DXY looks like it’s primed for breakout as EUR free falls:

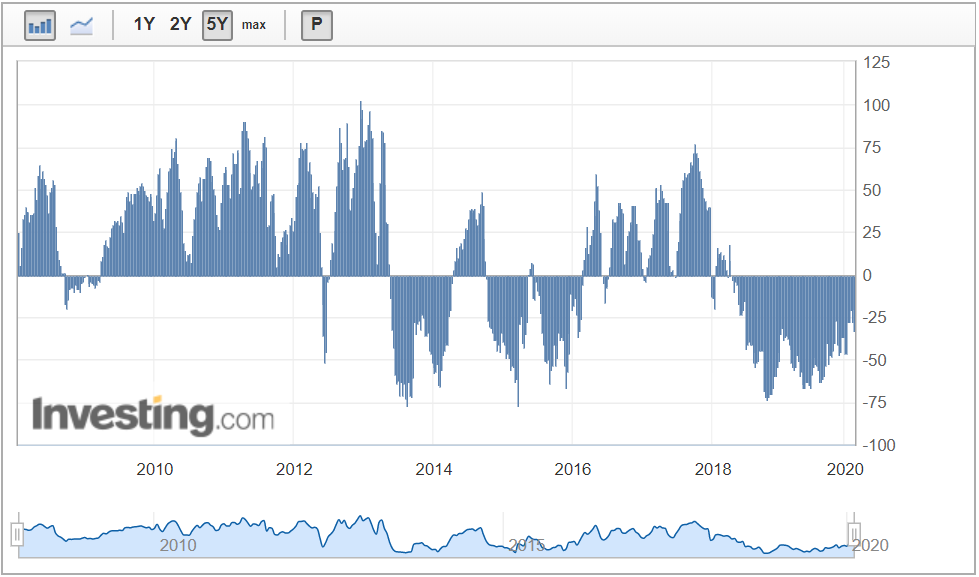

The market is not especially short EUR. There’s room to fall:

The Australian dollar was universally panned Friday night:

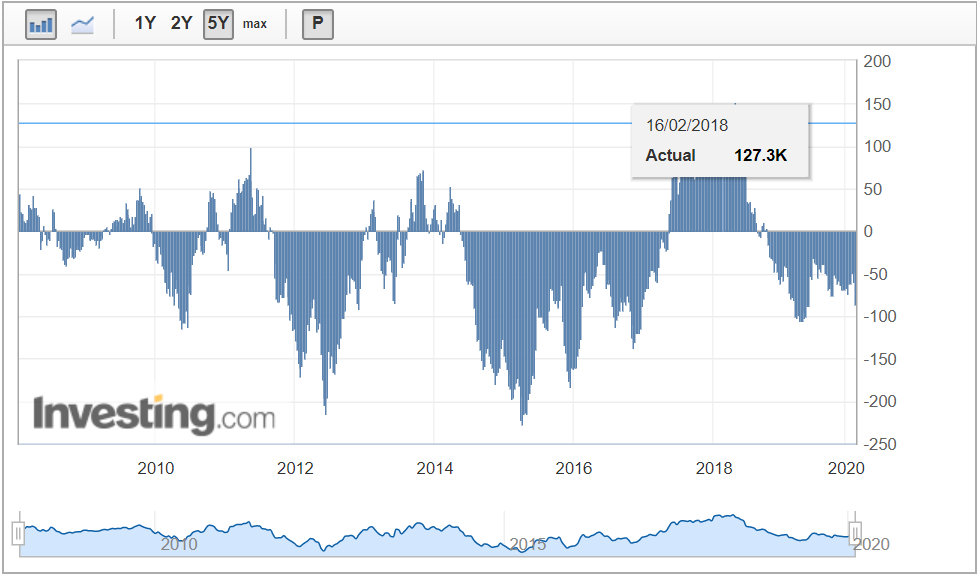

It alos has rooom to fall further in terms of CFTC positioning:

Gold also looks primed for higher:

Oil is trying. Too early for mine but the contango is helping:

Metals fell:

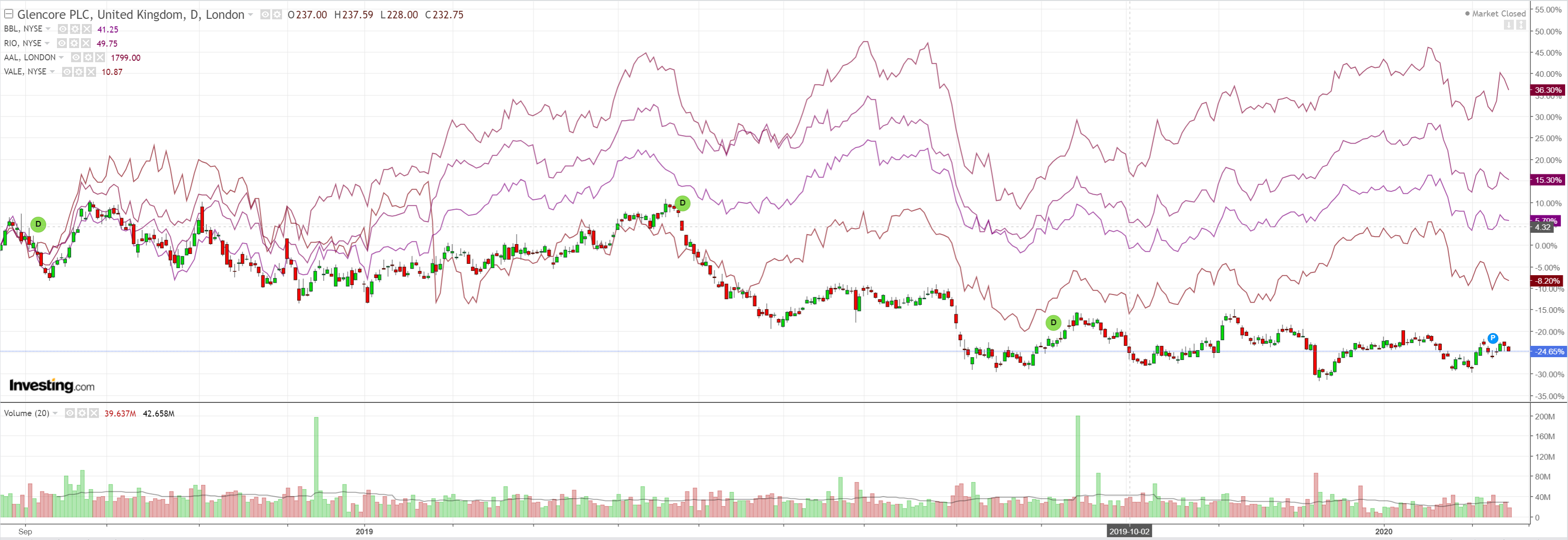

Miners too:

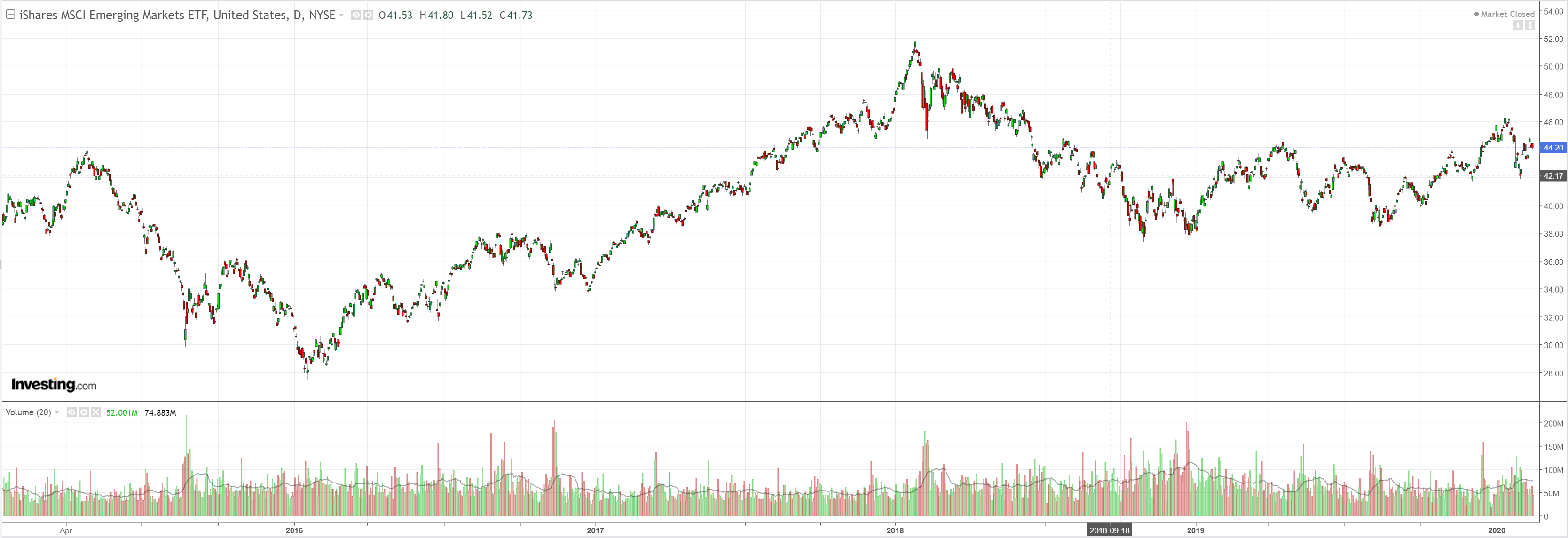

EM stocks fell:

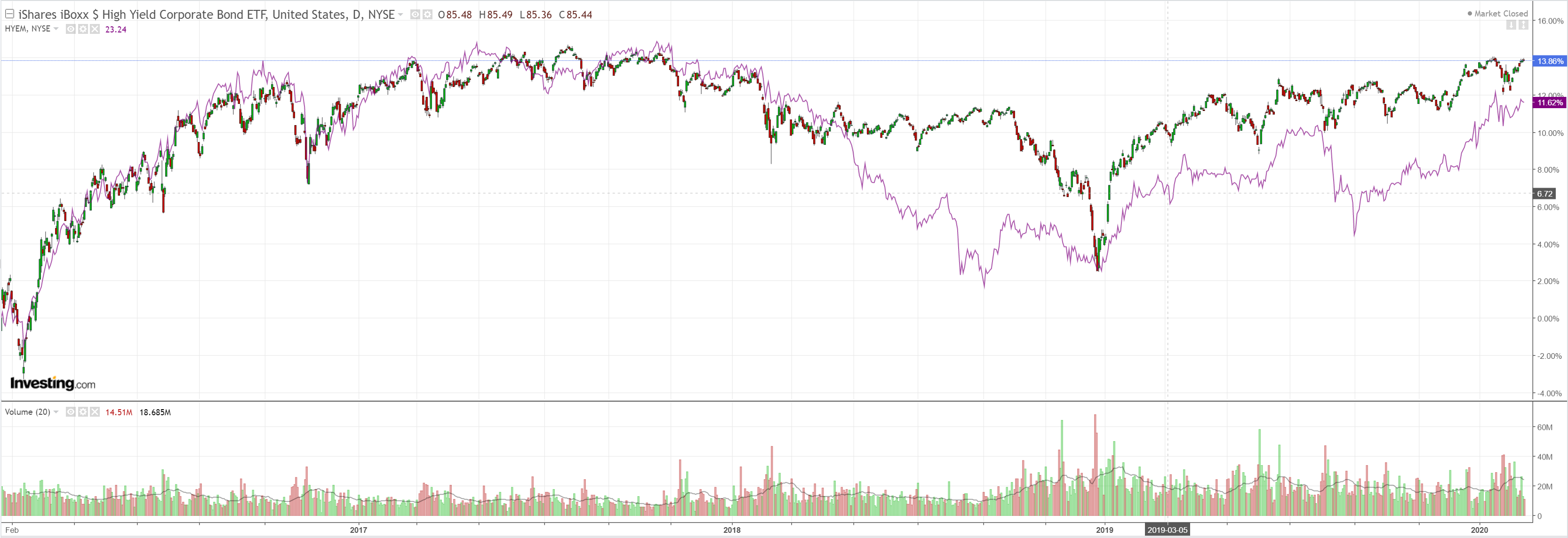

Junk remains impeturbed:

