This week, there have been multiple calls for the government policy to boost women’s superannuation contributions in order to bridge the gap in retirement savings between women and men.

It began when the Australian Council of Trade Unions (ACTU) demanded that the superannuation guarantee be lifted to 15% for women.

This was followed by KPMG which called for the federal government to make direct contributions into women’s superannuation accounts:

Women are the victims of these disparities in ways so egregious that KPMG observed “Australia discriminates against the majority of its population – women”…

“We say the government should provide super contributions for people on paid parental leave and provide top-up super for primary carers without demanding co-contributions,” Mr Wardell-Johnson said.

In another unexpected recommendation, KPMG called for the government to make super contributions for “those 50 to 59 receiving Commonwealth Rent Assistance”.

The Victorian Government also yesterday demanded direct government contributions to women’s superannuation accounts:

The Andrews Labor Government’s submission to the Commonwealth’s Review of the Retirement Income System makes a number of recommendations aimed at making sure women enjoy the same financial security in retirement as men – and aren’t penalised for taking time out of the workforce to have children.

Currently, women do not earn super on the Commonwealth’s Paid Parental Leave scheme. This means their superannuation balance takes an immediate hit, while they also forego compound interest for the rest of their working lives.

It’s unfair and it fails to recognise the professional hurdles they face when raising children.

The case for action is clear: The average woman’s superannuation balance at time of retirement in 2015/16 was $157,050, compared with $270,710 for men. That’s a 42 per cent superannuation gap.

That’s why the Labor Government’s submission makes a number of recommendations, including:

- Making superannuation payable as part of the Commonwealth’s Paid Parental Leave scheme

- Mandating superannuation funds to introduce a fee-free period of up to 12 months for parents on parental leave

- Allow joint superannuation accounts for couples, including same-sex couples

- Amend the sex discrimination act to allow employers to offer higher superannuation payments for female employees without requiring them to seek exemptions

As part of its recommendation, the Labor Government wants the Commonwealth Government to deliver on its commitment to increase the Super Guarantee rate to 12 per cent – and provide a pathway for it to be lifted to 15 per cent.

All of these demands miss the main reason why superannuation is skewed so heavily against women: because of the inequitable way that concessions are distributed, which disadvantages low paid workers irrespective of gender.

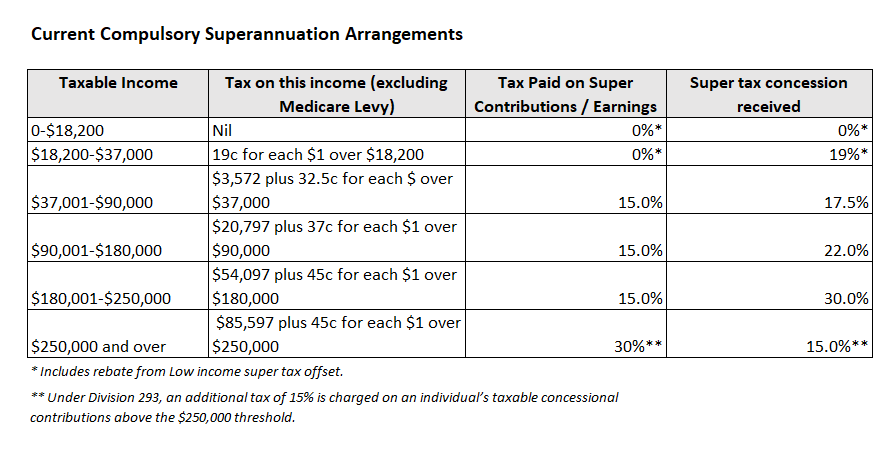

Under current arrangements, most superannuation contributions/earnings are taxed at a flat rate of 15%. Accordingly, those on low incomes receive minimal concessions, whereas those on higher incomes receive the biggest tax concessions:

Since women generally earn less than men over their working lives – because they tend to work in lower paid professions (e.g. nursing and teaching), work part-time, or take time off from working to raise children – they obviously accumulate much lower superannuation balances.

Therefore, the first best solution for those worried about superannuation inequity is to reform the system to make concessions equitable by targeting concessions at those who need it most – i.e. lower and middle income earners.

That is, the system should be made progressive so that lower income earners – be they male or female – get a better deal.

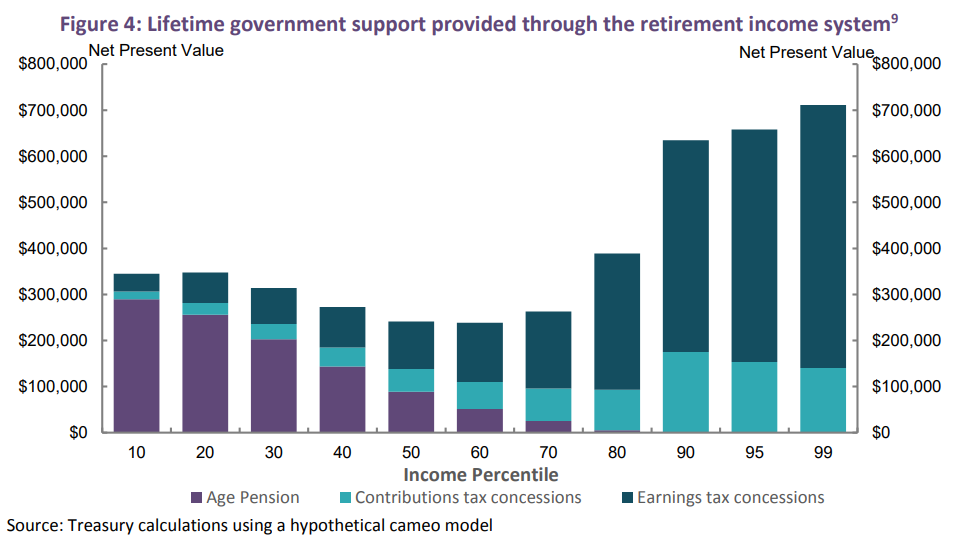

The federal budget would also benefit from superannuation concessions going where they are needed most, given superannuation is currently being used as a tax avoidance scheme by the wealthy (mostly men) who would never have taken the Aged Pension anyway (as illustrated clearly in the next chart).

As shown above, the top 1% of income earners will receive more than $700,000 in taxpayer contributions to their personal superannuation accounts over their working lives, dwarfing the $50,000 received by the bottom 10% of income earners, according to the Australian Treasury.

Let’s also not forget that Australia’s compulsory superannuation system already costs the federal budget $38 billion per year – far more than it saves in Aged Pension costs. Thus, increasing government contributions to women’s superannuation accounts would increase this budgetary cost, leaving less funds to raise the Aged Pension or housing rent assistance.

Indeed, the welfare of women (and lower income earners generally) would be improved if Australia’s superannuation concessions were abolished altogether and the budgetary savings were instead directed into boosting and broadening the Aged Pension. Although I’ll admit this is a ‘bridge too far’ politically.

More broadly, the growing outrage over the disparity between male/female superannuation and earnings is largely a fake issue. Most of us belong to family units whereby husbands/wives pool their financial resources – both incomes and savings – and share workloads, be it paid or domestic.

Moreover, when couples divorce, financial resources are split-up and distributed among the spouses, including superannuation savings.

So, instead of fighting manufactured gender wars and playing identity politics, policy makers should instead focus on eliminating poverty, irrespective of gender.

Making the retirement system equitable is a good start, beginning with overhauling the superannuation concession system.