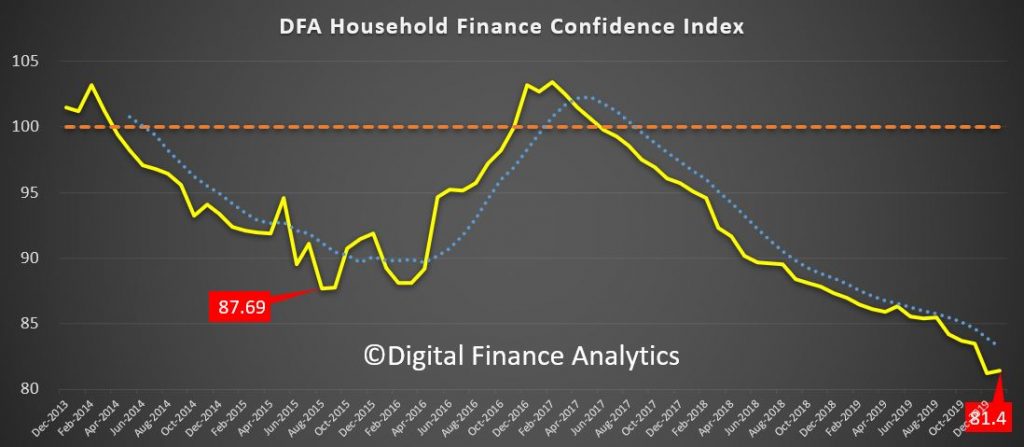

The latest results from our household surveys revealed that household financial confidence recovered just a little in recent weeks, but is still in ultra-low territory and well below the neutral 100 measure, at 81.4.

So far, the impact of virus concerns have not translated into households finances, whereas the bushfires, floods and other local events are having a more direct impact.

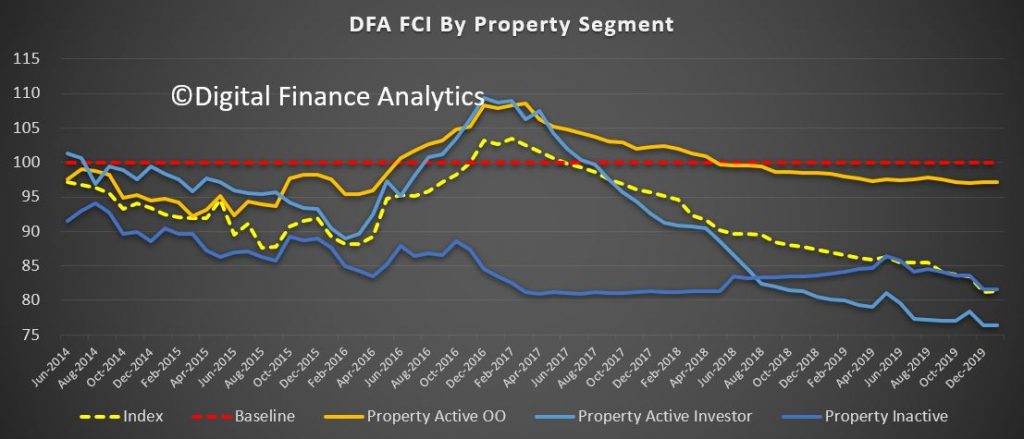

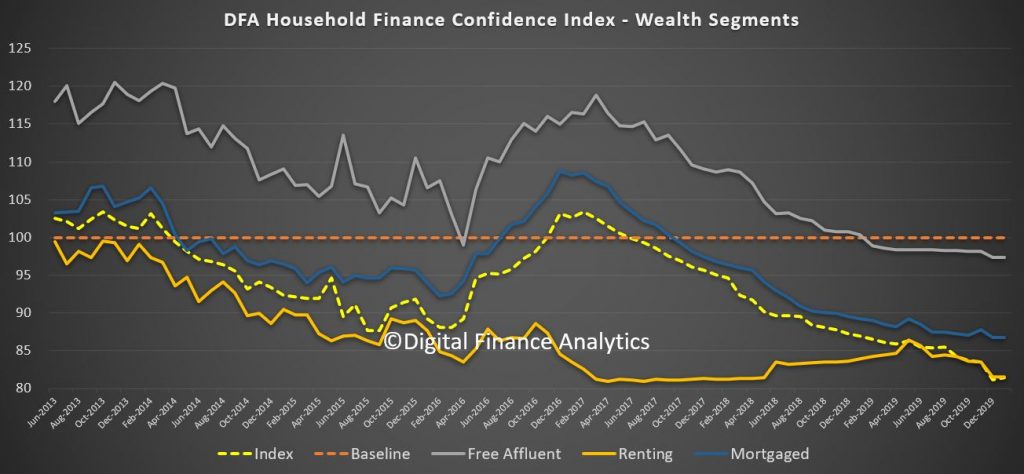

Across the property segments, owner occupied households are the most positive, thanks to rising prices in some locations and lower interest rates on some mortgages. Property investors and those renting remain more bearish, as rental costs continue in the doldrums.

