By Gareth Aird, Senior Economist at CBA:

Key Points:

- Non-mining business investment in Australia has eased. And forward looking investment intentions were downgraded in the mostrecentABS Capex Survey.

- We expect non-mining business investment to be sluggish in 2020.

- But this outcome is not locked in and there are policy levers that couldbe pulled to help lift private investment.

Overview:

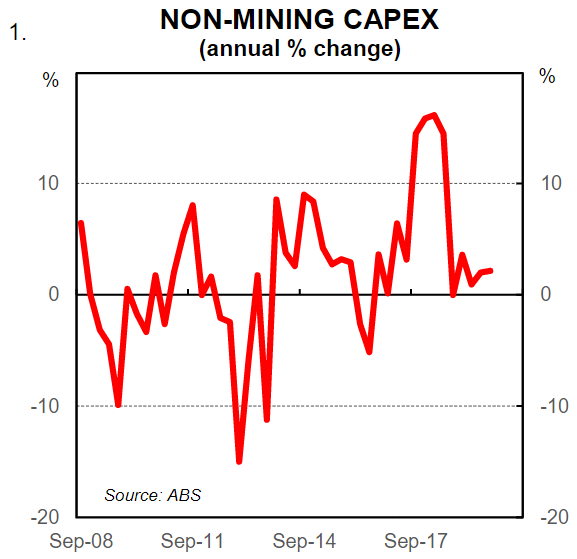

Non-mining private capex in Australia rose solidly in 2017 and 2018 after an extended period of weakness. But growth in non-mining business investment stalled during 2019 (chart 1). When the Q4 19 national accounts are released in early March we expect to seen on-mining capex rose by a soft 1.5% in 2019. And our forecast for 2020 is for a rise of just 0.3% (i.e. broadly flat). Business demand for credit is soft, the ABS forward looking intentions for non-mining capex are weak and a range of private surveys, including the CBA PMIs, are pointing to non-mining investment remaining sluggish in the near term. The outlook, of course, can change. And policy has a role to play.

The benefits of stronger investment are plentiful. Capital investment is essential for sustained job creation. And capital deepening, the situation whereby capital per worker is increasing, can boost productivity and living standards. In general, a lift in productivity is essential for a sustained lift in real wages. But Australia has a poor track record in terms of productivity growth in recent years (chart 2). There has been strong growth in hours worked but not a lot of growth in the capital stock and productivity growth has sagged. In this note we take a look at why non-mining business investment has stalled and why we expect it to remain sluggish in 2020. The outlook is better for mining investment, but this note focuses exclusively on non-mining capex given investment in the resources sector is almost entirely driven by external demand. We conclude with a discussion on some of the policy levers that could be pulled that would help to generate a lift in private non-mining investment.

Why non-mining investment has stalled?

