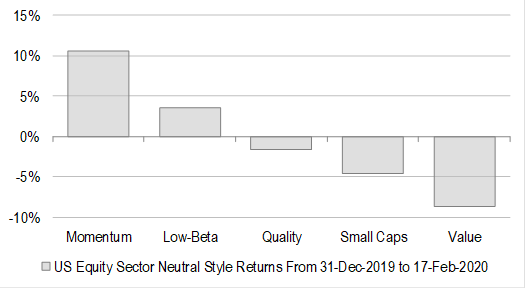

Globally, equities have very much been a momentum and quality story in early 2020. Value factors have badly underperformed, having bounced hard in late 2019. We have seen a very sharp risk-off rotation in alpha terms, even as the market has gained.

Having said this, the momentum and quality rotation has been nowhere near as sharp in Australia, in part because of some dramatic turnarounds in beaten-up stocks during the early stages of reporting season. And for context, we should also note that the value rotation in late 2019 was nowhere near as sharp in Australia as it was abroad.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.