The Australian dollar held at the cliff edge versus DM:

But fell against EMs:

Advertisement

Gold flamed out:

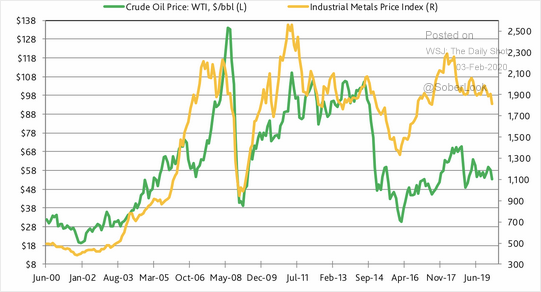

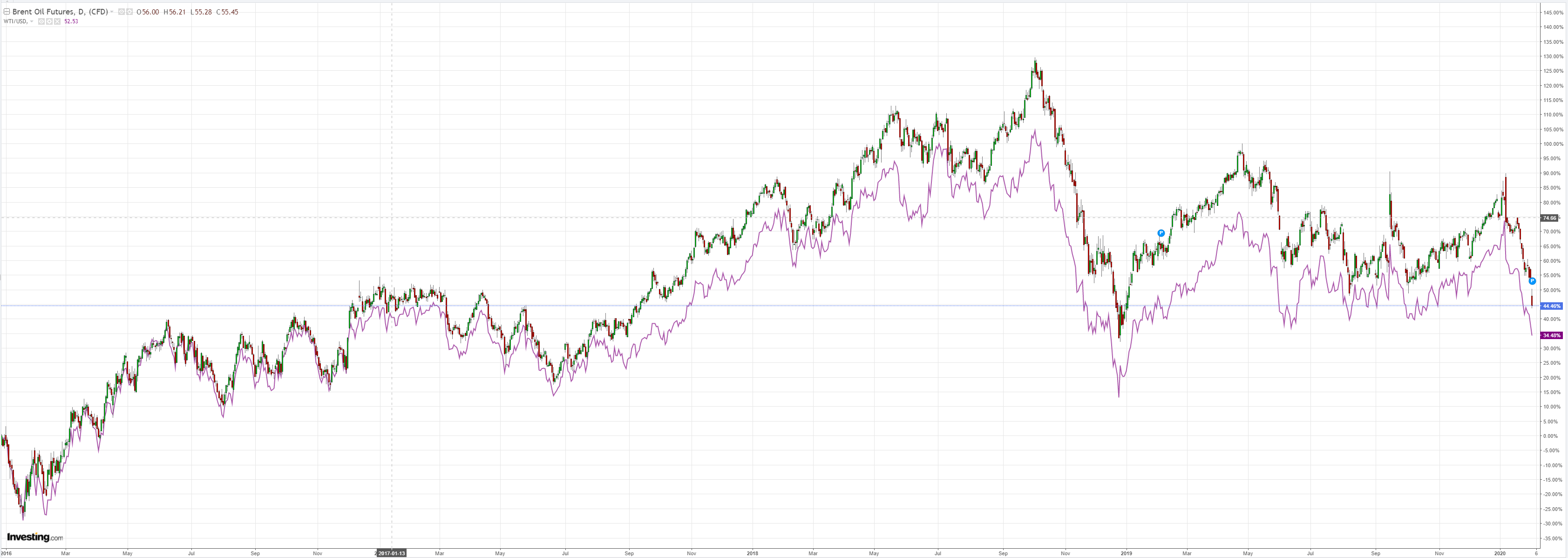

Oil is burning:

Metals too:

Advertisement

Miners were mixed:

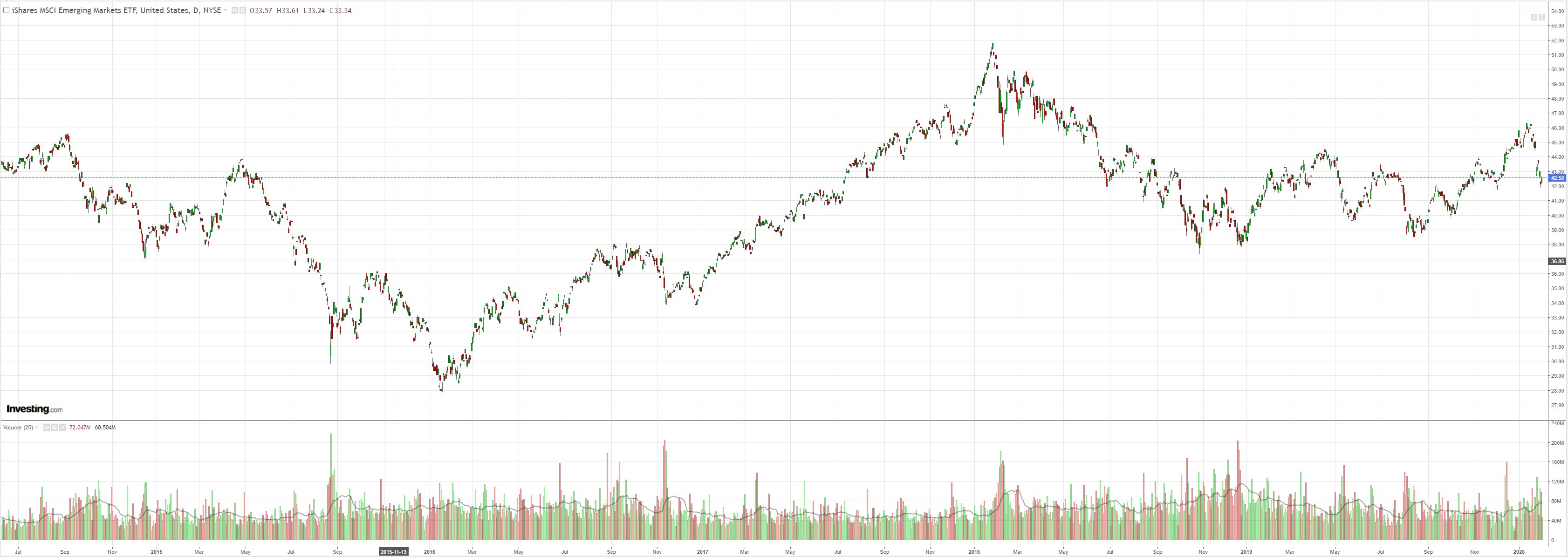

EM stocks pushed back:

Junk fell but is still OK:

Advertisement

Treasuries sold:

Bunds were bid:

Aussie split the difference:

Advertisement

Stocks roared back:

There is no virus! And another thing, there is no virus!

Westpac has the data wrap:

Advertisement

Event Wrap

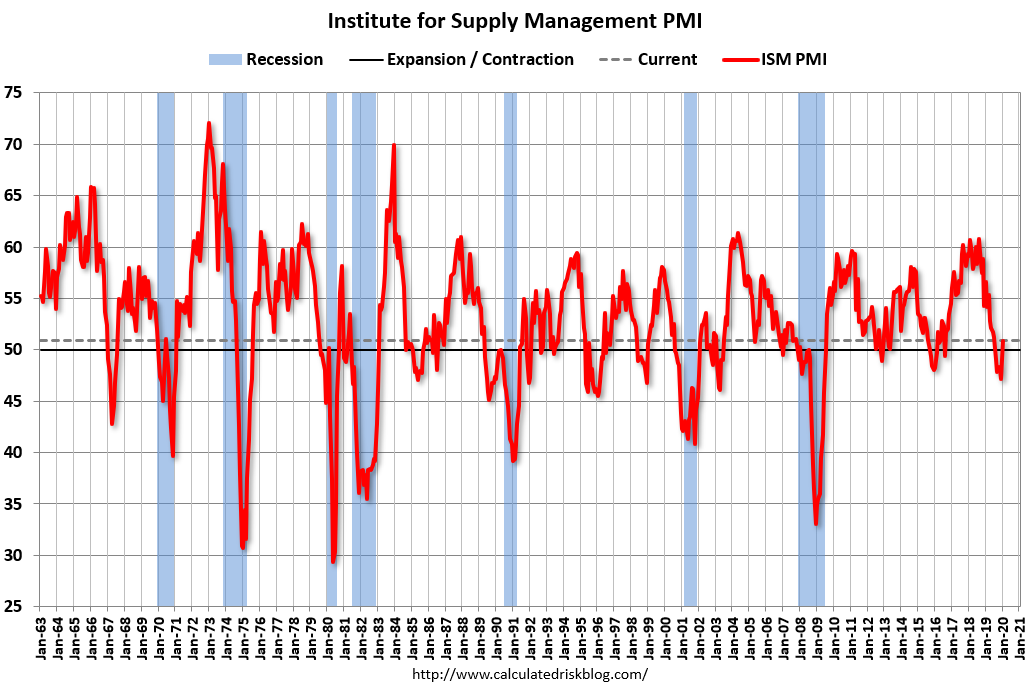

US Jan. manufacturing ISM was notably firmer than expected at 50.9 (est. 48.5, prior 47.8), with gains in most components, notably new orders at 52.0 (prior 47.6) and prices paid (53.3, prior 51.7). The employment component remained low at 46.6 but improved from 45.2.

Eurozone Jan. final PMI edged up to 47.9 (flash 47.8), reflecting slight improvements across the majority of national PMI’s. UK Jan. final PMI also rose to 50.0 (flash 49.8).

UK PM Johnson set out a staunch stance in front of negotiations with EU on trade and their future relationship, highlighting that the UK would walk away from talks if negotiations could not progress, yet hoped for a positive and mutually advantageous outcome. The EU demanded tight adherence to current regulation alignments and a “level playing field”.

Updated coronavirus statistics show confirmed cases total 17,488 worldwide (17,302 in China), of which 13% are in critical condition, and deaths total 362 (361 in China).

Event Outlook

The RBA is expected to remain on hold at their February meeting given continued robust momentum in the labour market. However, the weak state of domestic demand and sentiment along with the impact of summer’s bushfires and now the coronavirus outbreak, highlight the need for an easing bias and, in time, further policy easing. We expect two 25bps cuts in 2020, in April and August. The February decision will be followed by a speech by Governor Lowe on ‘The Year Ahead’ (Wednesday), his testimony to Parliament and the release of the February Statement on Monetary Policy (Friday).

In the US, President Trump is due to deliver his 2020 State of the Union address. Also worth watching will be the Iowa caucuses to choose a Democratic nominee to contest the election in November.

“The January PMI® registered 50.9 percent, an increase of 3.1 percentage points from the seasonally adjusted December reading of 47.8 percent. The New Orders Index registered 52 percent, an increase of 4.4 percentage points from the seasonally adjusted December reading of 47.6 percent. The Production Index registered 54.3 percent, up 9.5 percentage points compared to the seasonally adjusted December reading of 44.8 percent. The Backlog of Orders Index registered 45.7 percent, up 2.4 percentage points compared to the December reading of 43.3 percent. The Employment Index registered 46.6 percent, a 1.4-percentage point increase from the seasonally adjusted December reading of 45.2 percent.

I expect the US to be the last to succumb to the virus as its housing market booms on crashing mortgage rates, so DXY should stay strong.

Advertisement

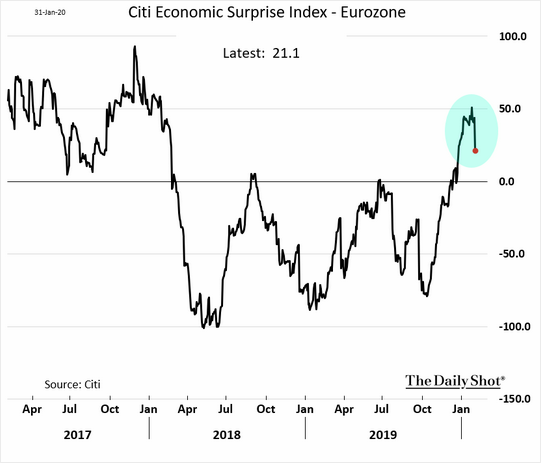

Certainly stronger than EUR which is badly exposed to China and is already weak:

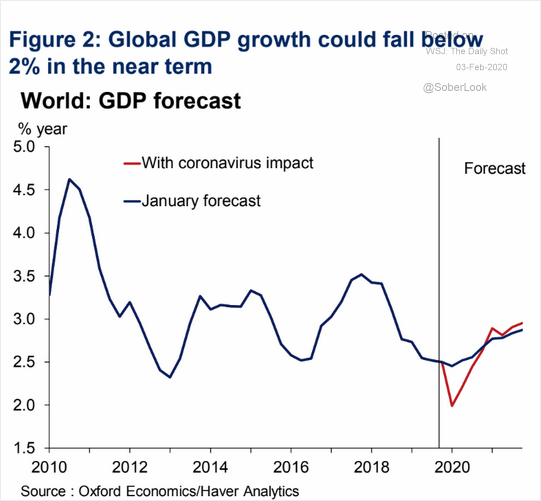

Falling global growth is also bad for the EUR:

Advertisement

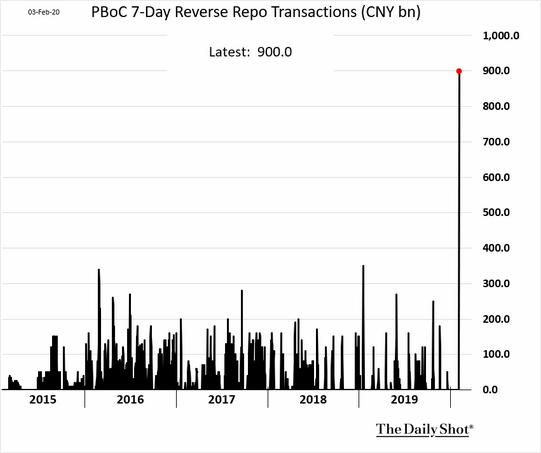

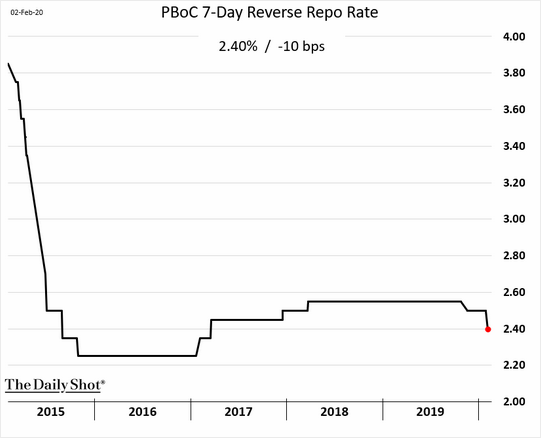

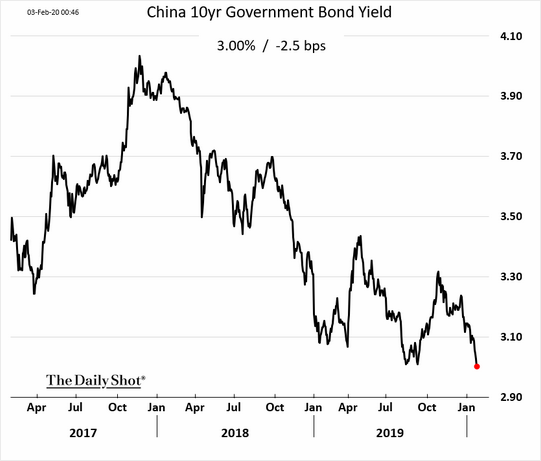

As China throws everything at it:

But not as bad as for Australia where the coronavirus hammer falls hardest. Moody’s is now mulling 2016 lows for commosites:

Advertisement

Which is a very good idea since that is where a Chinese pandemic will take them.

The Australian dollar will be destroyed in that event.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

{kind=link}