(i) Expectations of domestic demand are too weak

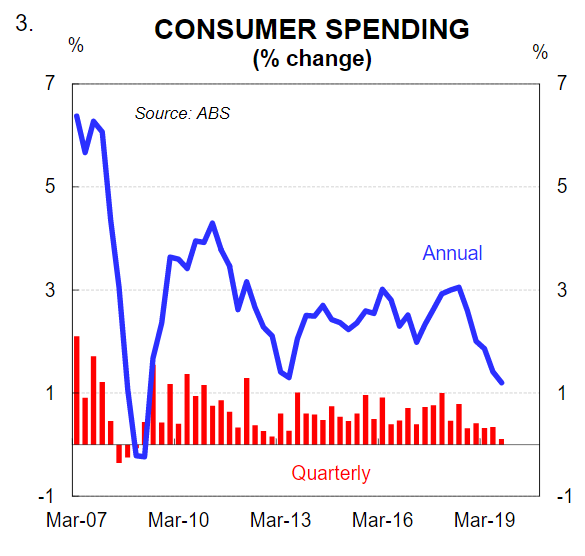

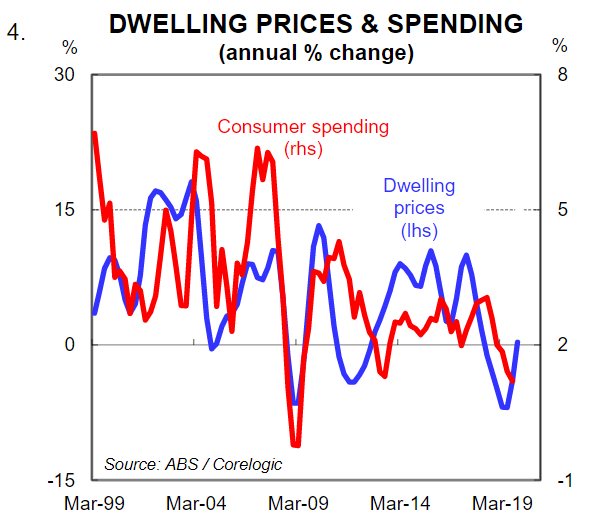

Investment generally follows demand. That is, in most instances private investment is responsive to demand rather than supply creating demand. External demand, particularly for commodities and education, has remained resilient. But domestic demand has weakened. A recent survey by the Australian Industry Group (AIG)showed that 41% of business CEOs surveyed cited a lack of demand as the as the top inhibitor to their business growth. Consumer spending, which accounts for 56% of Australian GDP, was soft over 2019. The unwelcome combination of weak wages growth, record high household debt, elevated job security fears and concerns around the economic outlook trumped decent employment growth and low unemployment on the spending decisions of households. The net result has been well-below-trend growth in consumer spending (chart 3).

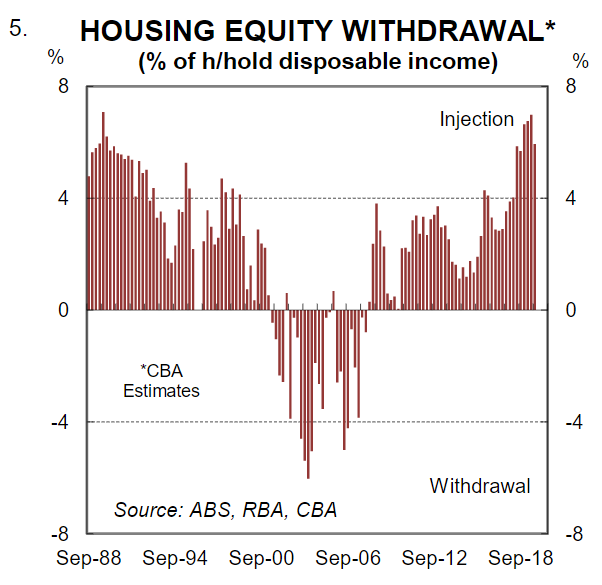

A negative wealth effect due to falling dwelling prices was also at work over the two-year period to mid-2019 which weighed on consumer spending (chart 4). The property market has since turned and dwelling prices are now rising. But as yet the boost in housing prices has not translated into higher household expenditure. Indeed with an apparent de-leveraging mindset at work, the future boost to spending via a wealth effect from rising house prices may be more muted than in the past. That is because: (i) households have used rate cuts to accelerate debt repayment rather than free up disposable income; and (ii)there has been a lift in household net equity injection which currently sits at multi-decade highs (chart 5).

We do not expect the outlook for non-mining business investment to improve in any material sense until expectations of consumer demand lift. And for that to happen there must be a shift in either the household perception of the economy or an increase in household income growth (via wages or tax cuts). A pickup in wages growth looks unlikely in the near term given elevated labour market slack. And there is little apparent appetite from the Government to bring forward legislated tax cuts. So it’s probably down to a sustained improvement in the household perception of the economy and lift in consumer demand for businesses to respond with increased investment. The recent evidence indicates that rate cuts on their own will not be sufficient enough to lift consumer sentiment. And, in fact, rate cuts may actually damage sentiment. So it will take a broader policy response to turnaround the household perception of the economy (see section2).

(ii) Global policy uncertainty is heightened

“You know, people talk about this being an uncertain time. You know, all time is uncertain. I mean, it was uncertain back in -in 2007, we just didn’t know it was uncertain. It was -uncertain on September 10th, 2001. It was uncertain on October 18th, 1987, you just didn’t know it.” Warren Buffet

