Exclusively from Gerard Minack at Minack Associates:

Australia remains stuck with the macro blahs: tepid growth in aggregate and stagnation per person. The risks are skewed to the downside. The key to the downside unfolding is not whether there’s a fluky one quarter GDP decline, but whether the labour market weakens. Falling employment would trigger powerful adverse feedback loops that likely cause a major recession. Expect the RBA to ease again to reduce this risk – unless fiscal policy is quickly deployed – and the A$ to continue to soften.

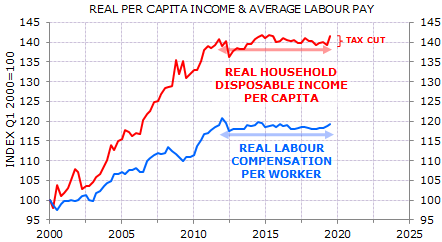

Australia’s domestic expansion remains sub-par, despite record-low interest rates, a below-average A$, and recent tax cuts. It’s easy to see why: labour pay and household disposable income have stagnated in real terms since late 2011 (Exhibit 1).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.