Via Westpac:

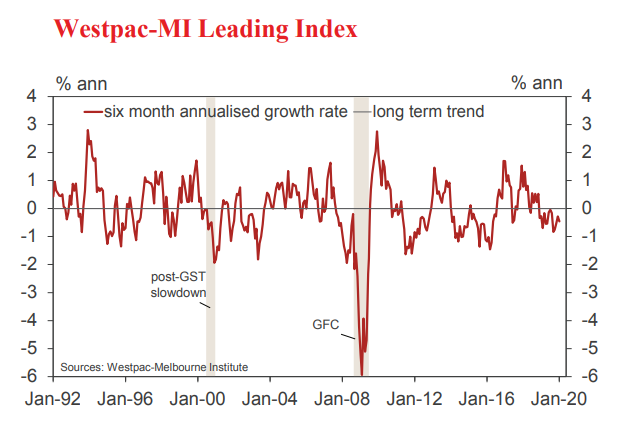

• The six month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, fell from –0.28% in December to –0.46% in January.

The growth rate in the Leading Index remains below zero, indicating momentum will track well below trend. In fact, the January print represents the fourteenth straight month that the Index growth rate has been negative. This has been consistent with the persistent below trend growth

we have seen for the Australian economy.

This update points to weak underlying economic momentum continuing in the first half of 2020 and is consistent with Westpac’s view that underlying growth will remain around a 2% pace in the first half of 2020.

After taking into account our estimate for the impact of the coronavirus and the bushfires in the first quarter of 2020 we have revised down our forecast for growth to 0% in the March quarter from 0.5%. That is now estimated to be followed by a 0.8% (0.5% underlying) in the second quarter as the effects of the virus disruptions dissipate and some rebuild begins in the aftermath of the bushfires.

Growth momentum is expected to lift in the second half as the rebuild from the bushfires comes through.

Overall, despite some significant redistribution of growth through the year we expect that growth in 2020 will hold around 2%, well below trend which we estimate as 2.75%. The Leading Index growth rate has deteriorated over the last six months from -0.16% in August to the current –0.46%. The main driver of the 0.29ppt shift has been a weaker signal commodity prices, measured in AUD terms (–0.5ppts); with some additional drag coming from slower gains in the sharemarket (–0.11ppts); and softer reads around the Westpac-MI CSI expectations index (–0.04ppts) and US industrial production (–0.03ppts).

These negatives have been partially offset by a modest recovery in dwelling approvals (+0.19ppts); a modest widening in the yield spread (+0.14ppts); and slightly better signals around the labour market, aggregate monthly hours worked (+0.05ppts); and Westpac-MI UE

index (+0.03ppts).

The Reserve Bank Board next meets on March 3. We expect the Board will decide to keep rates on hold at that meeting.

However we do expect further reductions in the cash rate over the course of 2020.

We note from minutes of the February Board meeting, which were released yesterday, that the Board discussed a further reduction in interest rates because prospects are for only gradual progress towards the Bank’s inflation and unemployment goals.

The decision to defer hinged largely around the benefits vs the risks of lower rates.

Those risks were around encouraging additional borrowing in the housing market. With housing credit growth benign and little evidence of loose lending practices it seems reasonable that any evidence that the gradual convergence towards the inflation and employment targets is not being achieved will result in further policy easing.

That profile remains Westpac’s view although we recognise that the risks are that this evidence may take more time to emerge than implied by our current forecast that the next cut in rates will be at the April Board meeting.