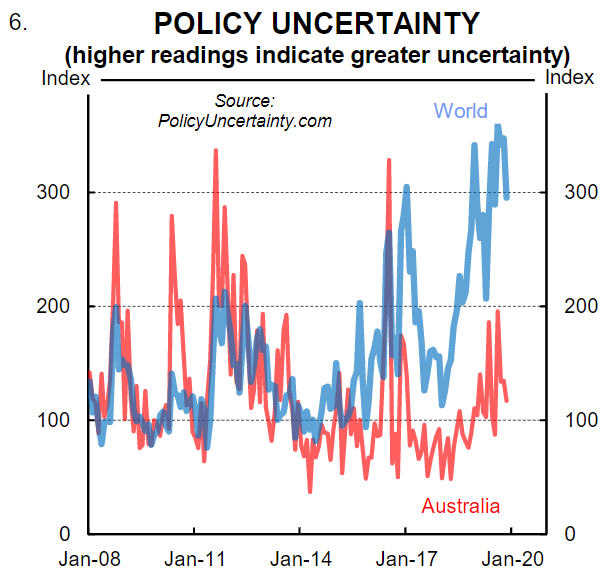

The world has always been uncertain. But there are periods of time where policy uncertainty is higher than usual as has been the case more recently (chart 6). A raft of so called geopolitical issues have led to an increase in policy uncertainty which has weighed on business investment, both locally and internationally. US-China trade policy, Brexit, developments in the Middle East and civil unrest in Hong Kong have all contributed in varying degrees to boost downside risks to the global economy which weighs on investment. And more recently concerns about the spread of the coronavirus have gripped financial markets. The virus has killed at least 170 people and infected more than 7,700. Financial markets are pricing in the risk that the Chinese economy, and by extension the world economy, will slow because of the disruption caused by the virus. Weaker investment could follow, both locally and abroad.

(iii) Fiscal policy is too tight

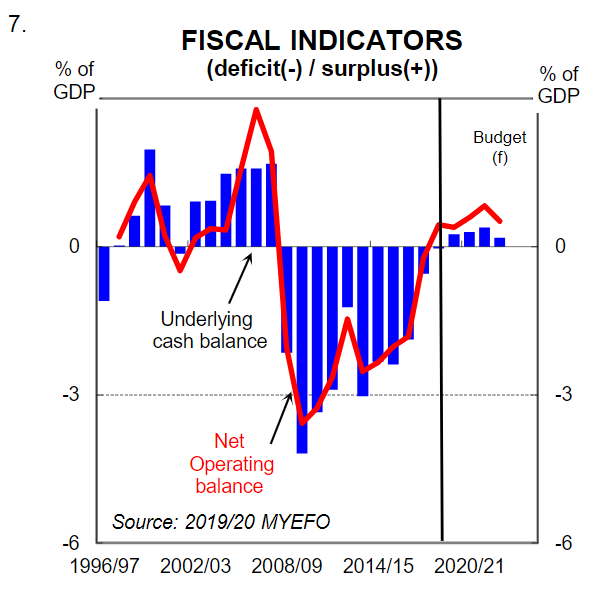

Fiscal policy is essentially changing government spending (recurrent and investment) and taxation to influence aggregate demand. The stance of fiscal policy is deemed “contractionary” or “expansionary” by looking at the direction and size of the expected change in the budget balance. At present, the stance of fiscal policy adopted in the Federal budget is contractionary (chart 7). Growth in taxation is greater than growth in expenditure, which is why the deficit has shrunk and the budget is now essentially balanced.

Whilst it is true that public spending has risen as a share of the economy and tax rebates totalling around $A7½ billion have been delivered to the household sector in 2019/20, overall growth in revenue has been stronger than growth in expenditure. Shrinking the Commonwealth Budget deficit in this manner in pursuit of a surplus effectively sucks money out of the economy resulting in a contractionary impact on aggregate demand.

The idea that private demand will be crowded out by boosting public demand has merit when the economy is running at full tilt will little spare capacity in the labour market. But when an economy is operating below trend and there is excess spare capacity in the labour market, as is presently the case in Australia, an increase in public demand should crowd in private demand.

