There is a common myth that Australia’s compulsory superannuation system has boosted national savings.

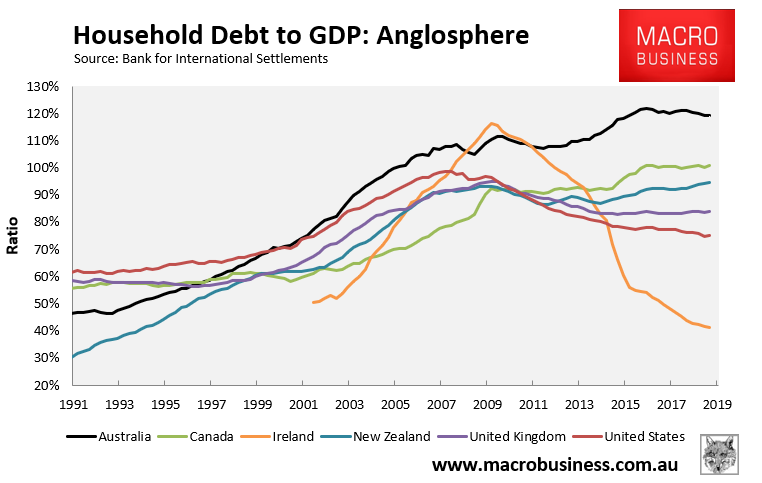

However, Fidelity International has challenged this misconception, arguing instead that superannuation is fueling the growth in Australia’s household debt, which is now the second highest in the world (see next chart), by forcing households to borrow more to offset the forced saving.

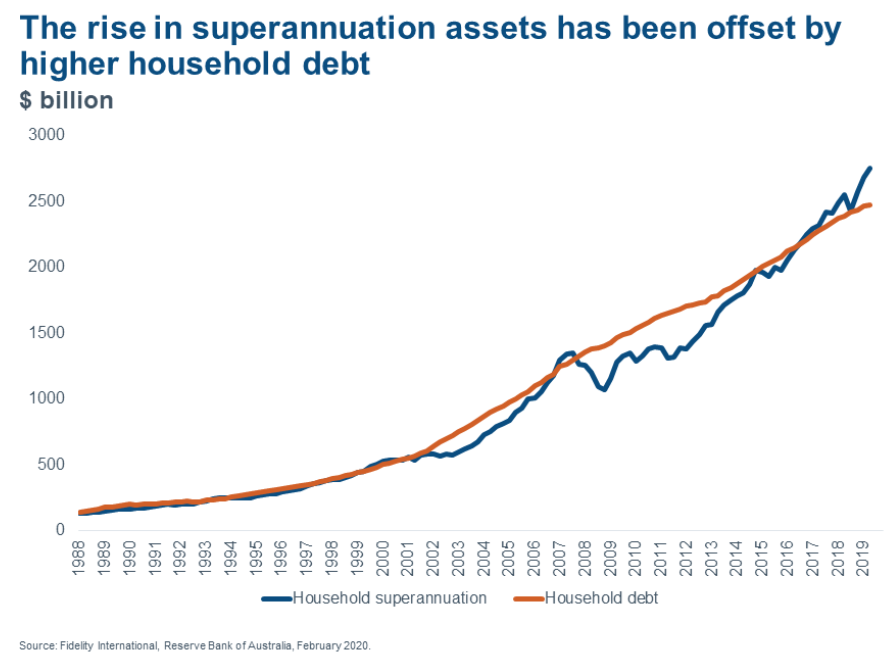

Australians have been making compulsory superannuation contributions since 1992. Today, there is around $2.75 trillion dollars in retirement savings in superannuation funds. As a result of the accumulation and growth of this savings pool, Australia now has the fourth-largest pension market in the world. On the other side of the balance sheet, Australians also have the second-highest level of household debt to GDP in the world at around 120 per cent of GDP. Household debt has grown in nominal terms from $217 billion dollars in June 1992 to almost $2.5 trillion dollars today.

Total superannuation assets and household debt have grown at a similar rate since 1992, suggesting that the superannuation saved by Australians has largely been offset by increased borrowing. It appears that the knowledge that most Australians have a pool of money waiting for them in retirement has resulted in the Australians becoming more comfortable with accumulating higher levels of debt during their working lives. Lower interest rates, increases in household incomes, and higher house prices have also contributed to the run-up in debt seen over the past 27 years.

Fidelity’s view was tacitly supported by RBA governor Phil Lowe last week, among others – as noted yesterday by Adam Creighton:

Lowe said as much last week too: “If you have to save more through super, you might save less voluntarily and therefore your consumption doesn’t move.” Trumpeting how much money is in accounts labelled “superannuation” ignores the overall balance sheet.

Michael Littlewood, a New Zealand academic who spent decades studying different retirement income systems in different countries, says German, New Zealand and Australian households have remarkably similarly levels of retirement assets, despite having vastly different retirement systems.

Advertisement

The fact remains that ‘savings’ in superannuation funds are only large because the government mandates it, not because they are inherently special. To quote economist Richard Denniss:

Much is made of the enormous size of Australia’s $2.9tn pool of superannuation savings, but we talk much less about the fact that the only reason it grew so big was that we literally force the vast majority of employees to spend 9.5% of their income buying superannuation every week. Let’s be clear: if we forced all Australians to get a massage every week or buy a new Australian car every year, we would have an enormous massage and car industry as well.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.