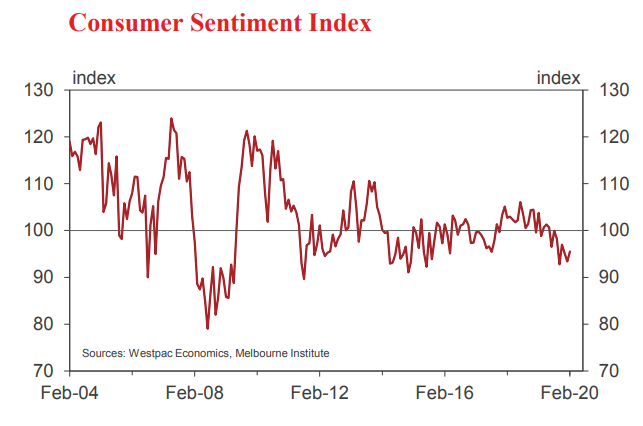

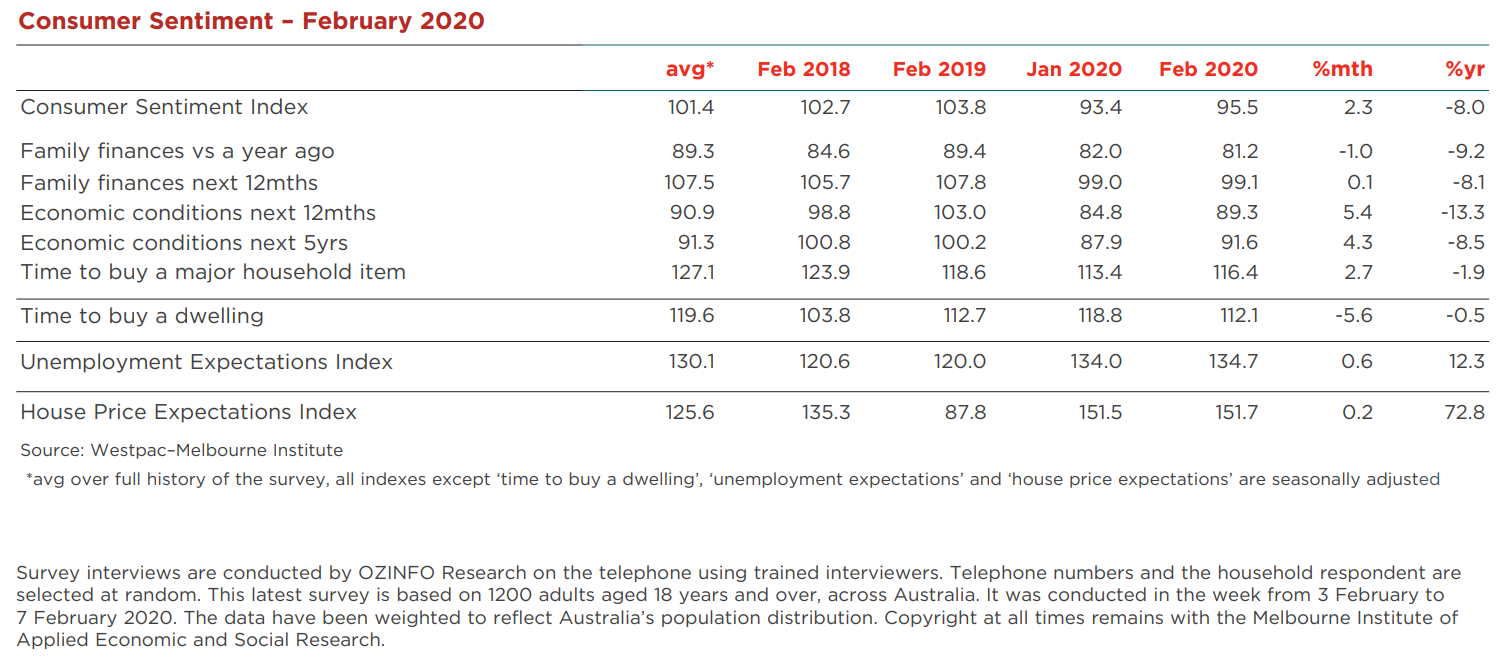

The Westpac-Melbourne Institute Index of Consumer Sentiment rose 2.3% to 95.5 in February from 93.4 in January.