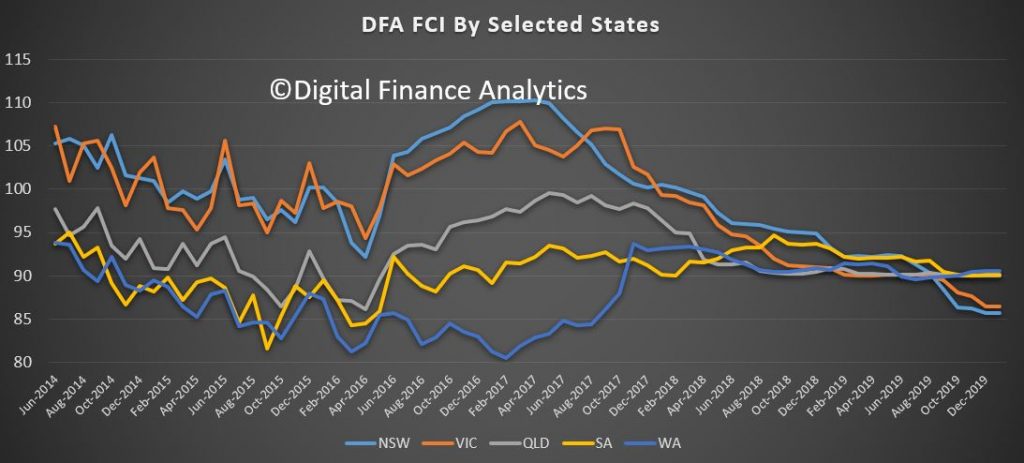

Across the states the recent trends continue, with both NSW and VIC households under greater financial pressure compared with WA, QLD and SA. Much of this is debt related as the average mortgage size grows ever larger in the two largest states.

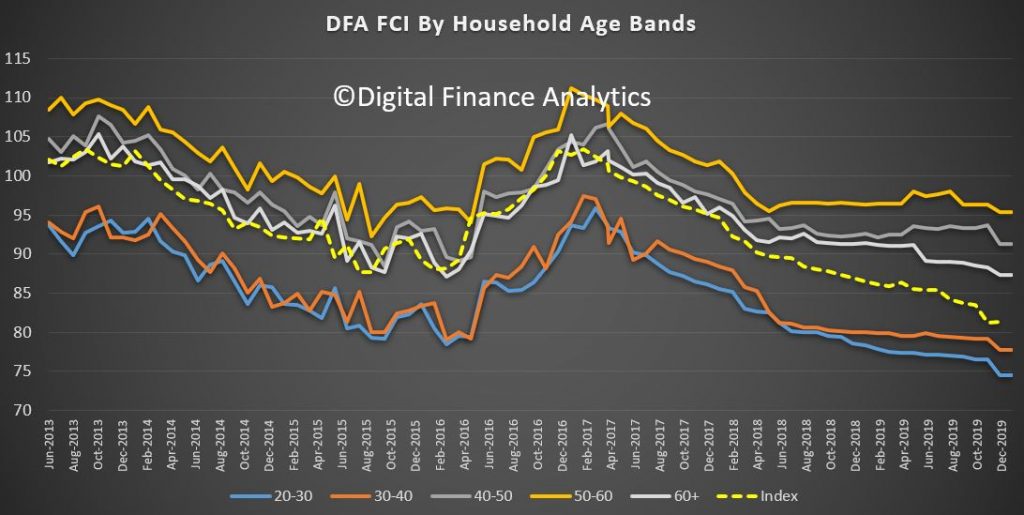

We continue to see pressure among younger households building relative to those in the older cohorts. Much of the pressure comes from housing costs one way or another.

Those mortgage free and owning property are relatively better placed than those with a mortgage, or renting. This is because housing costs are such a large element in a budget whether servicing a mortgage or paying rent.

