Markets are starting to come apart and some real weirdness is appearing. DXY got hammered last night as the EUR soared:

The Australian dollar took off versus USD but cratered vs EUR:

EMs were belted:

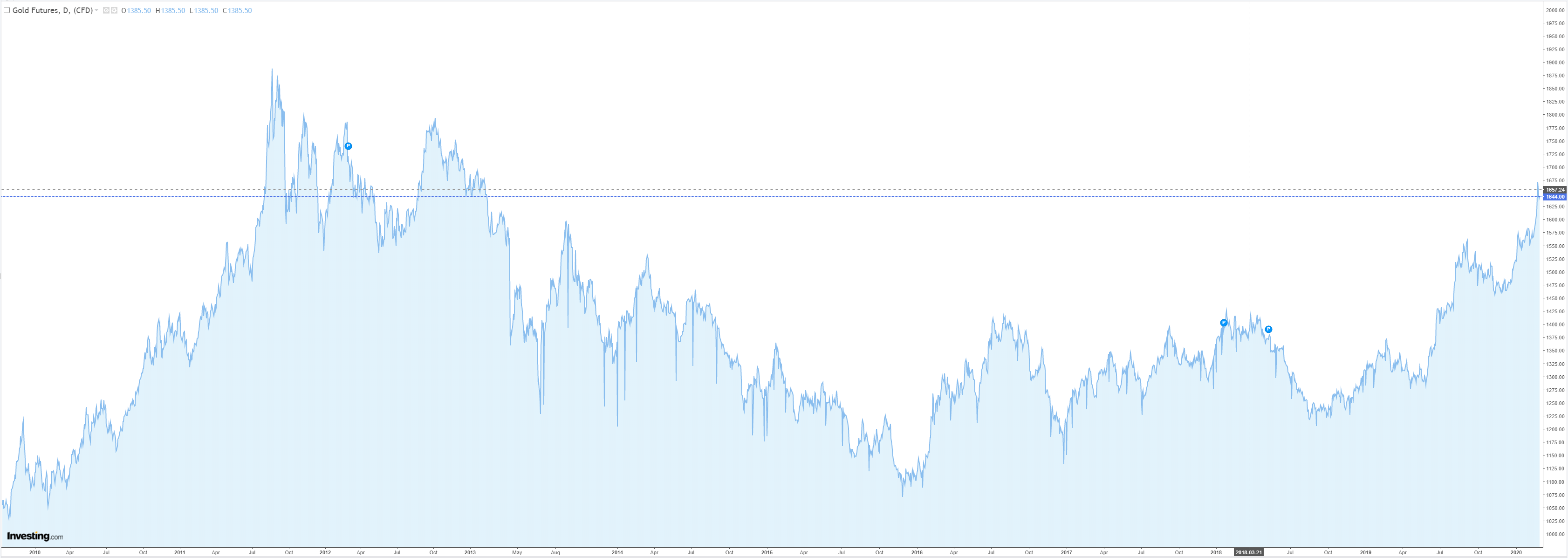

Despite DXY weakness, gold can’t run on:

Oil was drilled again. I think the 2016 is the target:

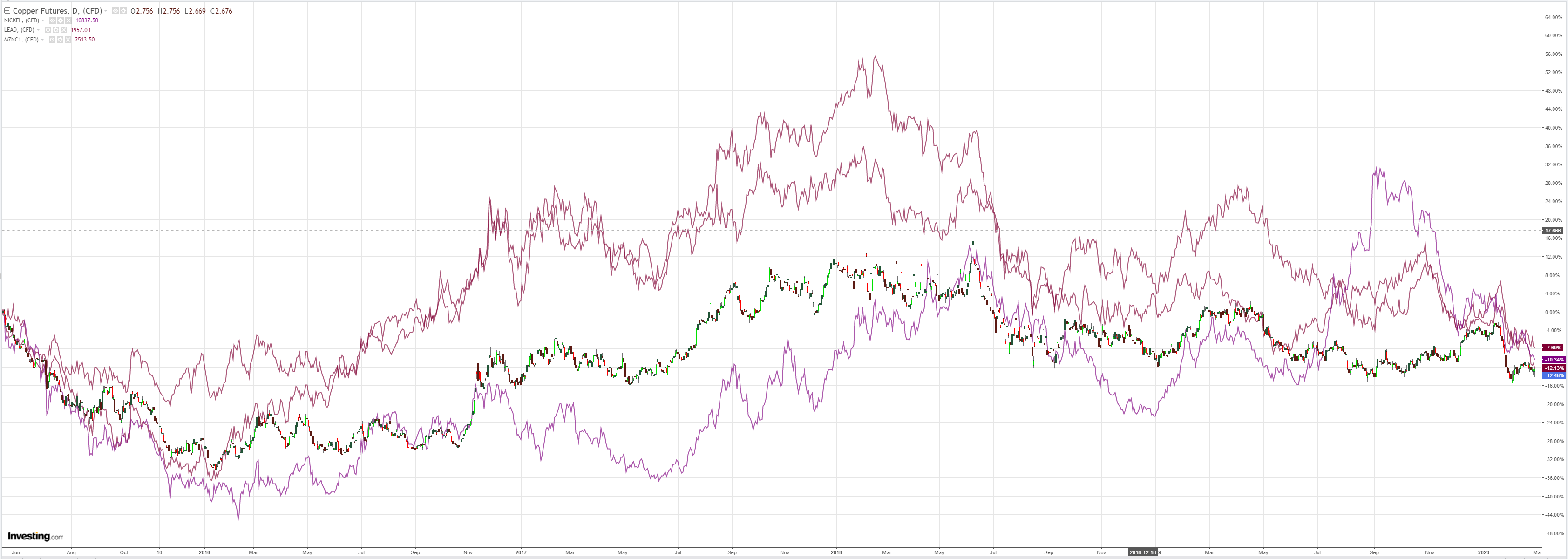

Base metals fell except copper. Say what?

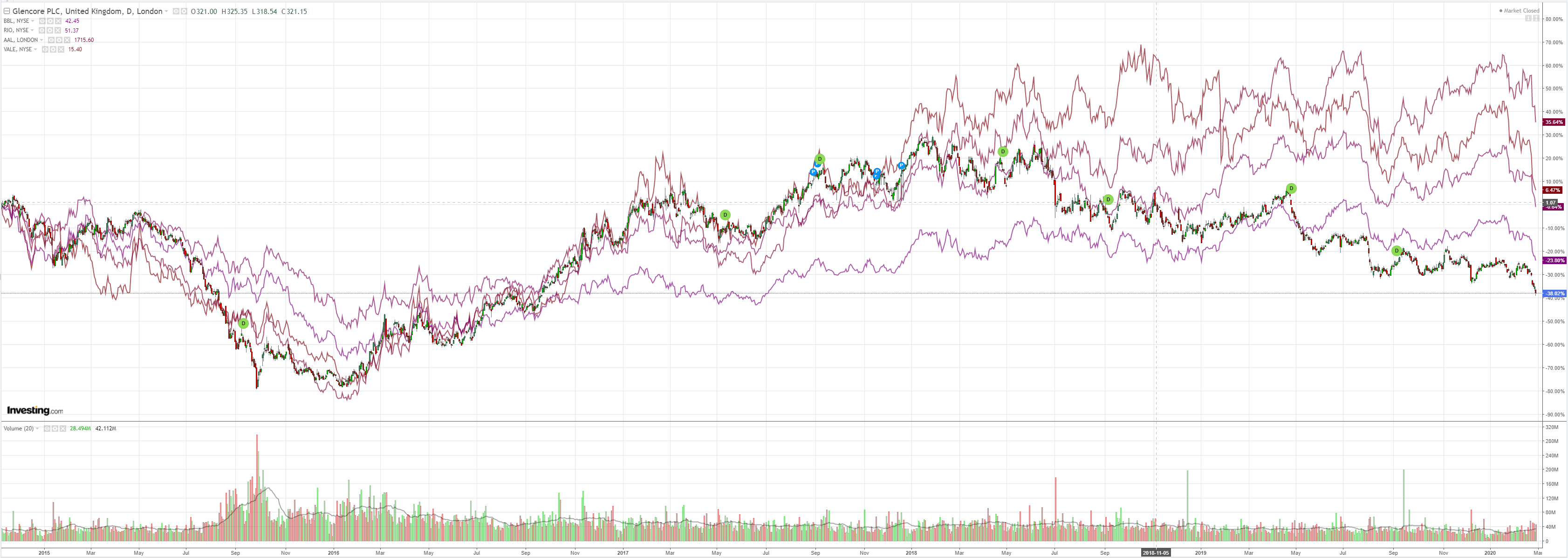

Miners were smashed:

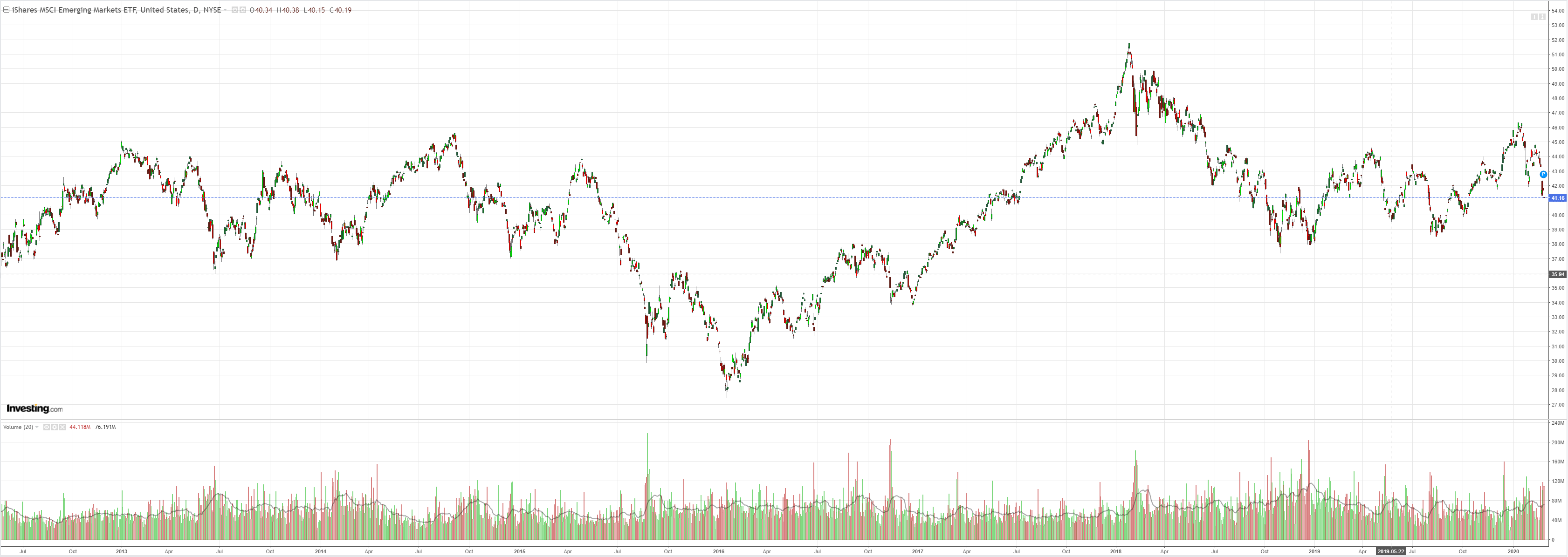

EM stocks gapped lower:

Junk has woken up in free fall:

Treasuries are on fire:

Bunds too:

Perversely the Aussie curve steepened as long bonds sold:

Stocks were pulverused but, worrying, haven’t even unwond their post-trade deal global recovery trade yet:

Westpac has the data wrap:

Event Wrap

Coronavirus update: The growth in cases outside China jumped significantly on 26 Feb to 569, from 335 on 25 Feb, marking a new peak. The US announced the appointment of a key Coronavirus Response Coordinator to guide US actions around the virus, and Pelosi and Pence stated that bi-partisan funding for responses was close to being agreed.

The 2nd update of US 4Q GDP was unchanged at 2.1% ann., but the core PCE fell to 1.2% from 1.3%. The non-defence/ex-air component of Jan. durable goods orders beat expectations at +1.1%m/m (vs 0.0% expected). US Jan. pending home sales rose +5.2%m/m (est. +3.0%). Kansas City Fed’s survey rose to +5 (est. unch at -1).

In the Eurozone, EC consumer confidence rose from 102.6 to 103.5 (vs 102.8 expected), suggesting little concern about the initial outbreak of the coronavirus pandemic.

Event Outlook

Australian January private sector credit is due, and expected to increase by 0.2%. Although this extends the soft trend of 2019, a gradual rise is anticipated in the coming months as the housing credit cycle builds momentum.

In New Zealand, February ANZ consumer confidence will be released, and is likely to be challenged by negative headlines surrounding COVID-19.

Indian Q4 GDP will be released, and expected to grow at 4.7%yr. The slowing pace of growth reflects broad-based economic weakness, but policy should provide some support.

In the Euro Area, preliminary estimates of February CPI are expected to print at 1.2%, well below the ECB’s inflation target.

Turning to the US, January personal income is expected to increase by 0.3%, reflecting solid wage gains but a softening of non-wage income. In addition, January personal spending is expected to grow by 0.2% as consumption slows after a period of outperformance. The January PCE deflator is expected to edge up by 0.2% to 1.8%, the core measure up 0.1% to 1.7%. Finally, the Federal Reserve’s Bullard will speak on the economy and monetary policy.

On Saturday 29 Feb, the market anticipates that China’s February manufacturing PMI will tumble by 5 to 45, a direct result of the impact of COVID-19. This will be accompanied by the February non-manufacturing PMI, which is expected to weaken by 3.1 as the services sector bears the hit to consumption.

There are a bunch of strange dynamics this morning. The major break is the strength of the EUR. As the meltdown gets more intense it is now behaving like the safe haven of choice. This is perhaps not that surprising given its interest rates never got off the floor in this cycle whereas the US did. The spike looks an awful lot like an unwinding carry trade. Over the last year or more there was a spike in EUR cross-border financing:

So, that raises a challenge for the Aussie versus the USD as DXY falls with EUR strength. Though it is important to remember that AUD/USD has already been one of the weakest crosses of the year so we are not talking regime change here.

Second, why gold and the Aussie long bond unerperformed is a mystery. Perhaps, as in the GFC, gold finds itself to some extent liquidated for liquidity. The Aussie long bond sometimes underperforms overnight then corrects during local trade. If the weakness persists, we’d have to wonder if capital flight from Australia isn’t suddenly an issue. The opposite is also possible. That as the virus goes global but gets less evere in China, the world sees Australia as coming out of this first. Good luck with that with the winter ahead!

Interesting stuff. I guess you can’t have a crisis without throwing up a few surprises. They’ll keep coming too. Markets have barely discounted a thing.

David Llewellyn-Smith is Chief Strategist at the MB Fund which is very conservatively positioned for coronavirus risks including a falling Australian dollar.