DXY firmed last night:

The Australian dollar was universally smashed:

Gold was all over:

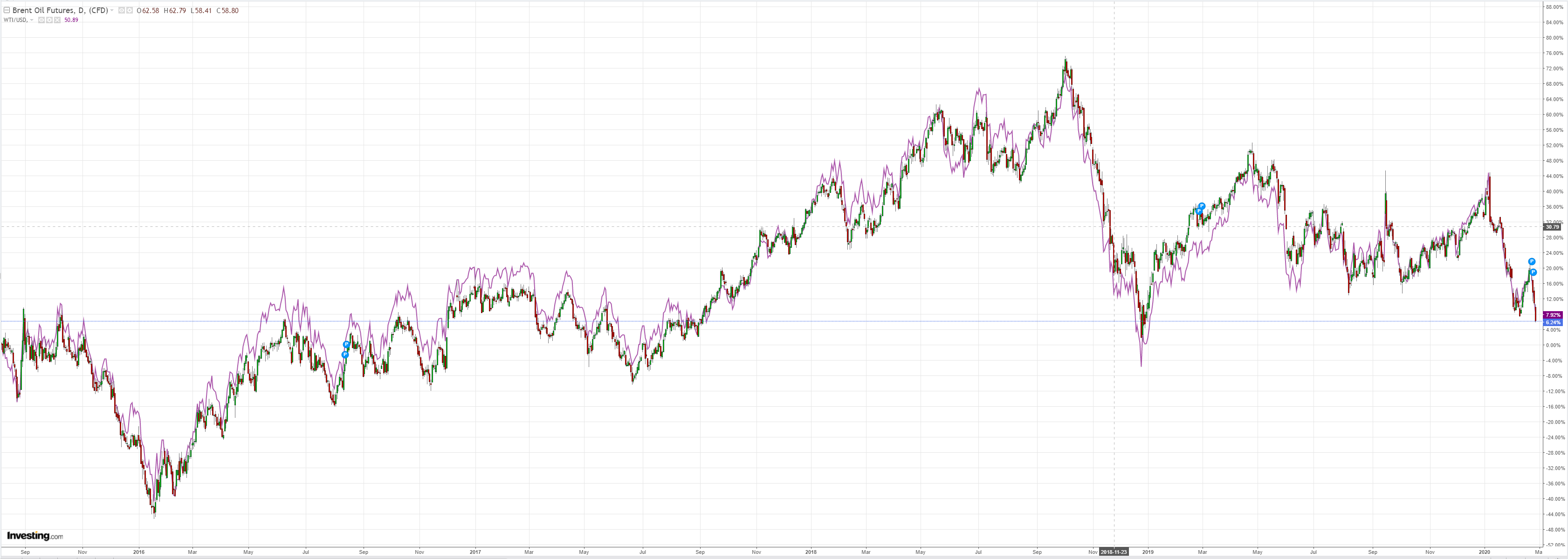

Oil sank:

Metals were mixed:

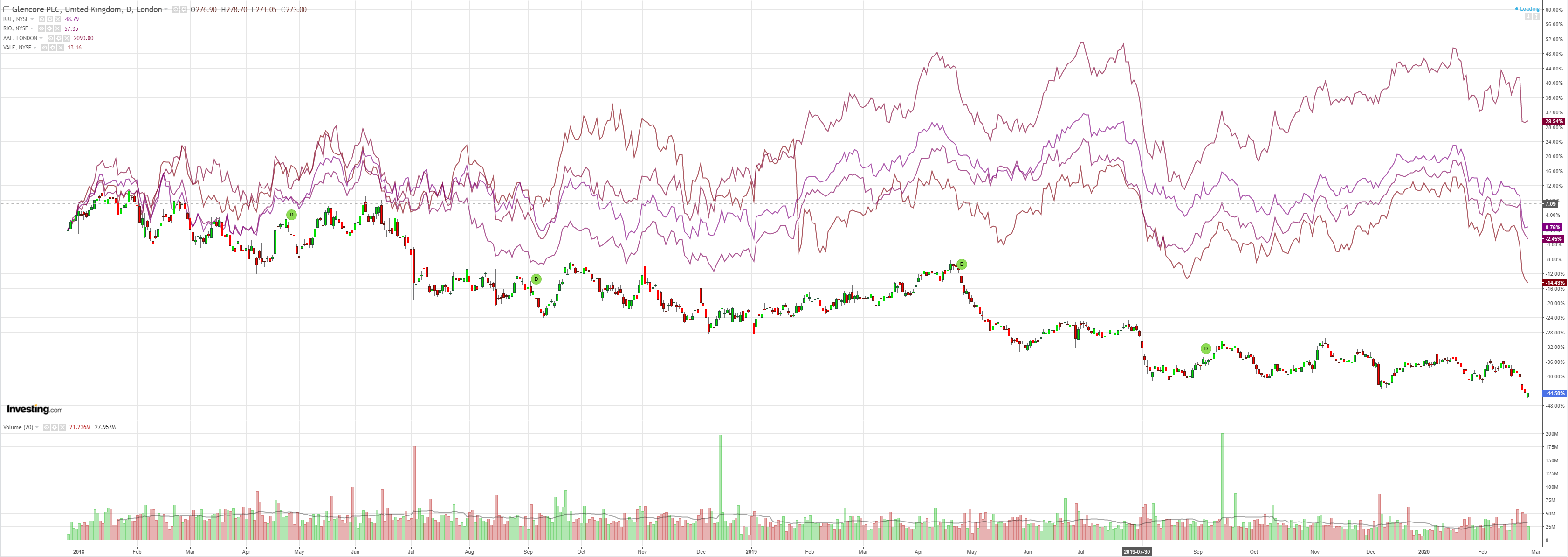

Miners fell:

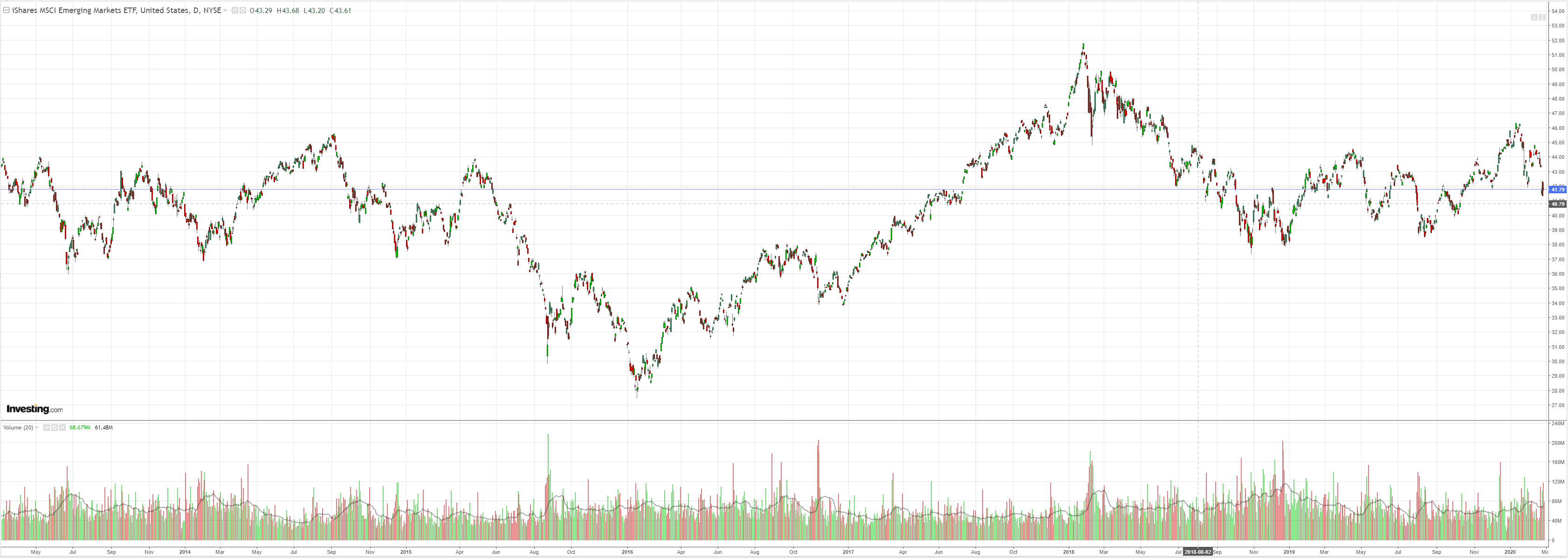

EM stocks held on:

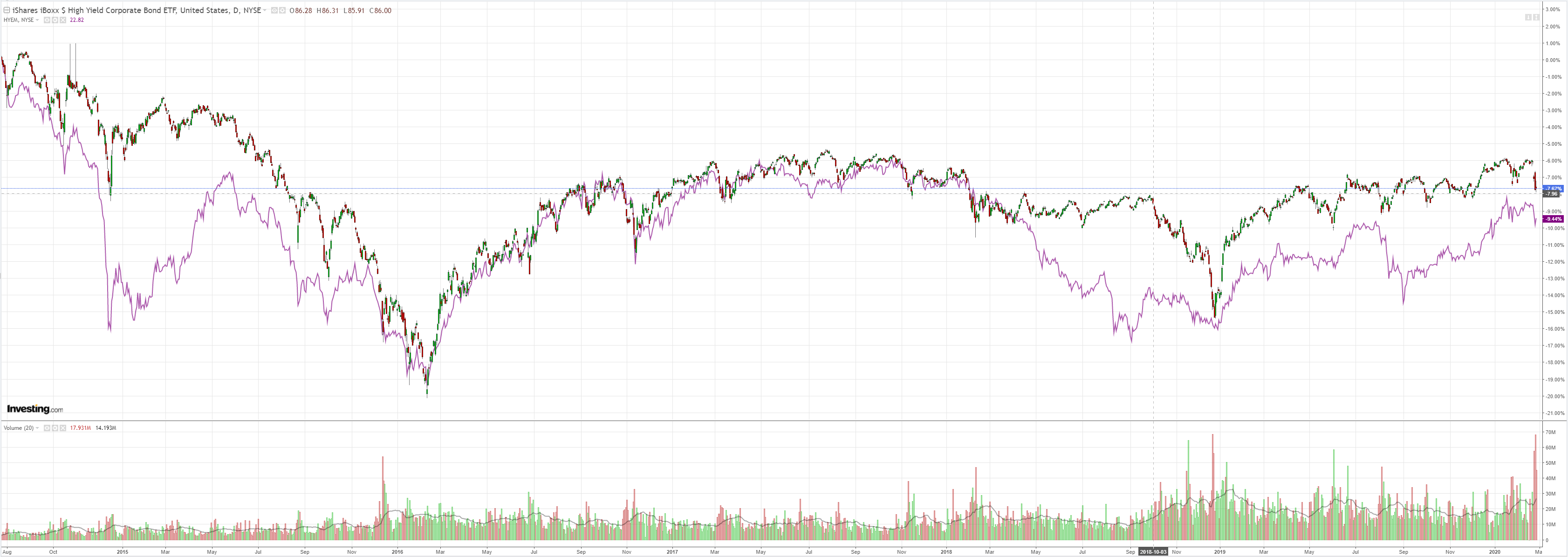

As junk was bid:

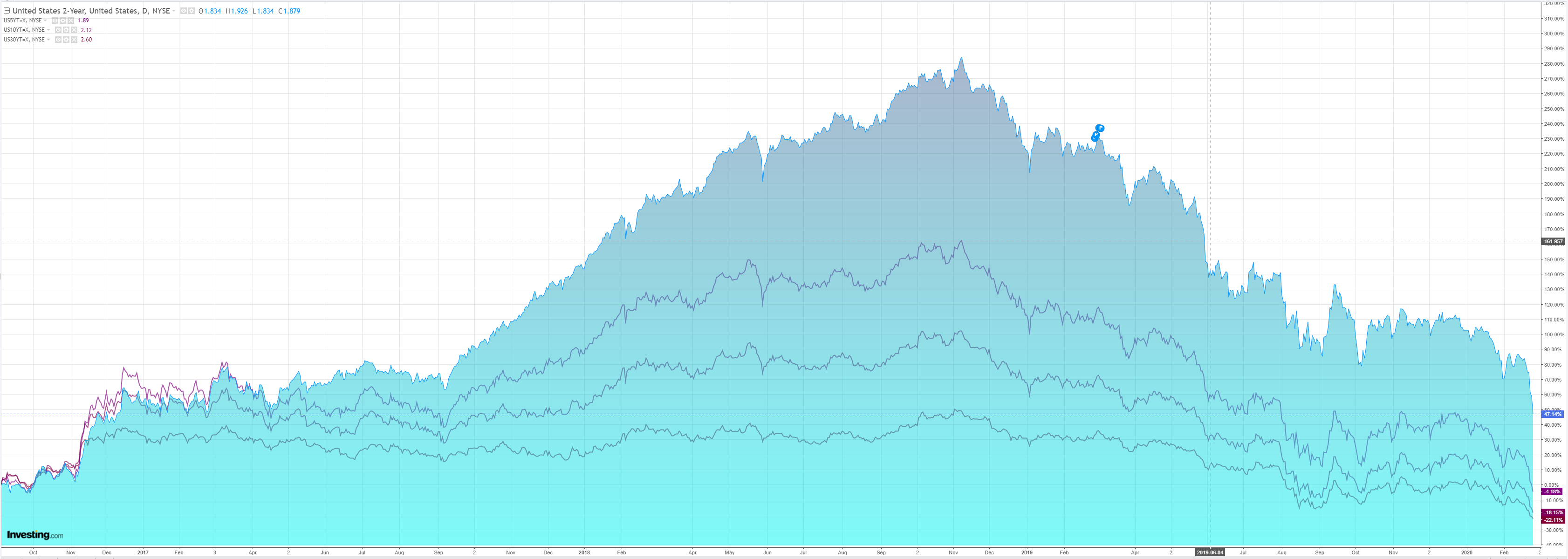

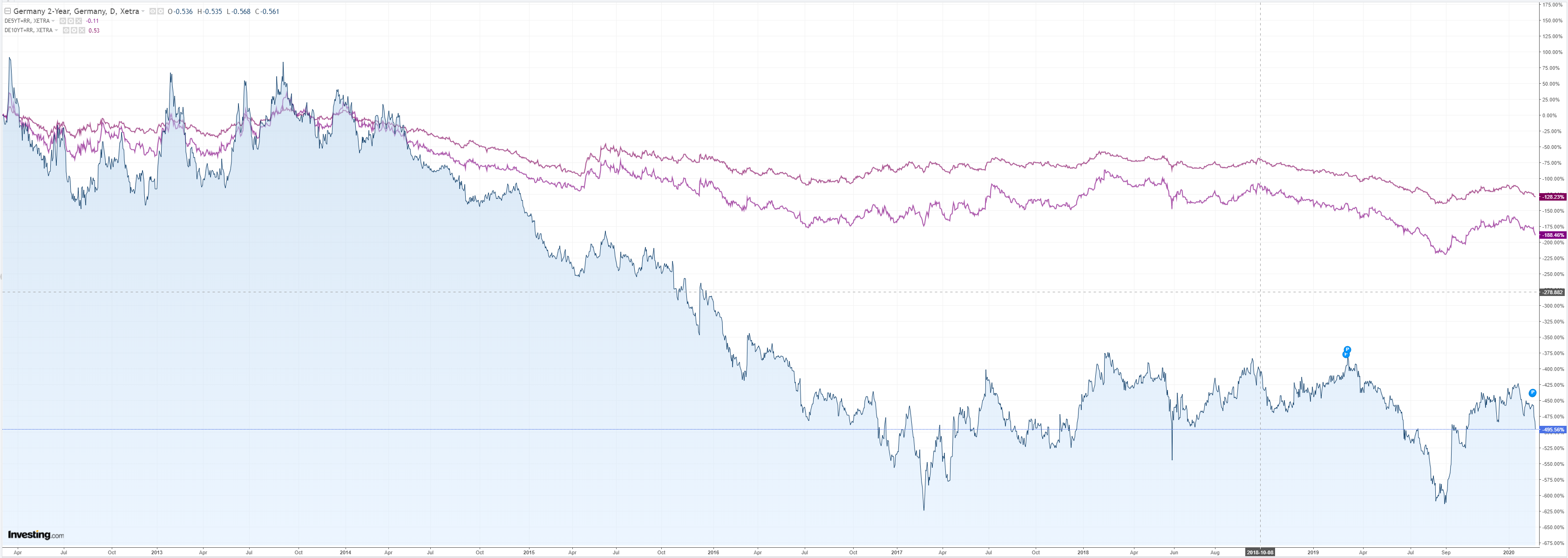

Bonds were all bid:

Stocks were up and down all session to this point:

Westpac has the data wrap:

Event Wrap

Coronavirus update: markets are now focussing on the growth rate in cases outside China. These jumped significantly on 22 Feb, although there was a slight pullback on 25 Feb at 335 new cases (vs 374 on 24 Feb).