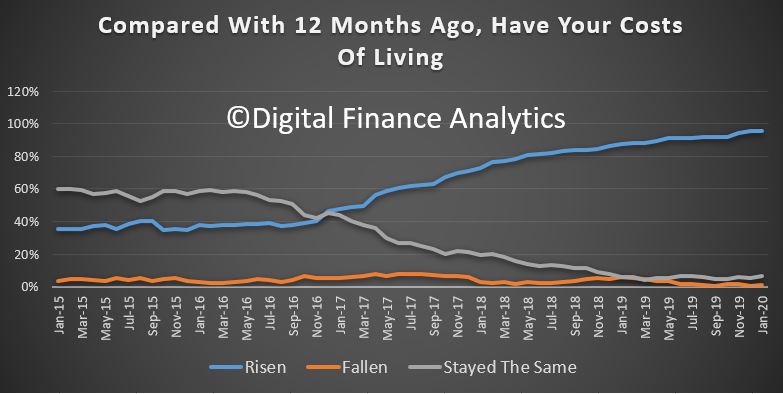

Looking in more detail at the moving parts, living costs continue to rise disproportionately, thanks to more expensive fresh food (drought related), child care and school fees rising fast, accelerating healthcare costs and continued high energy and fuel costs. 95% see their costs higher than a year ago. More are having difficulty with council rates and other regular commitments.

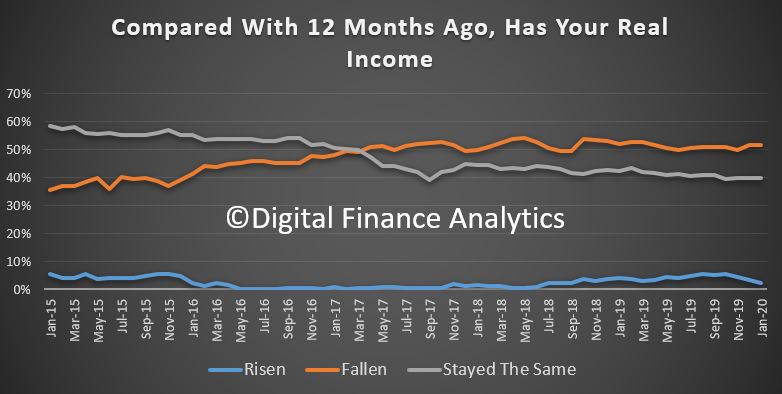

Income growth is muted at best, with 51% saying their income has been reduced in real terms over the past year, with both wages growth sluggish, and income from savings on deposits crashing as the cash rate is cut, and banks squeeze margin. Returns from share investments on the other hand are doing better. Those with spare income are preferring to pay debt down, rather than spend.

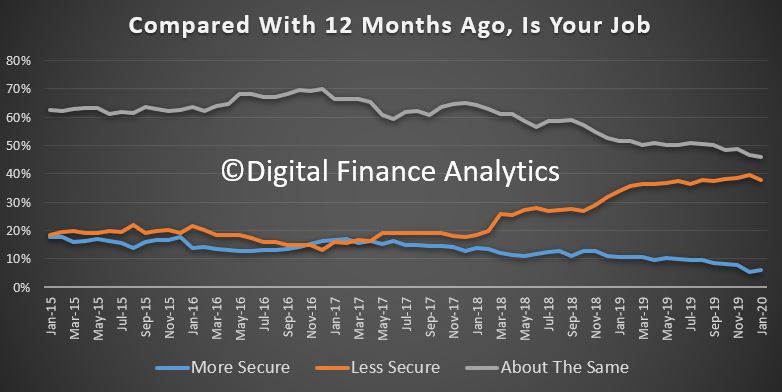

Job prospects are also sluggish, with just 6% feeling more secure than a year ago, while 38% are feeling less secure. We continue to see a pattern of multiple jobs, rising part-time jobs, less overtime and gig economy roles on the rise; all creating greater concerns about job security. Underemployment remains a critical issue for many.

