DXY is up and away as expected as EUR crumbles:

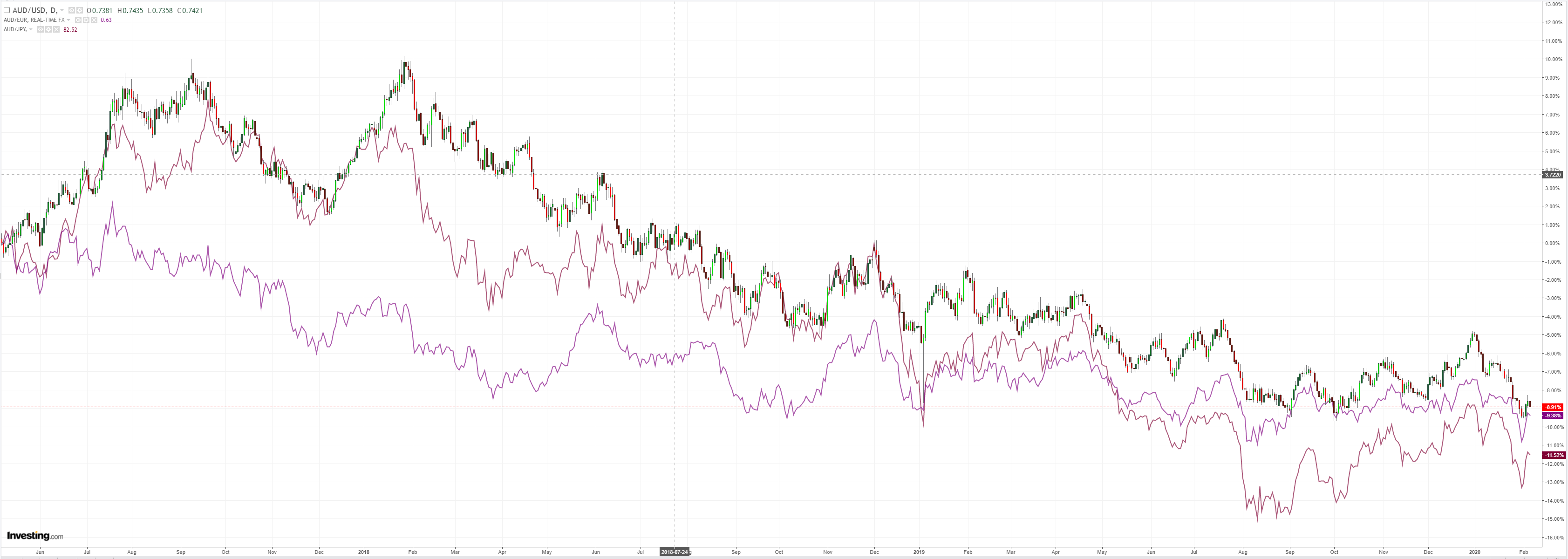

The Australian dollar was squashed aginast DMs:

EMs were hit even harder:

Gold has a virus chaos bid:

Oil is trying to bottom:

Metals too:

Miners fell:

And EM stocks:

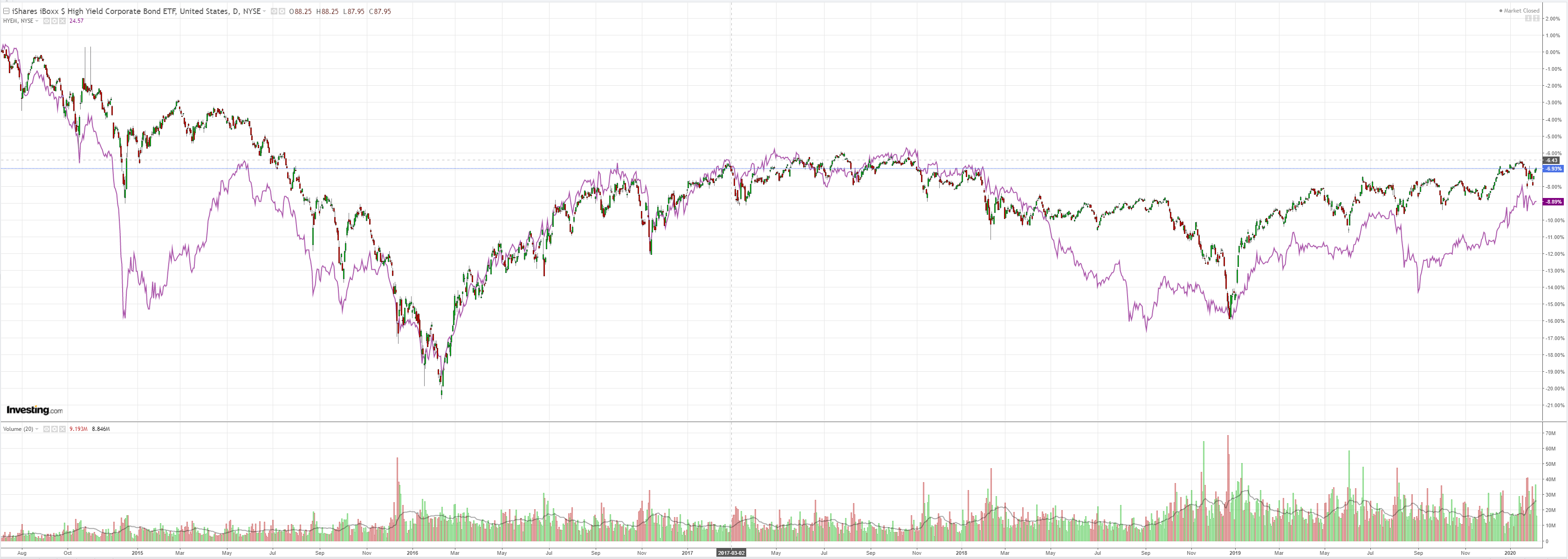

Junk is still fine:

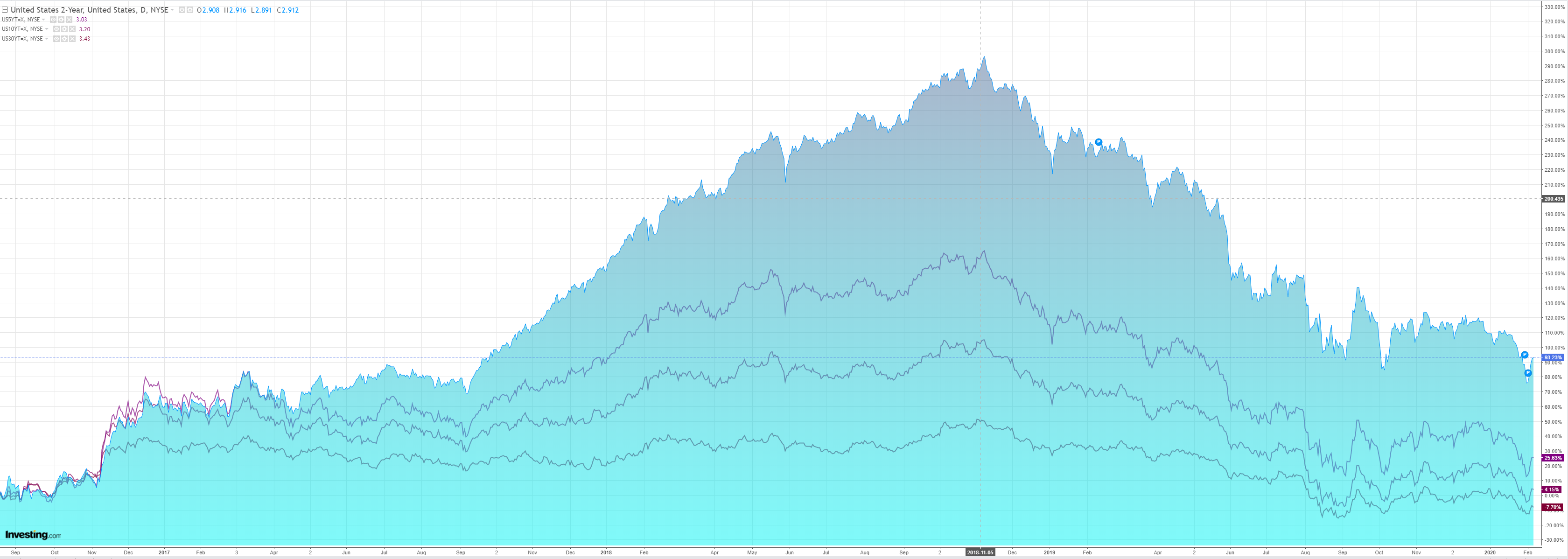

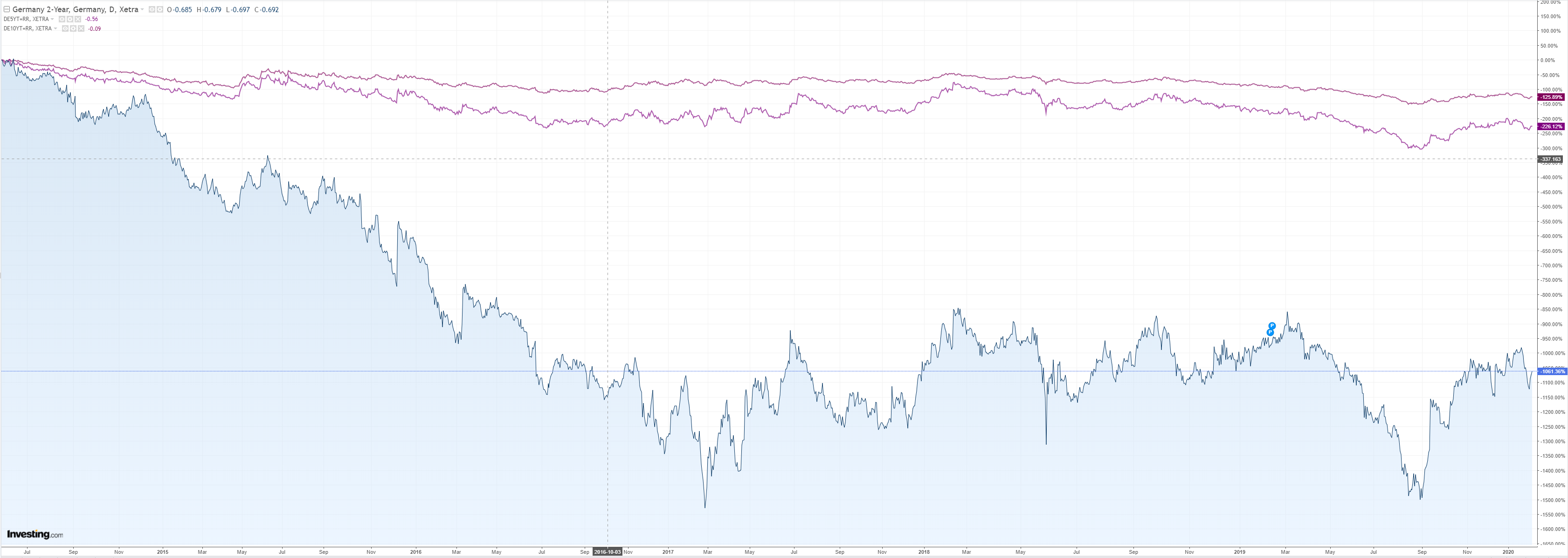

Bonds were lightly bid:

As stocks put on carefree new highs:

Westpac has the wrap:

Event Wrap

China will halve tariffs on $75 billion of imports from the US on 14 Feb, reciprocating US action as part of the phase-one trade deal.

Event Outlook

NZ inflation expectations survey is released by the RBNZ today. The key 2-year ahead measure fell to 1.8% – a two-year low – in Q4.

The RBA Governor will appear before the House of Representatives Economics Committee this morning from 9:30am to discuss the outlook for economy. Risks to the central view are again likely to be the focus. The February Statement on Monetary Policy will be released at 11:30am, and will include the full set of updated forecasts noted in the decision statement and Governor Lowe’s speech.

China trade data for Jan is out.

In the US session, the focus will be nonfarm payrolls and hourly earnings. We expect a 170k monthly gain for payrolls (consensus is 163k) and a 0.3% rise in hourly earnings in the month. While the January ADP print surprised to the upside, often it proves an inaccurate lead for the BLS release.

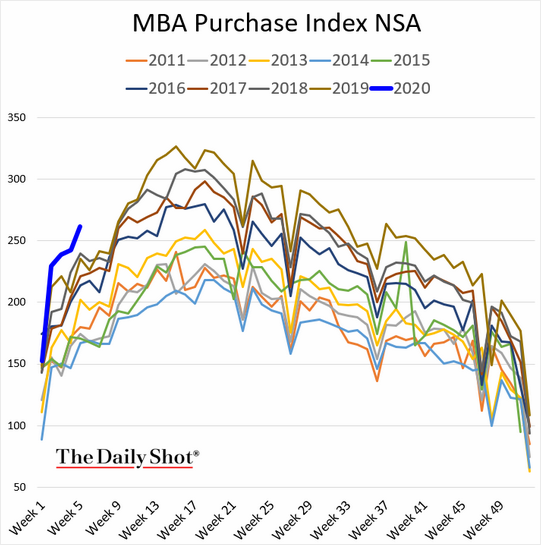

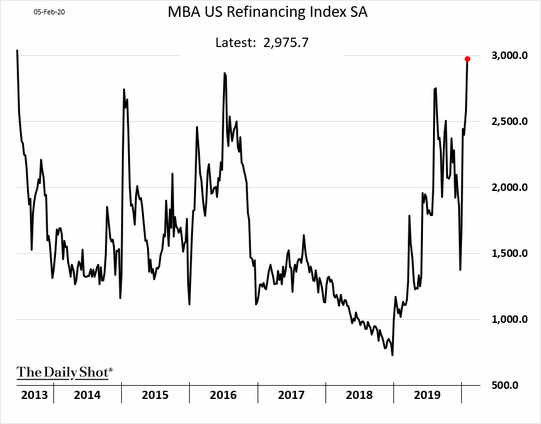

The US housing boom rolls on, stoked even more by the coronavirus drop in interest rates:

Supporting the consumer. While European household struggles on:

Awaiting a coronavirus belting for its exports machine.

There is no end is sight for USD dominance unless China contains the virus.

The reverse remains true for Australian dollar weakness.