US Jan. new home sales were strong, rising 764k (est. 718k, Dec. revised up to 708k from 694k) to the highest levels since Jan. 2007, with record high median prices (+14% y/y to USD348,200).

German Fin. Min Scholz raised the potential that Germany might ease back on its fiscal rules. Media reported that he was in favour of halting, even if temporarily, the adherence to the fiscal brake (which limits State and Federal spending within budgets). This potential boost to State and Federal spending met with mixed responses and some notable potential blocks from key CDU/coaltion members.

EU Chief (post-Brexit) negotiator Barnier heightened the tension around next week’s start of EU/UK talks by stressing the differences in the stances between EU and UK and that a deal this year is “highly unlikely”.

Event Outlook

Australian Q4 private business capex is expected to be broadly flat at -0.2% (market +0.5%). Soft equipment spending is expected to drive this result (f/c -0.5%) given weak business confidence.

Also to be released are Australian capex plans. Estimate 5 for 2019/20 capex is expected to print 1% higher than Estimate 5 a year ago (f/c $119bn), while Estimate 1 for 2020/21 is expected to be 2% higher than Estimate 1 a year ago (f/c $94bn).

In New Zealand, the January trade balance is expected to print at -$800m (market -$549m), led by a rebound in imports after a weak December. The ANZ business confidence survey follows December’s update which rebounded sharply, February’s edition likely to capture some of the coronavirus impact on sentiment.

The Bank of Korea is due to make their February policy decision. Given the sharp increase in uncertainty for the short to medium-term outlook, forecasters now expect the 7-day repo rate will be cut by 25bps.

In the Euro Area, January M3 money supply will be released (market +5.3%yr) alongside credit data. Euro Area economic confidence meanwhile has been forming a base well below 2018 highs, though COVID-19 is a clear risk for February and coming months.

Turning to the US, the second estimate of Q4 GDP is expected to show little to no change from the first at 2.1%, while January durable goods orders will likely provide further confirmation of the weak underlying investment trend. Finally, the Federal Reserve’s Evans will speak in Mexico City.

For forex, the race is on for which major economy suffers soonest and most from the COVID-19 shock.

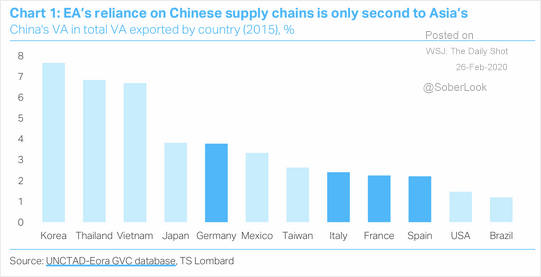

Europe is more exposed via a demand shock to exports plus the supply chain shock:

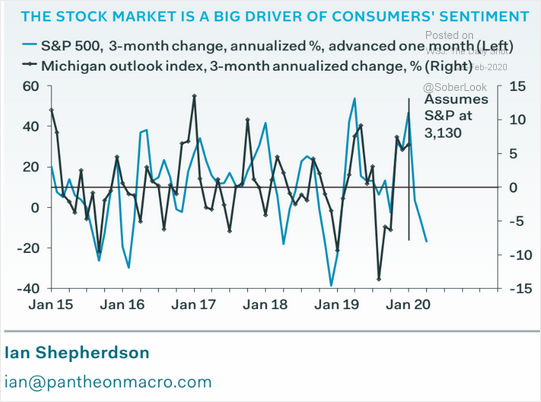

The US is more exposed via the oil patch and consumer confidence as stocks give way:

I still think that Europe will win the race into recession. It has materially less economic momentum and considerably more cononavirus, with much greater difficulties in shutting down borders and other containment measures.

That means a lower EUR, higher DXY, and lower AUD.