(iv) Drought

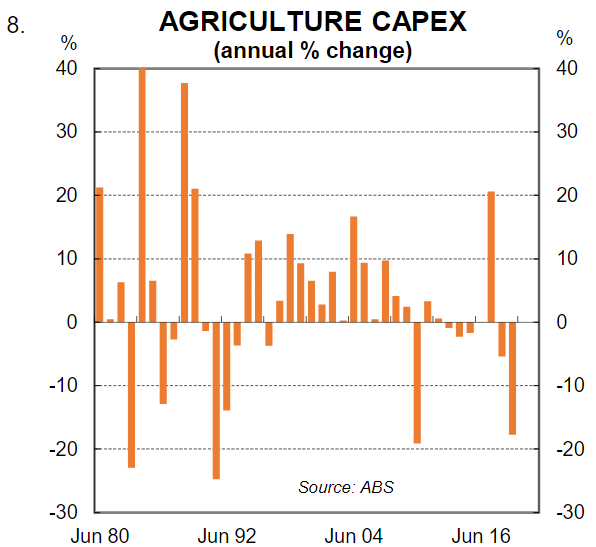

Large parts of New South Wales, Queensland and South Australia have been in extreme drought conditions since 2017. Droughts are common in Australia. But this one has been particularly bad because the effects of diminished rainfall have been exacerbated by a record run of above-average temperatures and terrible bushfires.

There have been clear and obvious economic costs. The drought had a big negative impact on both farm production and investment in 2018/19(chart 8). Agriculture capex fell by a whopping 17.7% in 2018/19 (i.e. $A2.3bn). In time the drought will break and investment in the agriculture sector will rebound. But given the prediction that dry conditions are expected to continue for a while yet, a lift in agriculture capex doesn’t look likely in the near term.

(v) Hurdle rates are too high

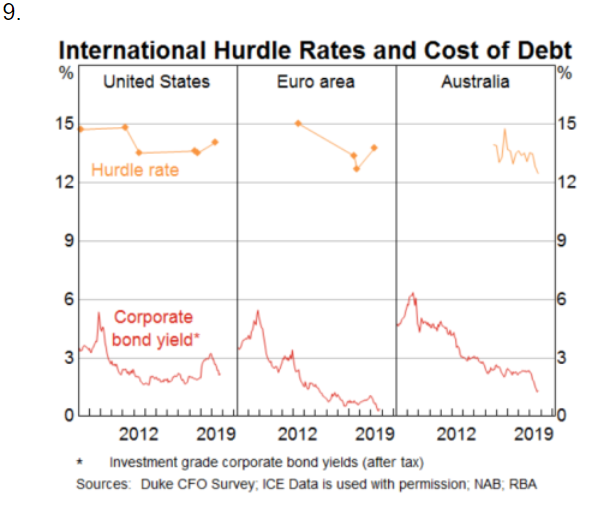

Firms generally use Discounted Cash Flow (DCF) analysis (or a version of it) to estimate the attractiveness of discretionary capital investment. But a range of evidence indicates that hurdle rates are often much higher than the weighted average cost of capital (WACC). A number of key policymakers have made this observation.

In October 2019, RBA Governor Lowe started that, “average hurdle rates of return for new investments in many countries have not changed much. It seems that there is a global norm for hurdle rates somewhere around the 13 to 14 per cent mark and it is hard to shift this norm” (chart 9).

These sentiments were echoed by the Australian Competition and Consumer Commission (ACCC) Chairman Rod Sims in early January 2020. Sims remarked that he hoped companies were, “reducing cost of capital calculations and not sticking to some benchmark that is no longer justified”. And that, “returns should be lower because interest rates are lower”.

We very much agree. Hurdle rates around 13% look unrealistically high in a low inflation and low interest rate environment. If hurdle rates were reviewed more frequently, they would have declined in line with inflation and interest rates.

The ‘stickiness’ of business hurdle rates is in stark contrastto valuationmethods employed in other areas. The property market is a case in point. Investors have been willing to accept lower nominal returns as interest rates have fallen. This makes sense as returns should be benchmarked against the risk free rate.A review of business hurdle rates would be a positive step to see more projects get across the line.But of course it is not something that canbelegislated and implemented across the board. Rather itis up to individual businesses to lower hurdle rates.