Despite the modest improvement this month, sentiment remains weak overall. At 95.5, the Index remains well below the long run average of 101.4 and firmly in pessimistic territory (readings below 100 indicate that pessimists outnumber optimists). This downbeat mood has prevailed since mid-2019 and coincided with a marked slowdown in consumer demand that looks to have carried into early 2020.

The lift in sentiment this month likely reflects easing concerns around bushfires and comes despite some significant negative developments, most notably the coronavirus outbreak abroad.

On the positive side, the survey week saw extensive rain in bushfire-affected regions with several large fires declared contained. The week also saw a confident tone from the RBA, with a range of commentary emphasising the bank’s positive medium term outlook for the Australian economy. Notably, consumer sentiment readings showed a clear improvement over the course of the survey week.

Against this, the escalating coronavirus outbreak looks to have had only a limited effect on consumer sentiment. While surprising, this is similar to the experience during the SARS outbreak in 2003 which had little or no impact on sentiment in Australia, although it had a material impact on confidence elsewhere, China in particular. The fairly muted response from financial markets may also have dampened the sentiment impact locally – the ASX is down only -0.6% since the previous survey in Jan. That said, the full impact of the outbreak is yet to be felt locally and we may see more of a drag on sentiment in the months ahead, particularly as the hit to sectors such as tourism and education start to come through.

The component detail this month showed the gain came from a recovery in expectations for the economy and in attitudes towards major purchases, partially offset by a deterioration in assessments of family finances.

The ‘economy, next 12 months’ sub-index rose 5.4% in February and the ‘economy, next 5 years’ sub-index rose 4.3%, both sub-indexes partially reversing the sharp falls seen over the previous two months but still 1–2% below their November levels.

Assessments of family finances were less promising. The ‘finances vs a year ago’ sub-index fell 1% in February to be back near recent lows while the ‘finances, next 12 months’ sub-index was essentially unchanged in the month but down sharply since mid-2019 (–10.7% compared to the average read over the first half of 2019). Both sub-indexes remain well below their long run averages despite several interest rate cuts, significant tax relief and a turnaround in housing markets – a pattern that points to other powerful headwinds bearing down on household finances.

Responses to an additional question on interest rate expectations show fewer consumers expect more rate cuts in 2020. Every six months we ask consumers about their expectations for mortgage interest rates over the next year.

The February results show just 16% expect rates to move lower, down from 22% back in August but still above the 10% read a year ago. Perhaps the most telling statistic is that 13% of consumers report that they simply “don’t’ know”, well above the 7% average seen over the last decade.

Attitudes towards major purchases improved in February but still look to be restrained. The ‘time to buy a major household item’ sub-index rose 2.7% in the month but remains 1.3% below its November level. At 116.4, the sub-index is well below its long run average of 127, suggesting consumers will continue to keep a tight rein on discretionary spending.

Labour market concerns have shown little change. The Westpac-Melbourne Institute Unemployment Expectations Index rose slightly, edging up 0.6% to 134.7 in February (recall that higher readings indicate that more consumers expect unemployment to rise in the year ahead). The index has moved sideways in recent months but is still up 12.3% on this time last year, consistent with a slowdown in jobs growth and rising unemployment over the year ahead.

Housing-related sentiment was mixed in February, buyer sentiment deteriorating but price expectations up a touch after recording another very strong gain last month.

The ‘time to buy a dwelling’ index fell 5.6% in February, unwinding a similar sized gain last month to be back near recent lows. The monthly pull-back was broadly based suggesting it may reflect some shift in expectations around interest rates. At 112.1, the index is again showing a clear softening compared to last year’s peak around 127 although it remains well above 2017 lows which saw the national index touch 90.

The Westpac-Melbourne Institute Index of House Price Expectations Index edged 0.2% higher in February, consolidating after a spectacular 70% surge over the previous nine months. Consumer price expectations continued to lift in NSW (+4.5%) and Vic (+1.7%) but cooled in Queensland (–3.7%) and partially retraced last month’s very sharp gain in WA (–12.9%).

The Reserve Bank Board next meets on March 3. Westpac expects the Bank to again leave rates unchanged but retain a clear easing bias. We continue to have a more downbeat view on Australia’s economic prospects for 2020 with growth expected to be around 2% rather than the RBA’s

expectation for an around trend 2.75%. As such, we see a combination of weak economic growth and deteriorating labour market conditions drawing a further policy response from the Bank. However, the RBA’s surprisingly confident forecasts, as well as likely near-term volatility associated with temporary shocks, casts doubt over how quickly they will respond. Currently we have April pencilled in for the next cut but the Governor may need more time to be convinced.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.