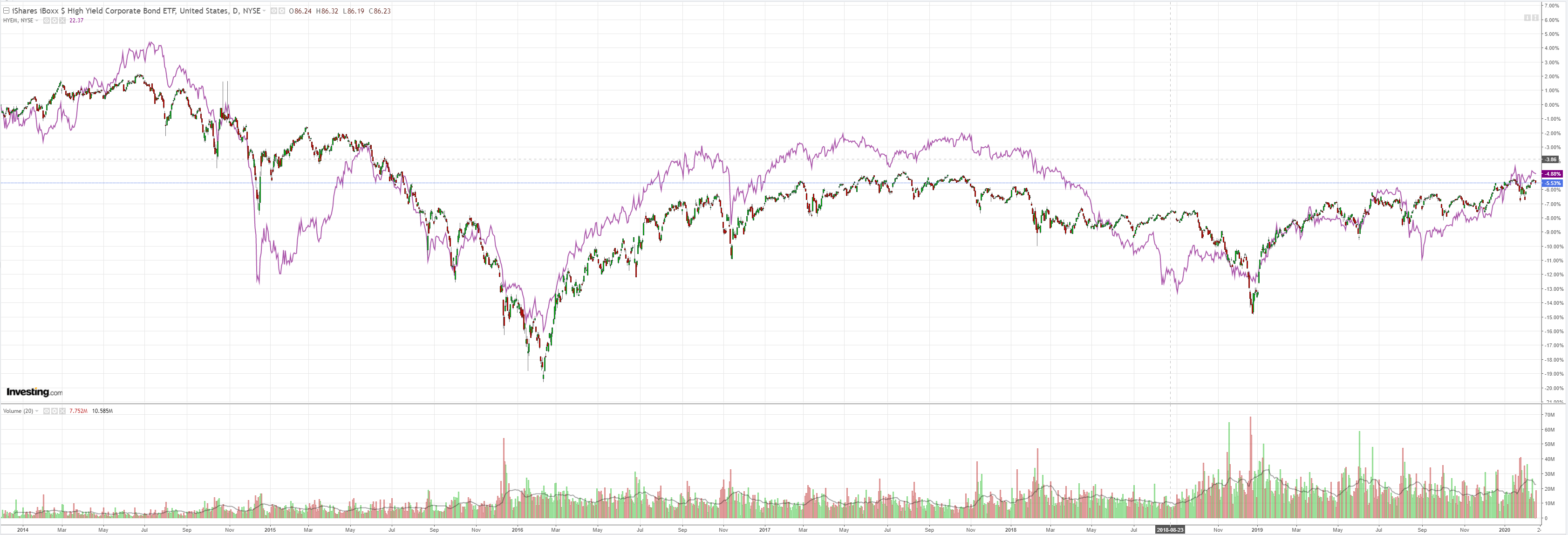

And junk:

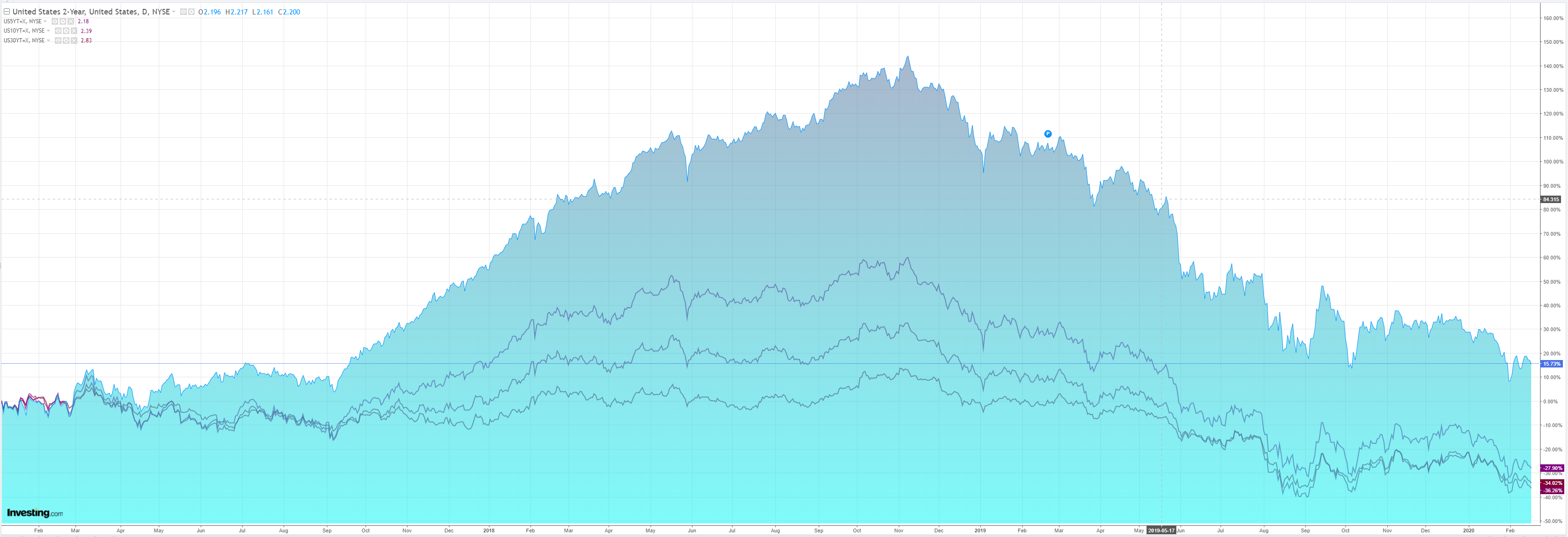

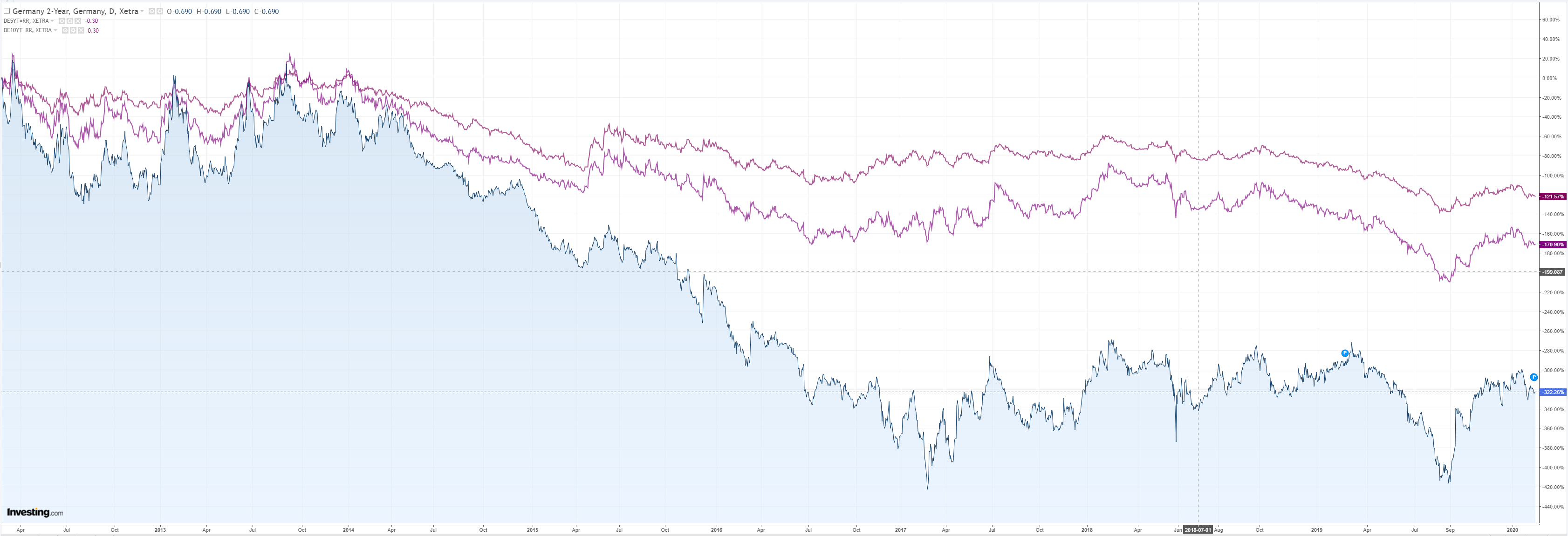

Bonds were bid:

Advertisement

And, lo, stocks bought the dip:

Westpac has the wrap:

Event Wrap

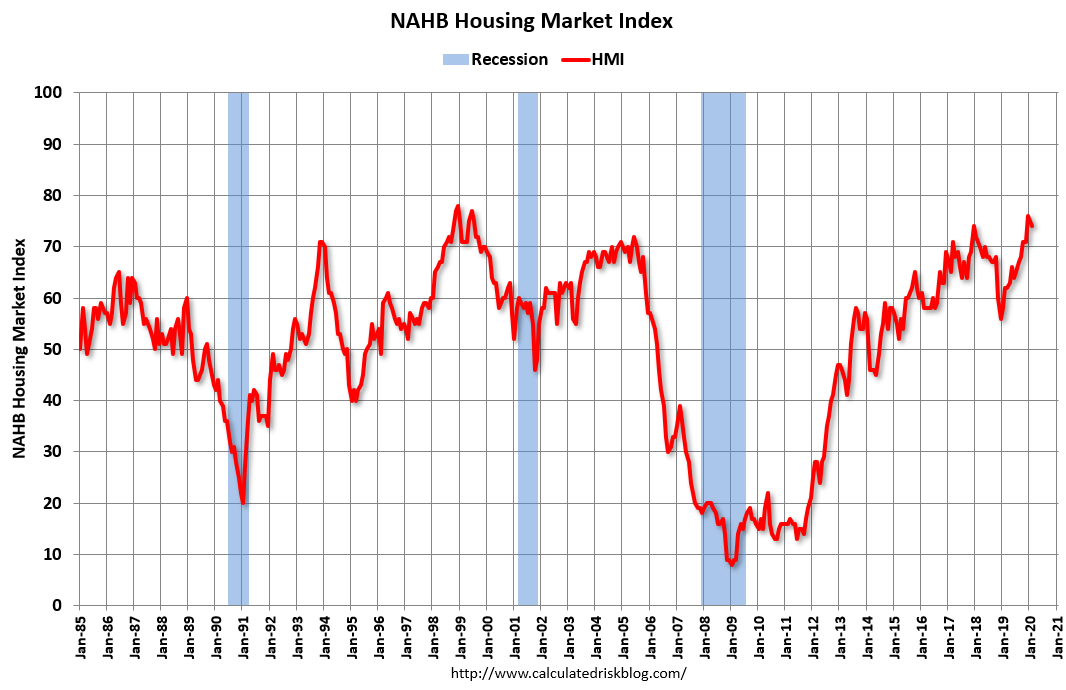

The NY Federal Reserve’s Empire State survey rose sharply from 4.8 to 12.9 (vs 5.0 expected). ISM-adjusted, it’s at a 15-month high. The survey likely captures the phase-one US-China trade deal plus fall in Brexit uncertainty, but is yet to capture the coronavirus pandemic impact. NAHB homebuilder sentiment slipped from 75 to 74 (vs 75 expected), still near a multi-year high. Low mortgage rates and a strong labour markets have supported the housing market.

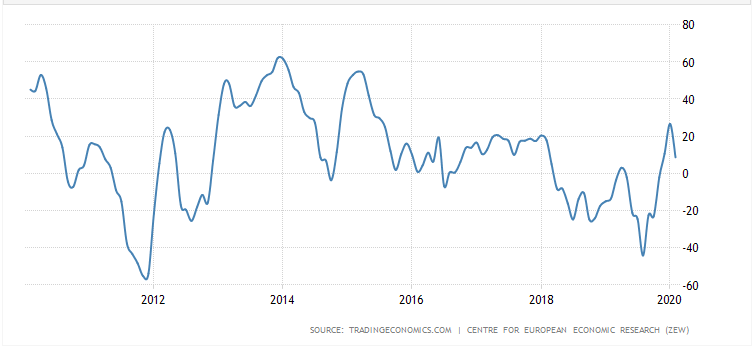

German ZEW economic confidence survey fell from 26.7 to 8.7, optimists continuing to outnumber pessimists, although the report does suggest a weak Q1 GDP outturn.

Last night’s GlobalDairyTrade auction saw prices for most products fall, the headline index down 2.9%. Our key export product – whole milk powder – fell 2.6%, matching yesterday’s futures market predictions of a 3% fall. At US$2966, it is at the bottom of past 12-month range of $2966-$3330.

Event Outlook

Australia: Another sub-par wage priceindex print is expected in Q4, with Australian wages forecast to rise 0.5%, 2.2%yr. The January Westpac-MI leading index is also due to be released. In December, the index rose from -0.62% to -0.32%, pointing to sub-trend growth in early 2020.

In the US, housing starts and permits will be followed by the FOMC’s January meeting minutes. Discussion of the risks to the growth and inflation will be the focus for the market. Bostic, Mester, Kashkari and Kaplan also due to speak.

It was all about growth divergence again. With the US leading thanks ot the Richmond Fed and tearaway building confidence:

Advertisement

Builder confidence in the market for newly-built single-family homes edged one point lower to 74 in February, according to the latest NAHB/Wells Fargo Housing Market Index (HMI) released today. The last three monthly readings mark the highest sentiment levels since December 2017.

“Steady job growth, rising wages and low interest rates are fueling demand but builders are still grappling with increasing construction and development costs,” said NAHB Chairman Dean Mon.

“At a time when demand is on the rise, regulatory constraints along with a shortage of construction workers and a dearth of lots are hindering the production of affordable housing in local communities across the nation,” said NAHB Chief Economist Robert Dietz. “And while lower mortgage rates have improved housing affordability in recent months, accelerating price growth due to limited inventory may offset some of that effect.”

…The HMI index gauging current sales conditions fell one point to 80, the component measuring sales expectations in the next six months was one point lower at 79 and the gauge charting traffic of prospective buyers also decreased one point to 57.

Versus implosion in the hoped for European rebound:

The ZEW Indicator of Economic Sentiment for Germany decreased sharply in February, falling 18.0 points to a new reading of 8.7 points. The indicator is thus slightly below its December 2019 level. The assessment of the economic situation in Germany has also worsened compared to the previous month, with the corresponding indicator dropping to a level of minus 15.7 points, 6.2 points lower than in January.

Expect it to get much worse in the months ahead as the China shock lands. At least the Brexit rebound will cusion it.

For now it is more of the same. The US economy is the COVID-19 safe haven of choice. Do not stand in its way.

The Australian dollar is hangong on for grim death but looks at severe risk of new eleven year lows.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.