What could be done to lift investment

(i) Loosen fiscal policy to boost aggregate demand

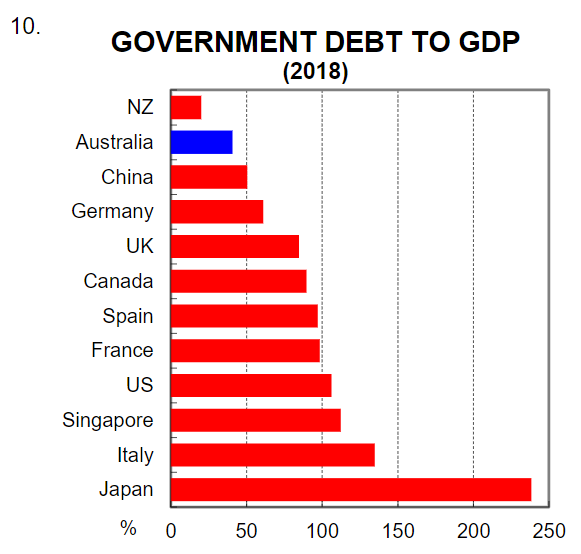

The Budget is in balance and Government net debt as a share of GDP is low (chart 10). At the same time, economic growth is below potential, household consumption and business investment are weak and there is a plenty of spare capacity in the economy. And of course the RBA cash rate is at a record low of just 0.75%. So the case for fiscal stimulus is strong.

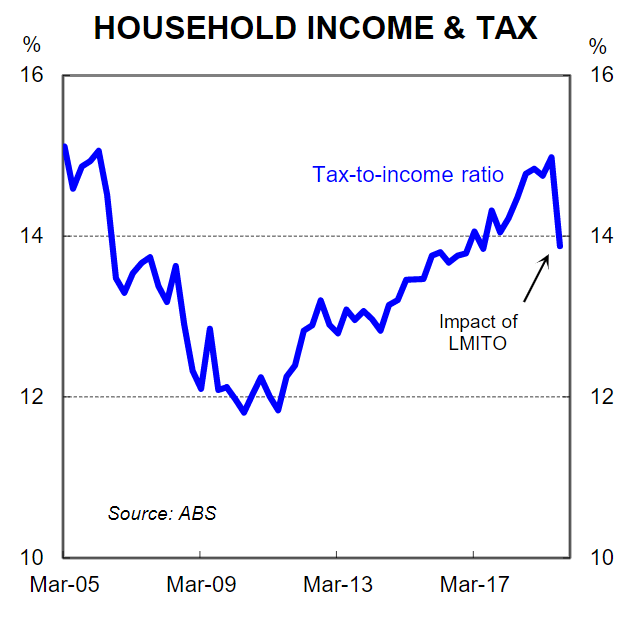

There are essentially three options that available to government to loosen fiscal policy: (i) cut taxes (personal and/or business); (ii) increase recurrent expenditure; and (iii) increase public investment. The recent trends in household disposable income, the tax-to-income ratio and government expenditure mean that the case for personal income tax cuts is stronger than the case for a further lift in recurrent expenditure and investment.

Australian workers haven’t had a tax cut in any material sense for years. Bracket creep means that workers are handing over an increasing proportion of their salaries each year to the tax office. As a result, the tax-to-income ratio has been on a solid uptrend over the past five years (chart 11). This has been weighing on growth in household disposable income and on the capacity for households to spend. Businesses have responded by scaling back investment.

(ii) Accelerated depreciation / investment allowances

Businesses generally can’t deduct spending on capital assets immediately. Instead they claim the cost over time, reflecting the asset’s depreciation. Investment or accelerated depreciation allowances, however, would allow businesses to deduct for tax purposes a larger proportion of their expenditure on capital equipment in the year of purchase as opposed to waiting until later years to reclaim the expenditure.

Such policy is preferable to a company tax cut for two key reasons. First, a company tax cut does not guarantee a lift in investment. At a time of soft aggregate demand a business tax cut might simply boost after tax profits rather than providing the catalyst for greater investment and economic activity. On the other hand an investment allowance is a direct incentive to bring forward capex spend. Second, a company tax cut would deliver a significant windfall to foreign investors which would be at the expense of the Federal budget bottom line in perpetuity. Investment allowances would impose no such cost. Federal Treasurer Josh Frydenberg has recently hinted that an investment allowance may be forthcoming by stating, “the government will continue to engage with the business community about what further reforms can drive even greater investment and further improve our competitiveness”.

