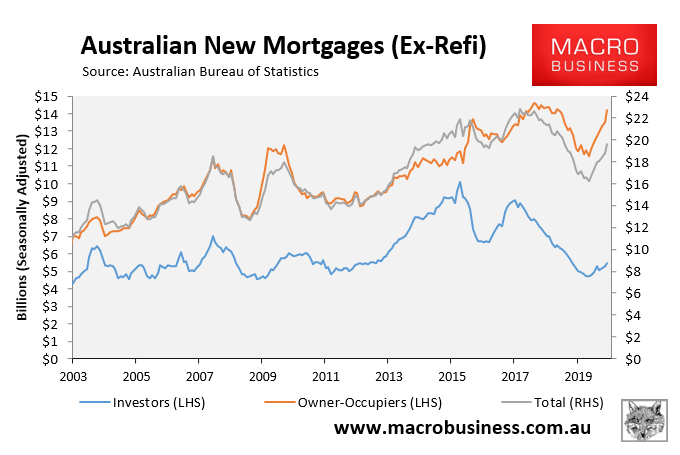

Yesterday’s new mortgages data from the Australian Bureau of Statistics (ABS) contained more bullish news for Australian house prices with both owner-occupied and investor mortgage demand lifting in December, continuing the strong rebound that began in mid-2019 following the federal election:

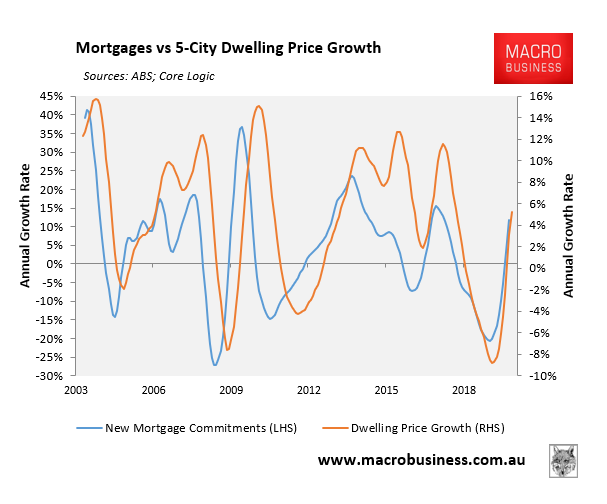

As shown in the next chart, there is a very strong correlation between new mortgage growth and the growth in dwelling values, with mortgages typically the leading indicator:

Therefore, the ongoing rebound in mortgage demand should propel dwelling values higher over the immediate horizon.

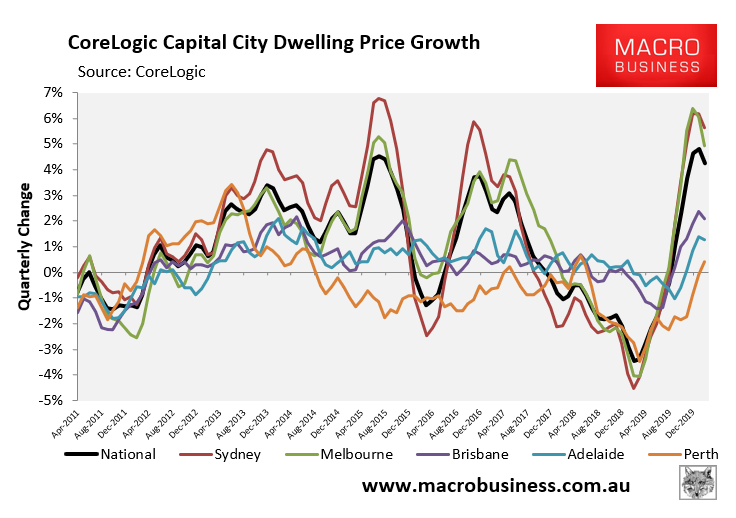

As we know, Sydney and Melbourne are the primary drivers of Australia’s house price rebound, both recording quarterly growth or around 5%:

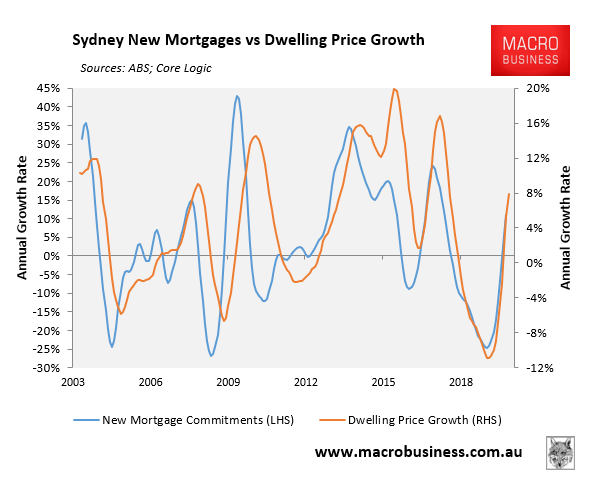

Not surprisingly, then, mortgage demand has also surged across both jurisdictions:

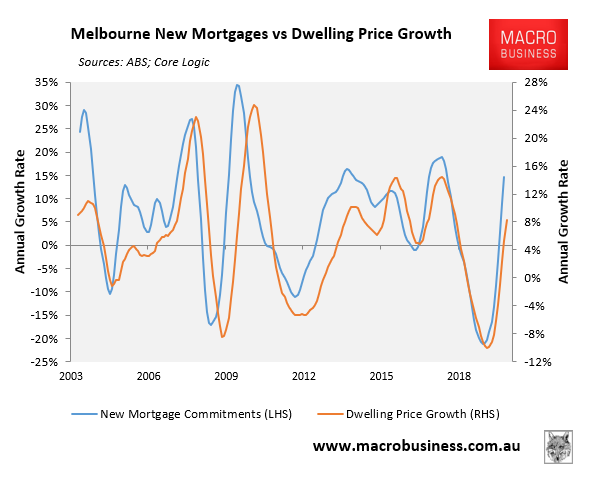

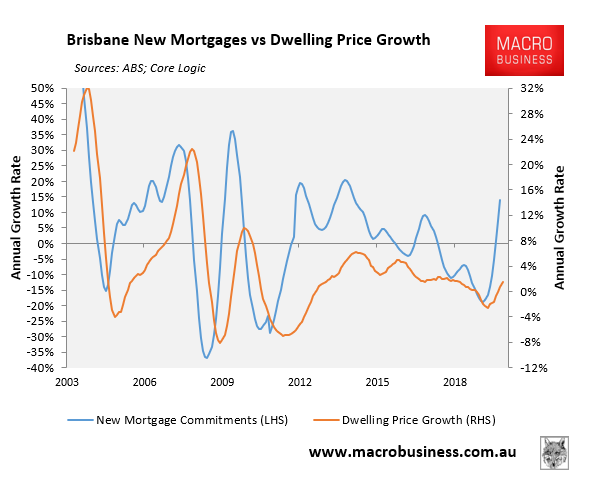

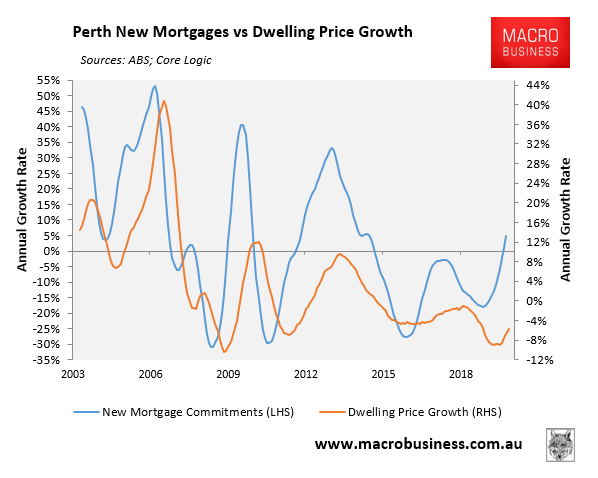

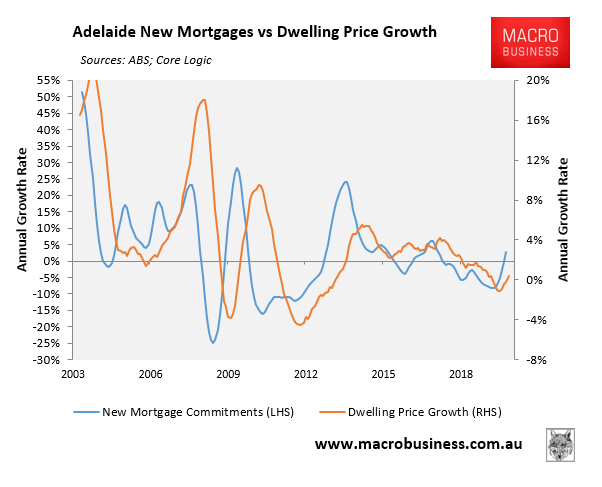

By contrast, the other major jurisdictions have experienced smaller mortgage rebounds and, therefore, lower price growth, as shown below:

Our base case is for the rebound in mortgage demand to continue over the near term, with house prices likely to rise through 2020, but to stall towards the end of the year.