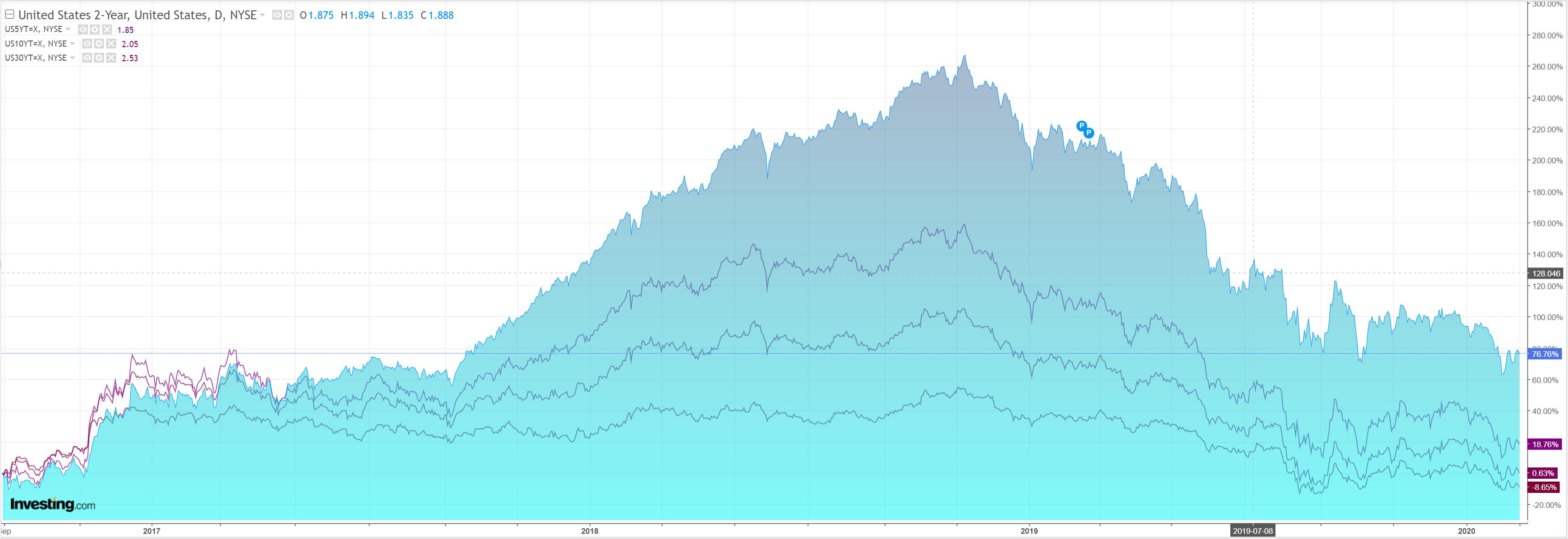

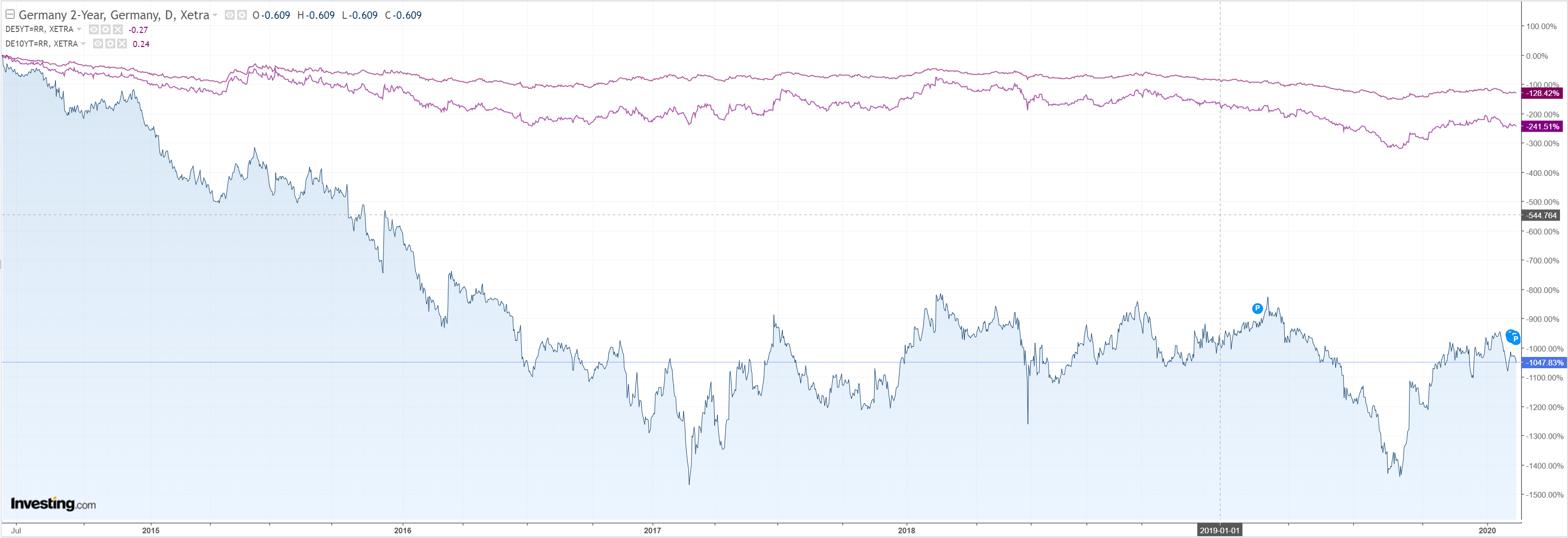

Bonds were bid:

Stocks flopped into green:

Westpac has the wrap:

Event Wrap

US retail sales rose 0.3% in Jan, as expected, although the prior month was revised 0.1ppt lower. The core control group was unchanged (vs +0.3% expected) and also revised lower in Dec. Industrial production fell 0.3% in Jan (vs -0.2% expected). Consumer confidence (Univ. Mich.) rose from 99.8 to 100.9 and beat expectations, while the 5-10yr inflation expectations component slipped from 2.5% to 2.3%. The mix of data suggests downside risks to GDP forecasts for Q4 and Q1.

Event Outlook

In NZ, REINZ housing data is due this week for January. The supply of homes is tight, while low interest rates are supporting demand, resulting in robust price growth. BusinessNZ services PSI for January, and December net migration are also due.

Japanese GDP is expected to contract sharply in Q4 as a result of weak consumption. Q1 will then be impacted by the coronavirus outbreak.

In the US, markets are closed for Presidents Day.

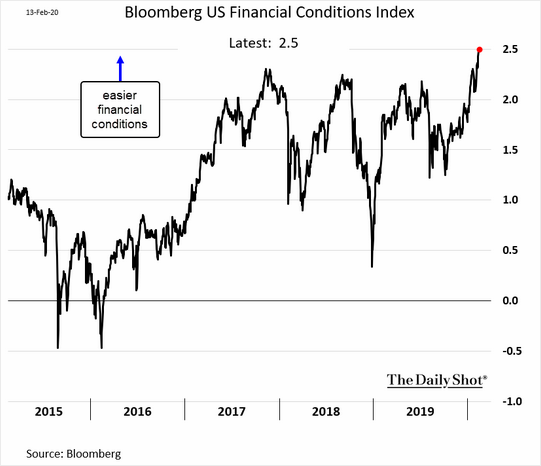

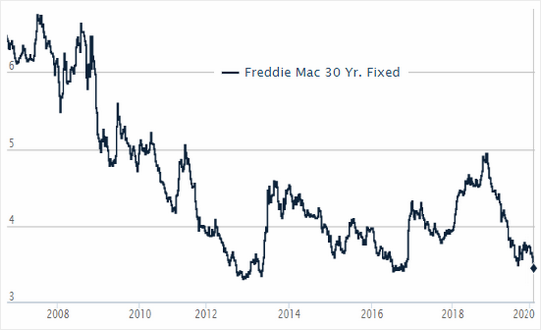

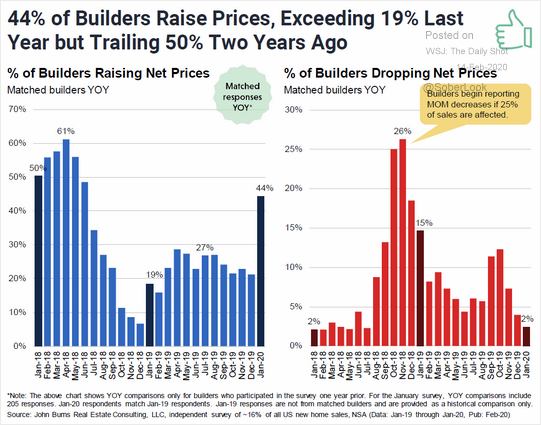

The basci set up is unchanged. The US is powering on easy money for housing:

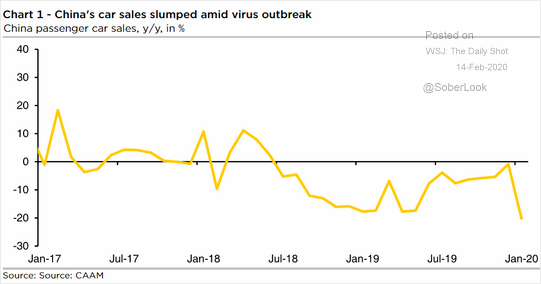

Whie Europe is barely out of recession and is about to feel the full force of the COVID-19 demand shock:

With German industry driving off a cliff.

While that happens, the Australian dollar can only go lower as DXY roars.