Another sea of green across Asian stock market boards today, although Chinese stocks were much higher earlier in the session. Gold came back slightly after its big drop overnight even as USD strengthens against almost everything with offshore trading in Yuan seeing more weakness.

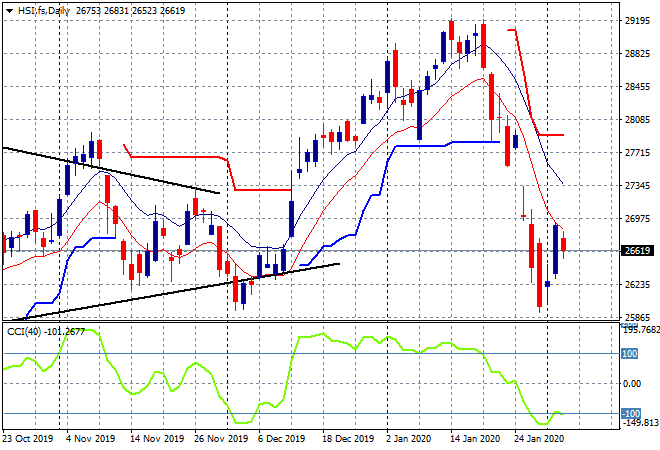

The Shanghai Composite has given up some mid session gains but is still up nearly 0.9% to breach the 2800 point level, still well off its pre-Lunar New Year highs. The Hang Seng Index is hovering along here, up only 0.2% to 26721 points, without making a new session high as price continues to look weak here – deadcat bounce anyone?

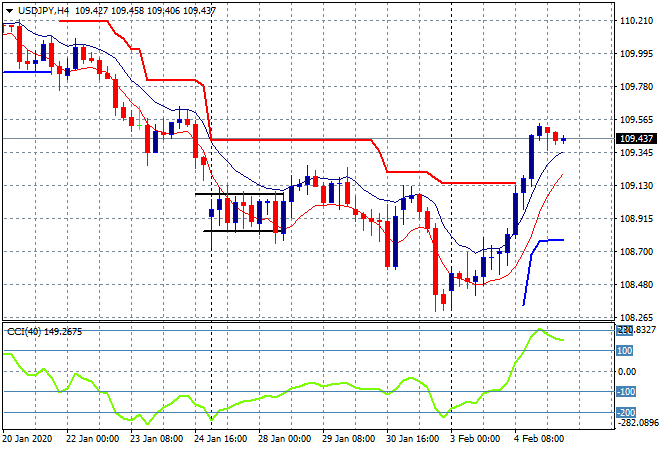

Japanese share markets continue to claw their way back with the Nikkei 225 closing 1% higher at 23319 points as the elevated USDJPY pair remains steady at the mid 109’s after a big short covering rally saw it lift to a two week high:

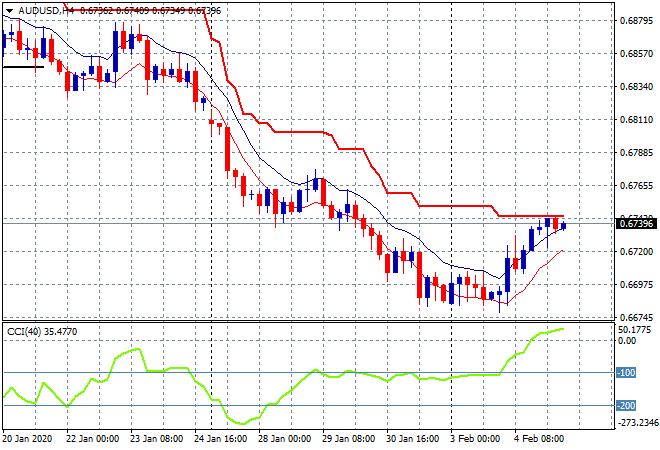

The ASX200 had another relatively modest session today, up only 0.4% only just missing out on getting back above 7000 points to close at 6976. The Australian dollar has stalled after its post RBA bounce, unable to break through trailing ATR resistance, as I still contend this move is temporary:

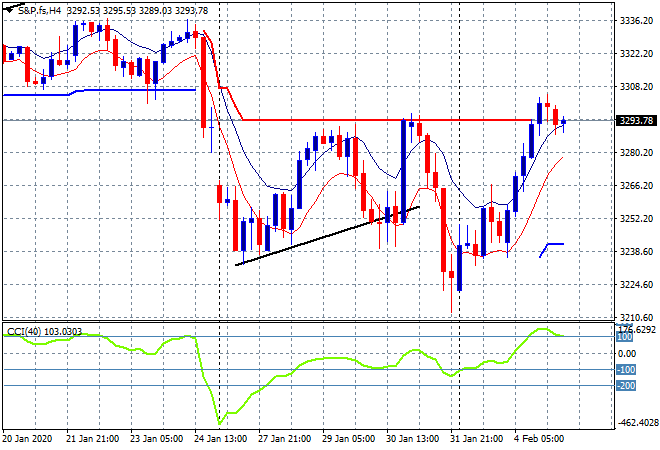

Eurostoxx and S&P futures are steady after the big rises on both sides of the Atlantic overnight with the four hourly chart of the S&P500 indicating some short term resistance at the 3300 point level after nominally breaking last week’s intrasession high:

The economic calendar includes a slew of preliminary PMIs in Europe but the event to watch is ECB President Lagarde in Paris, then the latest trade balance figures from the US and the ISM Services print.