The Australian dollar hung on to critical support again:

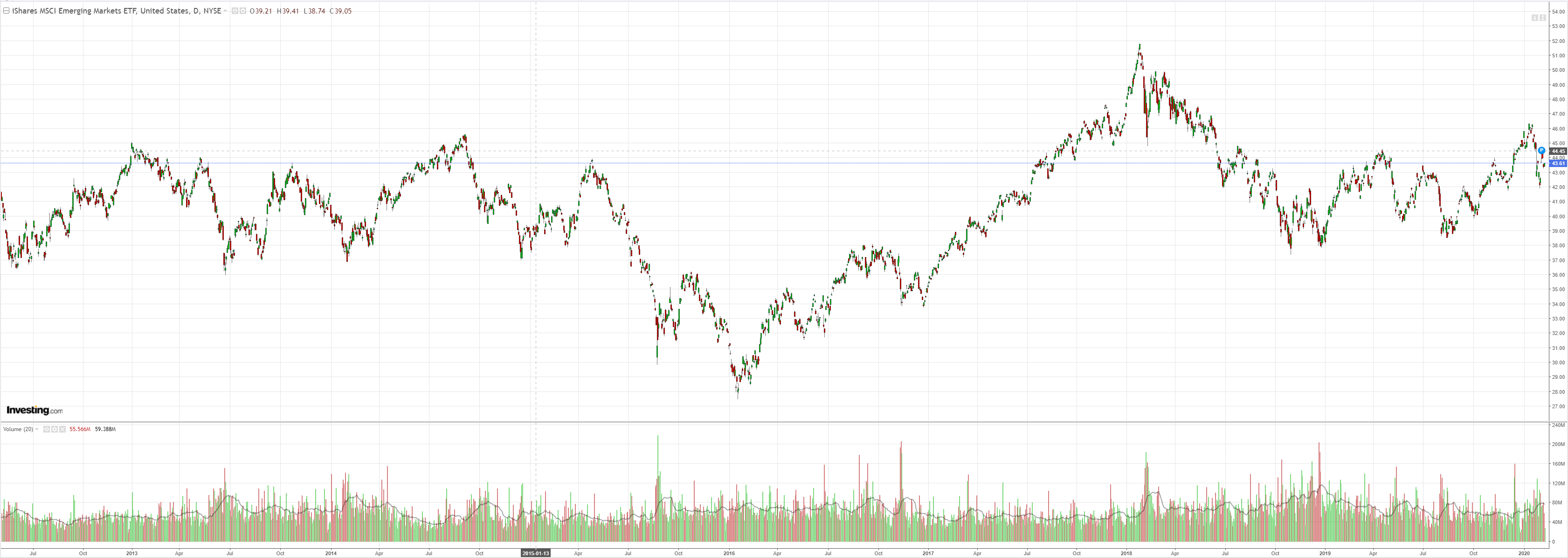

EMs were also weak:

Advertisement

Gold was firm:

Oil is getting trashed depite Libya and OPEC taking 1.5mb/d off the market:

Advertisement

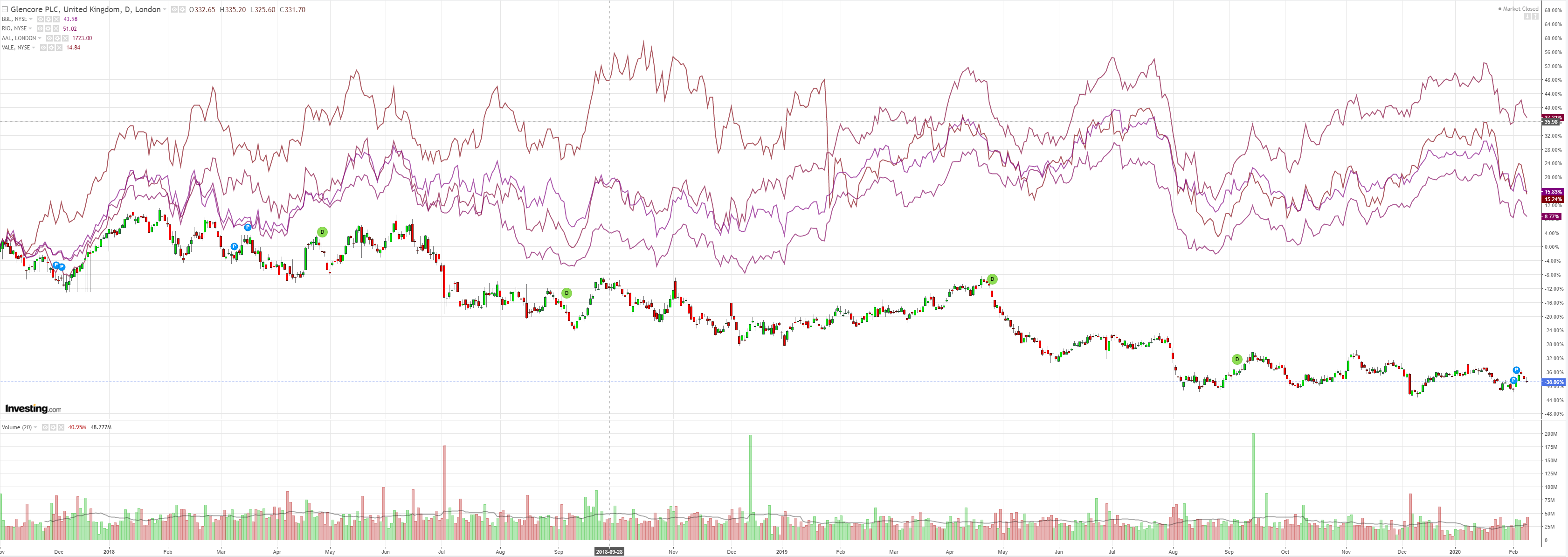

Metals are still falling:

Big miners too:

EM stocks were OK:

Advertisement

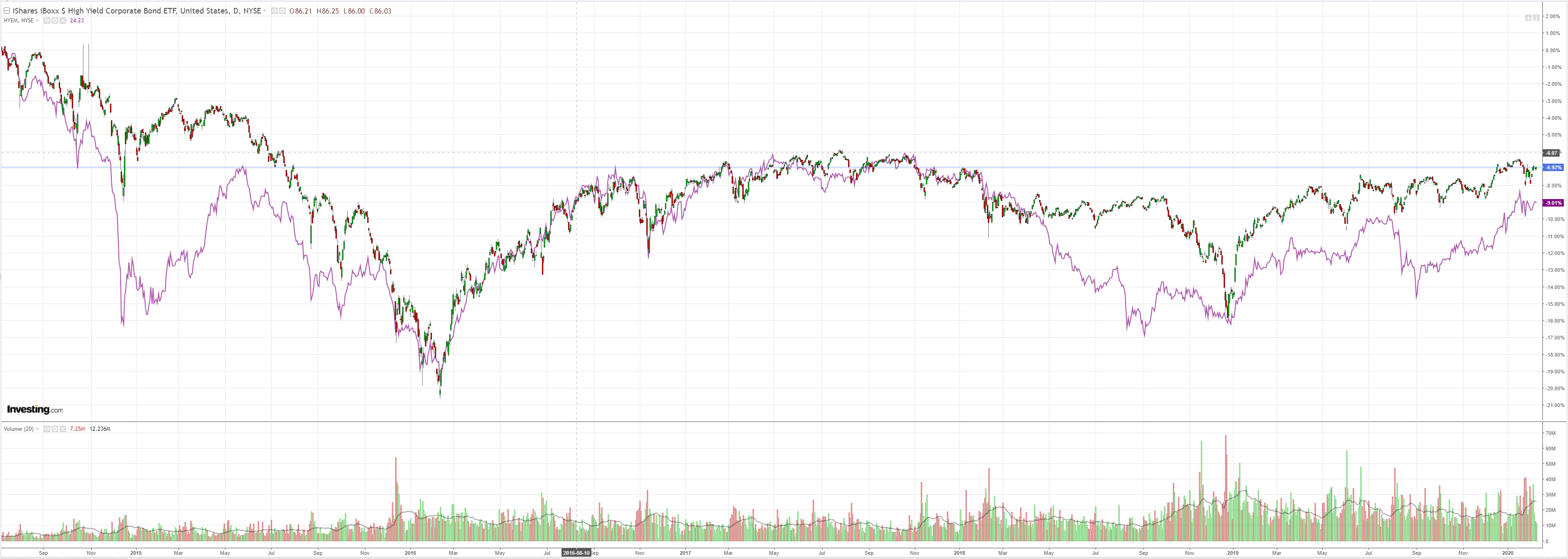

Junk is serene. This can’t last if oil keeps falling:

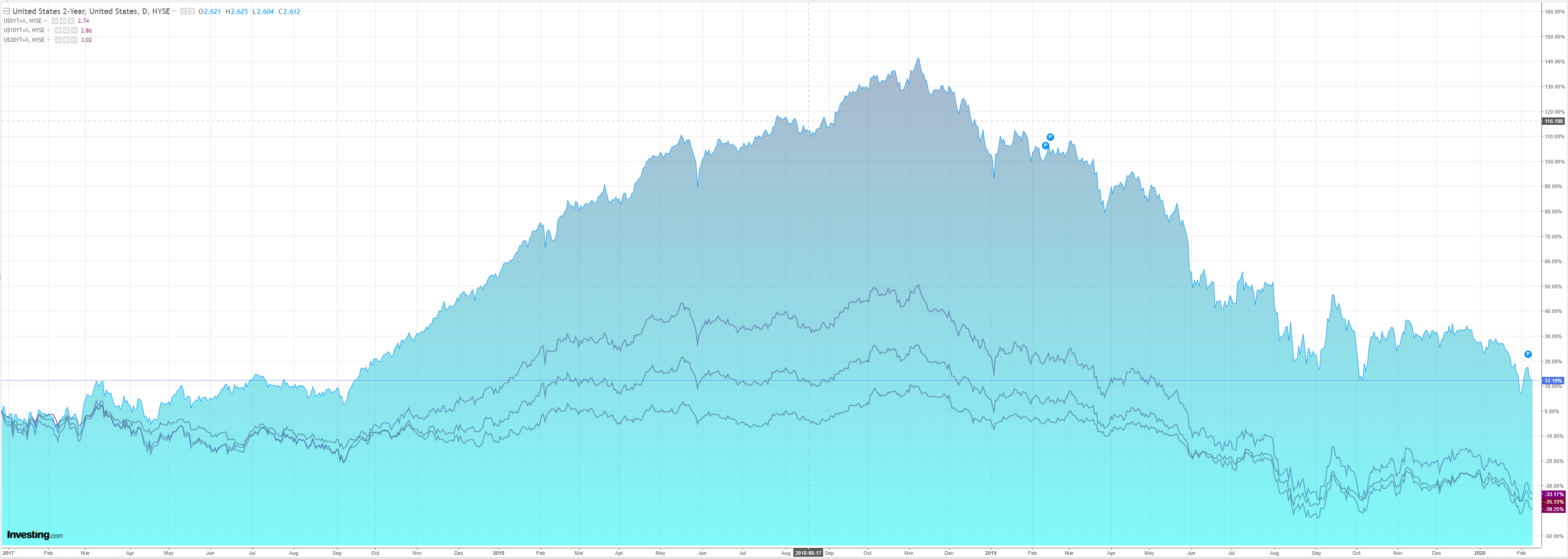

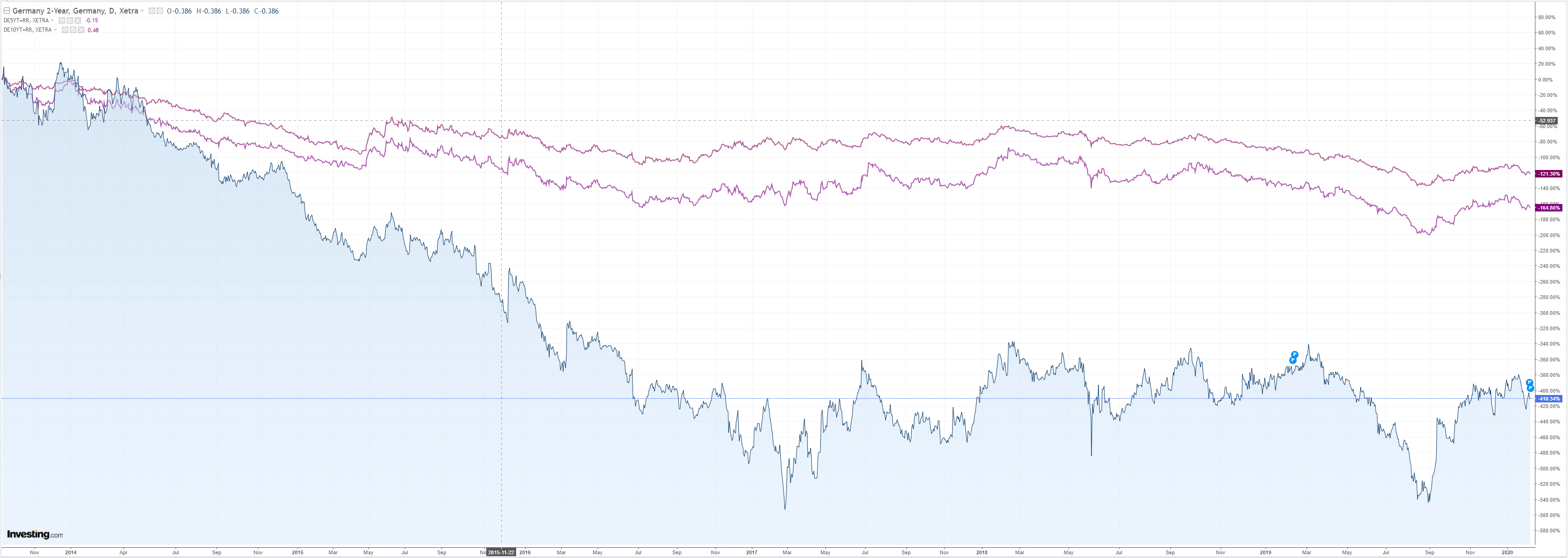

Bonds rallied:

Advertisement

As did stocks:

Westpac has the data wrap:

Event Wrap

No major data to report.

FOMC member Bowman said the economic backdrop looks “very favorable”, the economy should continue to grow at a moderate pace, with low unemployment, and an expected rise in inflation to its 2% target – all reflecting the key messages of the most recent FOMC policy statement. There was no indication that coronavirus had caused any material change in the economic outlook and policy stance. Daly said a mindset change was required, where inflation is a “bit above the target”, rather than below.

Updated coronavirus statistics show confirmed cases total 40,655 worldwide (40,199 in China), of which 910 have died (908 in China) and 3669 have recovered.

Event Outlook