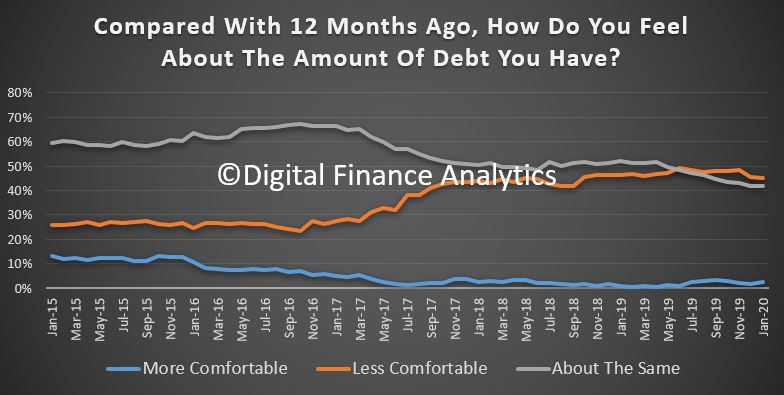

Turning to loan finances, some have been able to refinance to lower rate mortgages (and others appear to be missing the opportunity to switch and save), while some households are unable to transfer to a lower rate thanks to underwriting constraints. Households are able to grab a larger loan now lending standards have been loosened. Lower rates mean that 42% remain about the same with regards to confidence, while 45% are less comfortable than a year ago. We also note a rise in the use of unsecured debt, and buy-now pay-later (which will be the subject of an upcoming article based on new data we have captured). De-leveraging continues among those who can afford it.

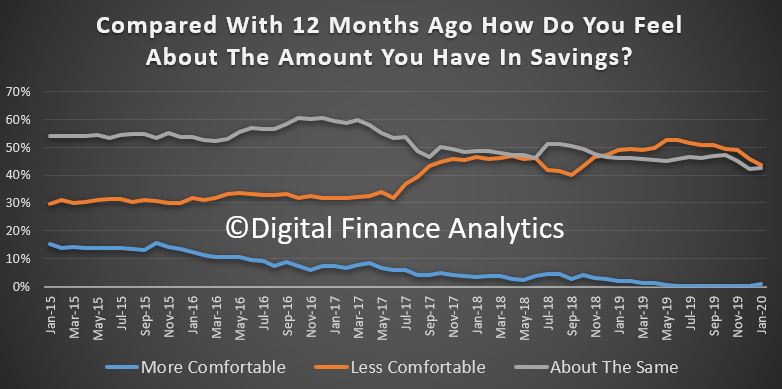

On the savings front, those with market investments continue to enjoy paper capital growth, while dividends remains relatively stable. But those with term deposits continue to see rate compression and there is a move from term accounts to call accounts as the margin between the two have fallen further. More than 3 million households rely on income from bank deposits, and the reduction in the returns from deposits is having a dramatic impact on many. That said, many households remain adamant that they do not want to take on more market risk, so reluctantly accept lower income – which in turn flows to lower spending. 43% feel less comfortable than a year ago. Many are dipping to savings, and using capital for living expenses, something which may not be sustainable.

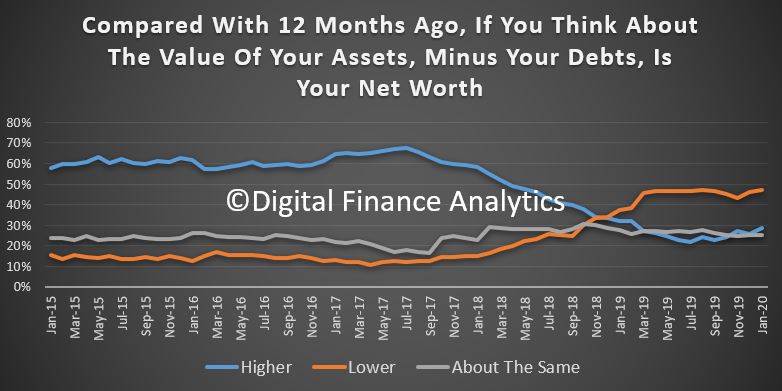

Finally, putting all this together we look at net worth – assets minus loans and other liabilities. The upturn in home prices reported in the media have flowed through to more expectations of growing wealth. 28% now have higher net worth than a year ago. That said 47% have lower net worth, thanks to rising expenses, and little in the way of savings. 24% reported no change. We note some significant differences between the more affluent segments and suburbs where net worth is rising (and supported by rising market investments) compared with regional areas and the urban fringe where there is no evidence of any wealth effect – so far. This is continue to dampen spending.

So, to conclude, we appear to have reached something of a floor in household financal confidence, but the journey back to more balanced settings will only be achieved once real incomes start to rise. Meantime the property recovering and wealth illusion may help a bit, but there is little here to suggest a rise in consumer spending. Many households are trapped in a high housing cost situation (either mortgage debt or rent) and with continued pressure in costs of living, the pressures will remain for some time to come.

The question is, what if anything might break the trend? Well income growth if it came, would assist on the upside, but then if growth stalls further thanks to the second order impacts from the virus, the confidence floor might just disappear. Households are in a finely balanced predicament.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.