That prevented the Australian dollar from launching:

But it was strong against EM:

Gold held up:

Advertisement

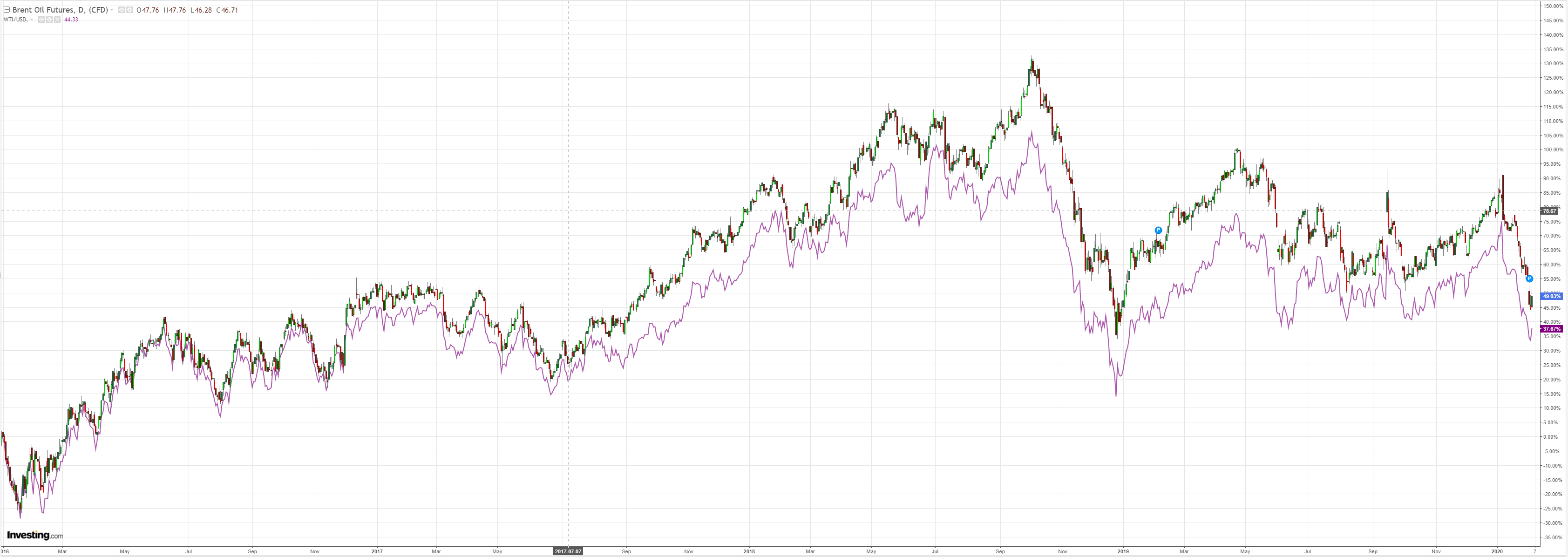

Oil bounced:

And metals:

Plus miners:

Advertisement

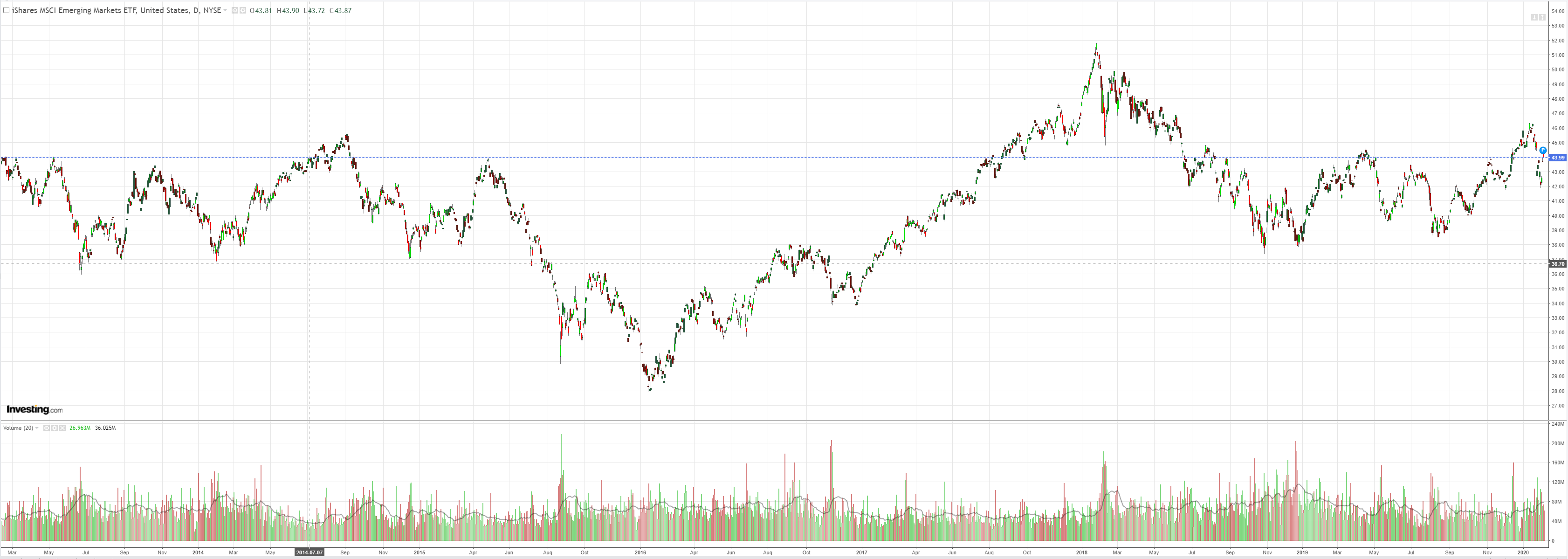

And EM stocks:

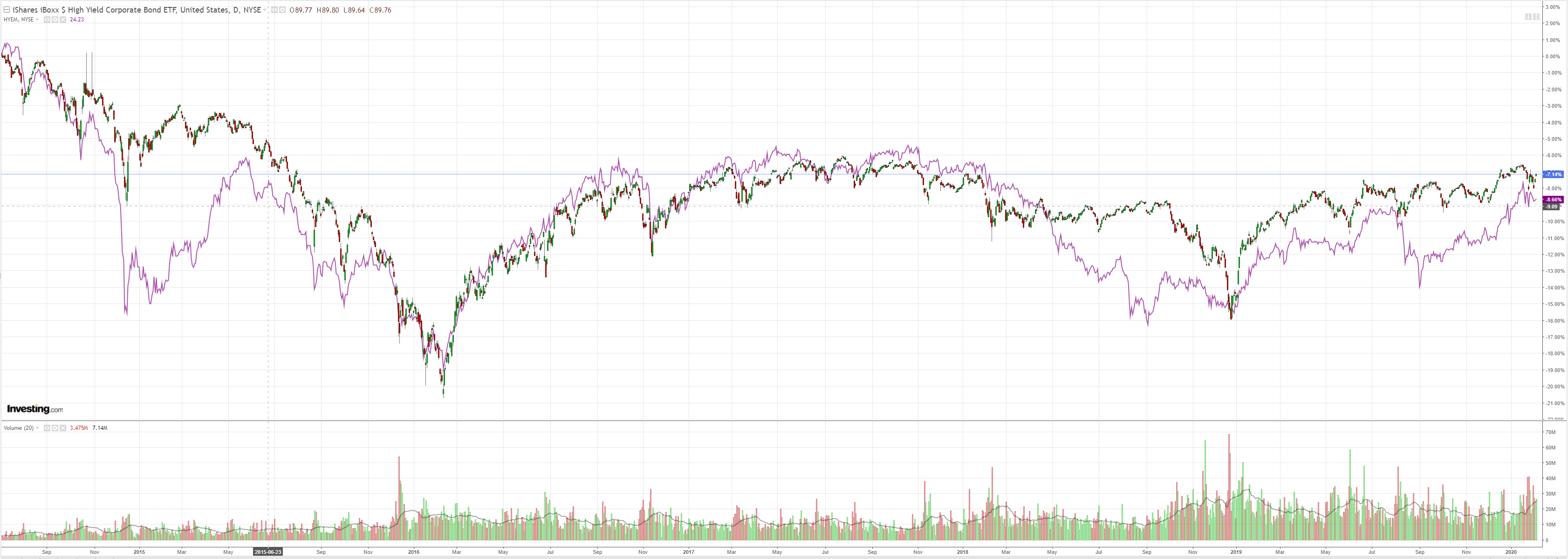

Junk is still fine:

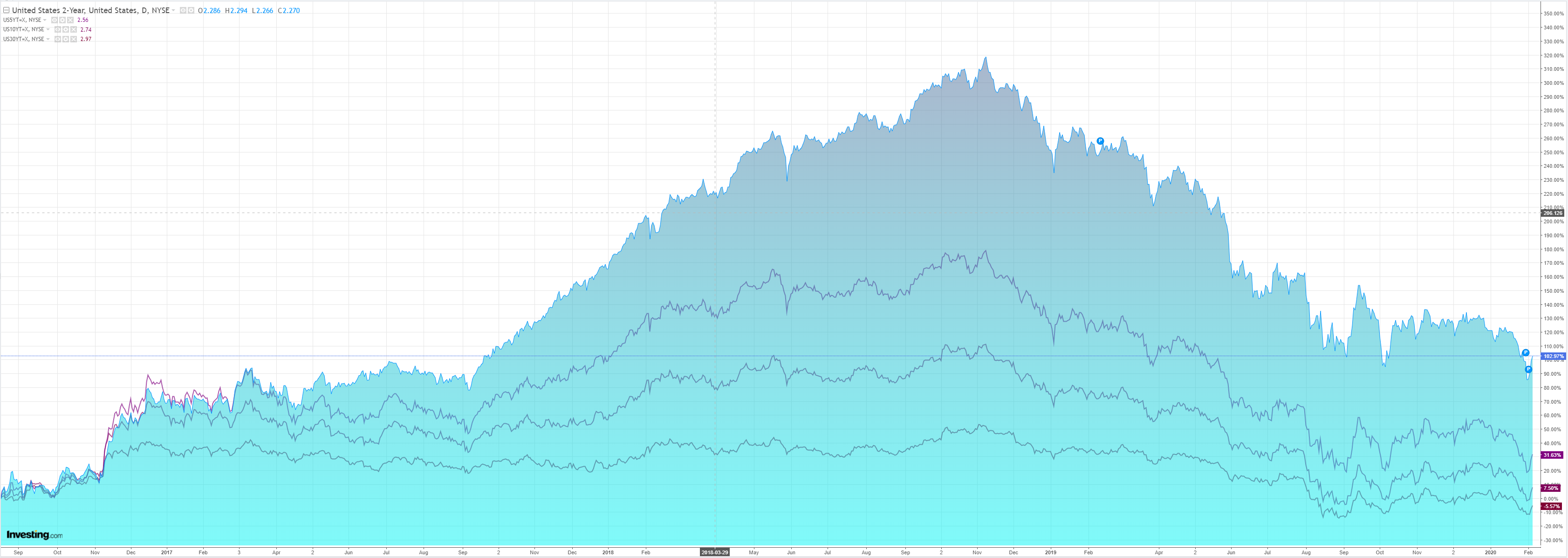

Bonds were hosed for a second night:

Advertisement

Stocks remain unstoppable:

Much of the favourable EM and commosity price action arose from hopes of n-CoV miracle cures. All of which were exaggerated.

The data for the night is wrapped by Westpac:

Advertisement

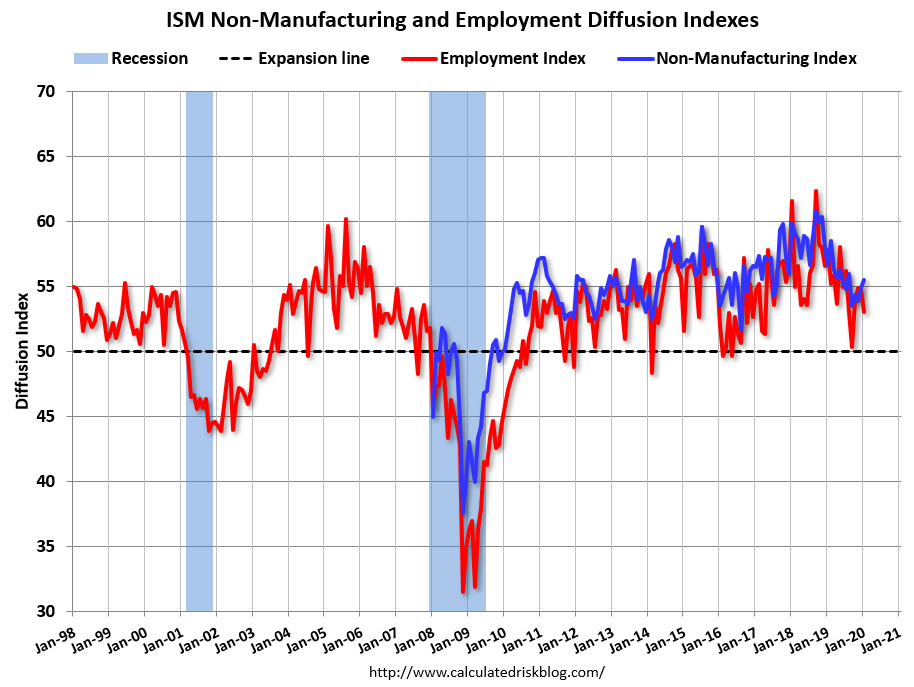

Event Wrap The general lift in risk sentiment was further supported by solid EU and then strong US data.

US Jan. non-manufacturing ISM at 55.5 beat expectations (55.1) and highlighted increasing business activity rising to 60.9 (prior 57.0) and orders climbing to 56.2 (from 55.3)

US Jan. ADP Employment survey posted a much larger than expected rise of 291k (est. 158k) without seeing any notable revisions to the prior strong reading (Dec 199k from initial 202k). The rise caused markets to question current estimates of 160k for Friday’s NFP and boosted US sentiment.

US Dec trade deficit was in line with expectations at –USD48.8bn (est. –USD48.2bn). Confirmation of the narrowing annual trade deficit with China (-17.6% to USD345.6bn) and the first contraction of the overall annual deficit in 6 years (at –USD616.8bn) also supported improving risk sentiment.

Markit’s Final Jan. Eurozone and UK composite PMI’s lifted from their flash readings (51.3 from 50.9 for EZ and 53.3 from 52.4 in UK) and noted improved potential, notably in UK, prospects for 2020.

Eurozone Dec retail sales disappointed as they weakened more than expected. Sales fell -1.6%m/m (est. -1.1%m/m) for a meagre annual rise of 1.3% (est. +2.3%)

Event Outlook

Australian retail sales are expected to partially reverse their 0.9% November gain in December, falling 0.2%. November’s strong gain looks to have largely been driven by ‘Black Friday’ spending and hence was a one off. The summer bushfire emergency may also have affected spending in the month. Real retail sales are expected to rise 0.2% in the December quarter, leaving annual growth at just 0.1%yr.

Australia’s trade balance is expected to widen from $5.8bn to $6.7bn in December on the back of export strength.

President Lagarde of the ECB will speak as will the FOMC’s Kaplan and Brainard, on the economy and payments respectively.

The NMI® registered 55.5 percent, which is 0.6 percentage point higher than the seasonally adjusted December reading of 54.9 percent. This represents continued growth in the non-manufacturing sector, at a slightly faster rate. The Non-Manufacturing Business Activity Index increased to 60.9 percent, 3.9 percentage points higher than the seasonally adjusted December reading of 57.0 percent, reflecting growth for the 126th consecutive month. The New Orders Index registered 56.2 percent; 0.9 percentage point higher than the seasonally adjusted reading of 55.3 percent in December. The Employment Index decreased 1.7 percentage points in January to 53.1 percent from the seasonally adjusted December reading of 54.8 percent. The Prices Index of 55.5 is 3.8 percentage points lower than the seasonally adjusted December reading of 59.3 percent, indicating that prices increased in January for the 32nd consecutive month.

And espeically ADP:

Advertisement

Private sector employment increased by 291,000 jobs from December to January according to the January ADP National Employment Report®. … The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.

…“The labor market experienced expanded payrolls in January,” said Ahu Yildirmaz, vice president and cohead of the ADP Research Institute. “Goods producers added jobs, particularly in construction and manufacturing, while service providers experienced a large gain, led by leisure and hospitality. Job creation was strong among midsized companies, though small companies enjoyed the strongest performance in the last 18 months.”

Mark Zandi, chief economist of Moody’s Analytics, said, “Mild winter weather provided a significant boost to the January employment gain. The leisure and hospitality and construction industries in particular experienced an outsized increase in jobs. Abstracting from the vagaries of the data underlying job growth is close to 125,000 per month, which is consistent with low and stable unemployment.”

As expected, the housing market is injecting resilience into the US economy. It is the place to hide so long as n-CoV gets worse.

Thankfully, it helps offset policy errors in Australia that hold the Australian dollar higher than it should be.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.