Australia: Another robust gain for housing finance is expected in December, circa 1.6%. Demand for loans from owner occupiers has been driving growth in recent months and this is expected to continue in December. Meanwhile, the NAB business survey is likely to report another weak reading for conditions and confidence in January.

UK: The monthly GDP data points to a contraction in Q4, -0.1%.

US: Fed Chair Powell’s testimony will be the main event, with a particular focus on any discussion of the risks. Bullard, Quarles, Kashkari and Daly are also due to speak. NFIB small business optimism and JOLTS data are due too.

The narrative is intact. The US is the best place to hide from coronavirus.

Advertisement

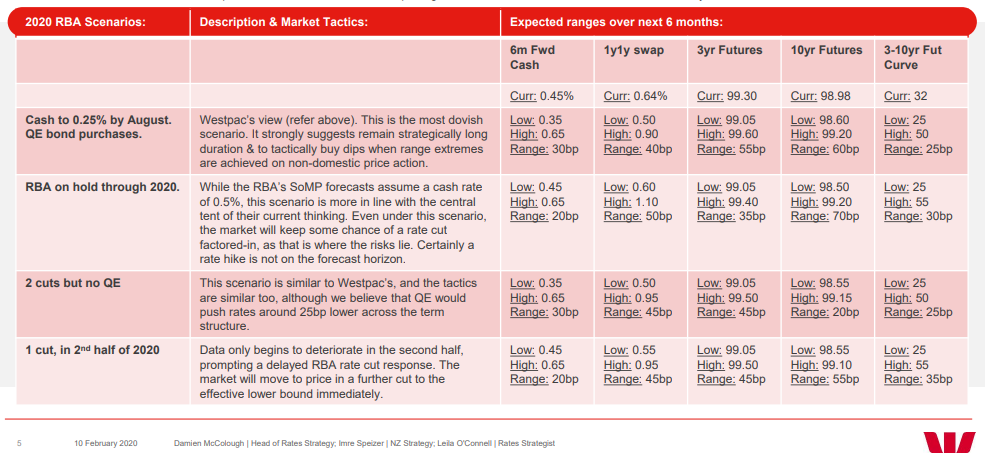

Sadly for us, the RBA didn’t cut, or the Australian dollar would now be in free fall. Westpac examines some spread scenarios while we wait for Dr Phil to catch up:

Last week, in his Governor’s Statement, speech and the SoMP, Phillip Lowe could not have sent a clearer message to markets around the near term policy track. He thinks the RBA has provided enough policy accommodation for now and is expecting an extended period of unchanged policy while they assess the impacts of that accommodation on the real economy. That view is very different to Westpac’s own. The RBA surprised us by retaining a growth forecast of 2.75% (around trend) for 2020, despite the weaker momentum apparent in the Q3 national accounts and developing questions around the global economy. It is also somewhat brave, given a range of leading indicators around the labour market, to assume that the recent falls in the unemployment rate will be sustained. Westpac’s forecast is for the unemployment rate to drift upwards over the first half of 2020. The uncertainty around the coronavirus poses substantial risks at least over the first quarter both globally and domestically, implying a realistic downward revision to growth forecasts, both globally and domestically. Westpac continues to expect that a combination of a more moderate growth outlook and an unexpected (by the RBA) deterioration in the labour market will require a further policy response. Currently we have April pencilled in for the next cut (followed by a further move in August) but recognise that the Governor may need more time to be convinced that further action will be required. As such, it is worthwhile exploring where markets could move in the first half of the year under different RBA scenarios.

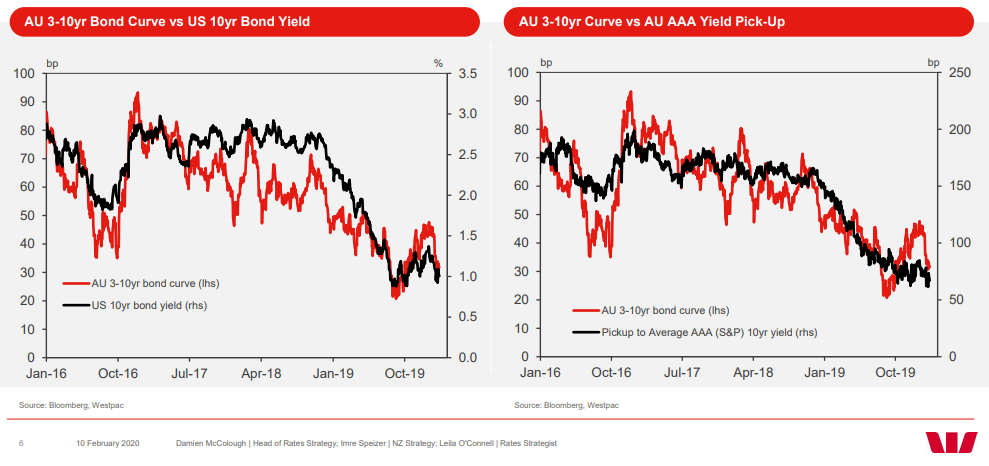

The AU bond curve has flattened in recent weeks during both bullish and bearish episodes. The bearish episodes, such as last week, have been largely a result of a re-pricing of RBA expectations, while the bull flattening episodes have been driving by long end buying on safe haven flows (chart at left). So will this trend stop being the case? We have held a curve flattening preference for some time and do not have a tactical or strategic desire to shift significantly from that view. The same major themes that have driven the curve flatter in recent years are still in play. Lower domestic cash rates and a global liquidity glut that is underwriting a search for yield remain in play. That being said Australia’s yield advantage relative to other AAA sovereigns (chart at right) is the smallest it has ever been. So that should slow the pace of curve flattening from current levels. Other headwinds are likely to come from any renewed market confidence that the RBA will shift policy in similar way to our own forecast timing. Even so, those sort of steepening impulses will continue to be short-lived.

I remain confident that the RBA’s terrible forecasting ability will prevail in short order and it will be forced to cut again as the coronavirus shock arrives in earnest.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.