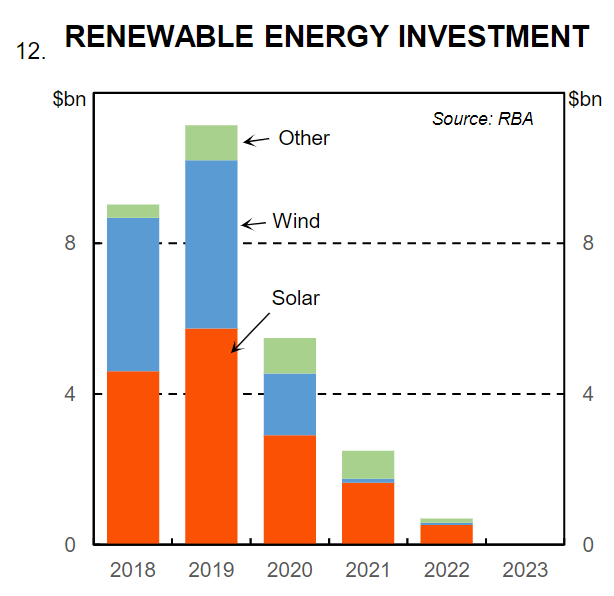

(iii) Clarity and certainty on energy policy

Renewable investment has slowed significantly (chart 12). Part of the decline in renewable investment can be attributed to excessive government intervention in the electricity market coupled within consistent policy. As our Mining and Commodities Strategist, Vivek Dhar, recently noted, new renewable investment in the national electricity market has increasingly become more dependent on government involvement(both Federal and State). The absence of a market mechanism to price carbon effectively is the leading cause of uncertainty.

There is clearly both the scope and need for a policy certainty and clarity on energy in Australia. In the first instance there would be a lift in energy-related investment from having a clearer energy policy. But secondly, increased investment in energy that reduces the price of power is akin to a tax cut for both the household and business sectors. In the case of the household sector, aggregate demand would be boosted by falling energy prices.

(iv) Productivity-enhancing reform and red tape reduction

Productivity-enhancingreform should be one of the mainstays on any policymakers’agenda. It should be a constant and ongoing process with the objective of raising productivity, economic outcomes, productive investment and living standards. Government policy, particularly at the Federal level, has been light on productivity-enhancing reform in recent years. But there is clearly scope for reform. The Productivity Commission’s 2017 report, Shifting the Dial: Productivity Review, for example, which is a detailed inquiry into Australia’s productivity performance, provides recommendations on productivity-enhancing reform. Pushing through with some of these policieswould have a positive impact onthe outlook for business investment in Australia.

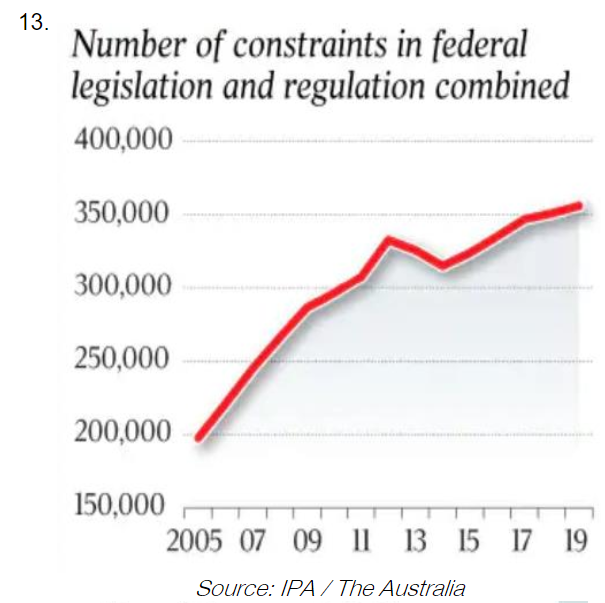

“Cutting red tape” can also help. Whilst the phrase “cutting red tape” can sound like a throwaway line, at its core, excessive red tape imposes costs on businesses that can often be a deterrent to investment. The CBA Global Markets team regularly meets with businesses across a range of industries. And we frequently hear first hand about the red tape and regulatory roadblocks that impose large costs to business. These often act as a hand brake on business investment. A co-ordinated approach between three-tiers of government, regulators and business to cut excessive red tape and unnecessary regulation would be a tailwind on business investment. According to the 2019 research paper “Regulation in Australia”, by the public policy think tank the Institute of Public Affairs, the number of regulations in Federal law has increased by 9% to 356,000 since 2013. And at a state level, QLD and Victoria are the most heavily inundated with red tape (charts 13 and 14).

(v) More monetary policy stimulus

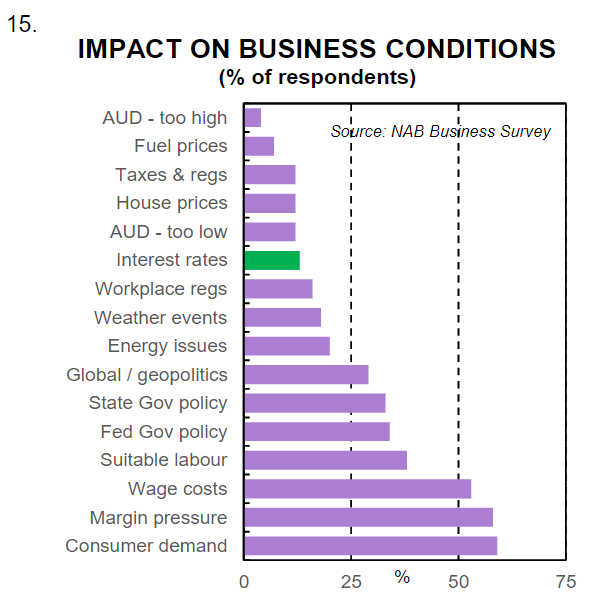

To be clear, the cost of money is not holding back investment. Business surveys show that corporates do not see the level of interest rates as an issue (chart 15). But as we have mentioned earlier, business investment responds to demand in the economy. The Australian household sector is highly indebted which means that the debt burden is a headwind on household consumption. Whilst most households do not reduce their monthly mortgage payments when interest rates go down, lower interest rates speed up the deleveraging process for households that carry debt. Over time this strengthens household balance sheets and growth in consumption will follow. In turn this will support business investment.

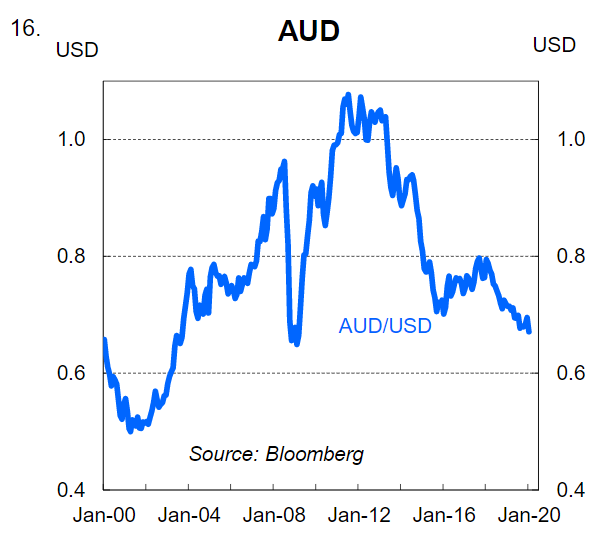

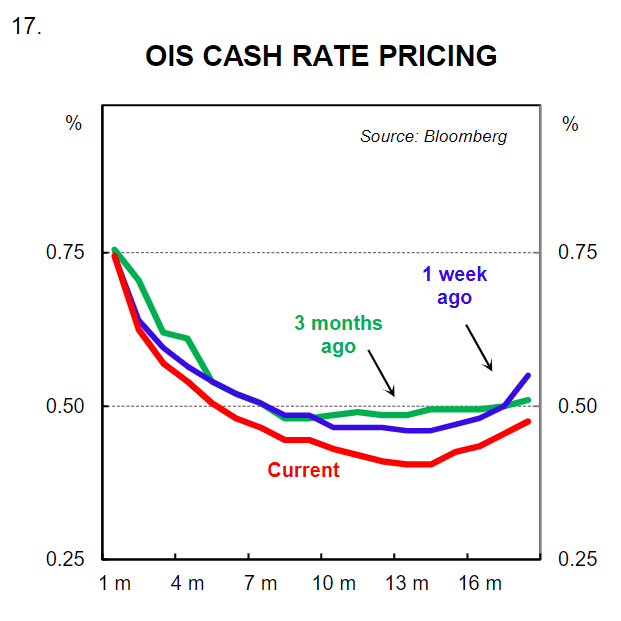

Lower interest rates should also put downward pressure on the AUD (chart 16). A lower level of the exchange rate can be positive for business investment as it makes Australian businesses more competitive on a global scale. We expect the RBA to provide more stimulus to the Australian economy and take the policy rate down to 0.25% in 2020.Current market pricing implies a terminal rate of 0.37% (chart 17).This will boost demand at the margin. We should stress, however, that monetary policy can only do so much, particularly as we reach the lower bound. It cannot do anything to change the more entrenched and structural impediments to growth. And there are both benefits and costs to taking the cash rate lower.