Friday night saw DXY pull back sharply as EUR rallied:

The Australian dollar bounced but then gapped lower this morning to be near new lows again:

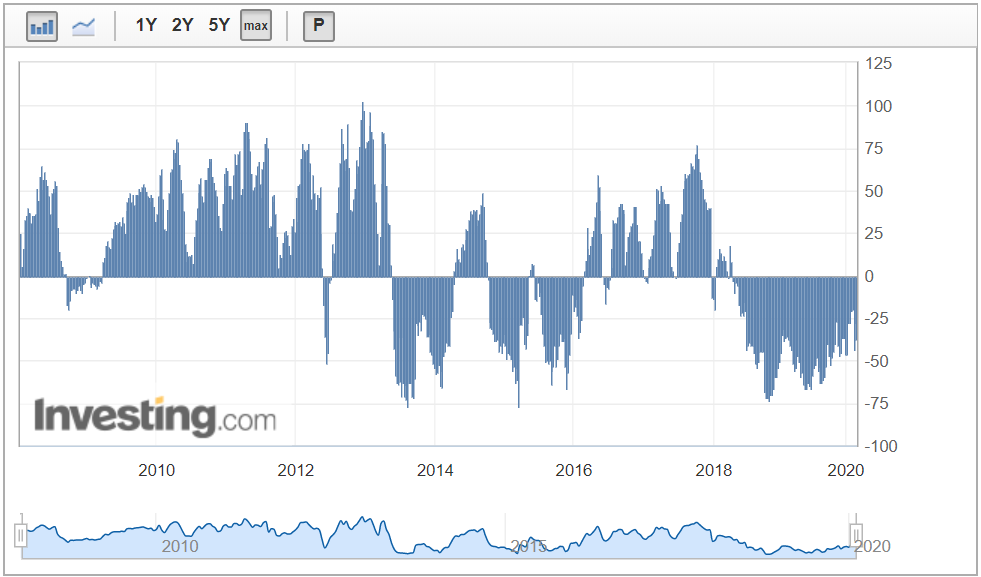

Gloriously, AUD shorts fell, leaving plenty more downside:

EM forex is worse still:

A golden rocket takes flight:

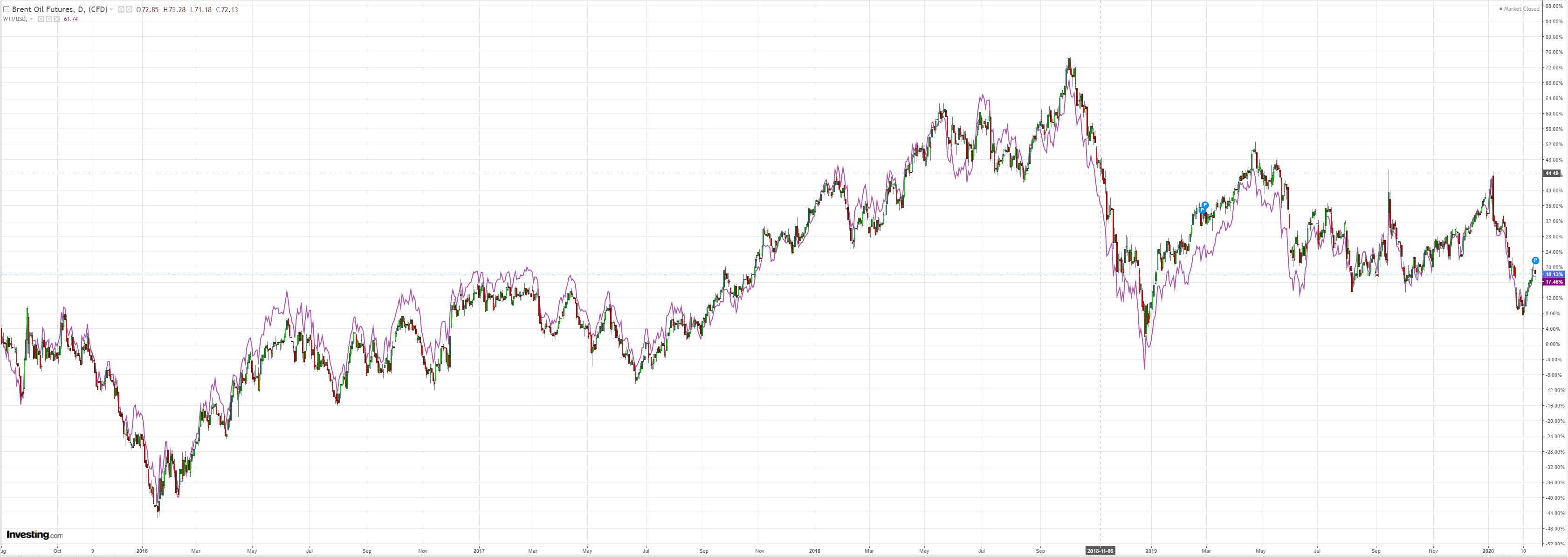

Oil fell but not enough:

Base metals were weak:

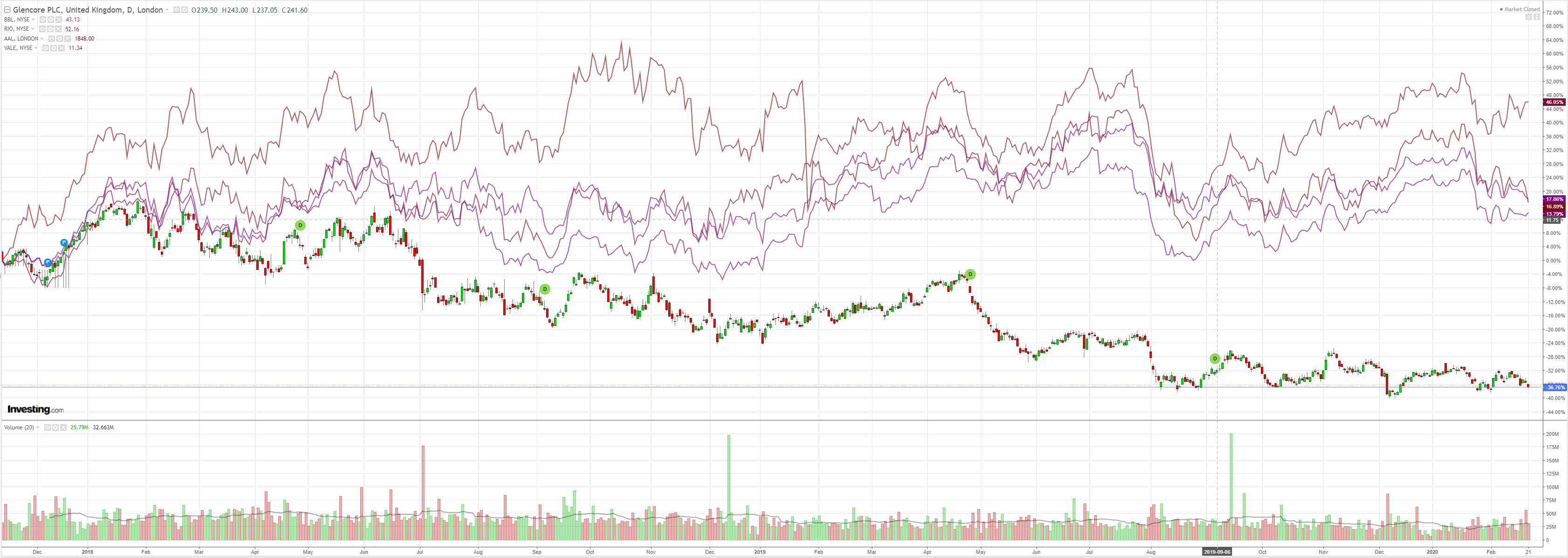

Big miners were thumped. The iron ore rally is not believed:

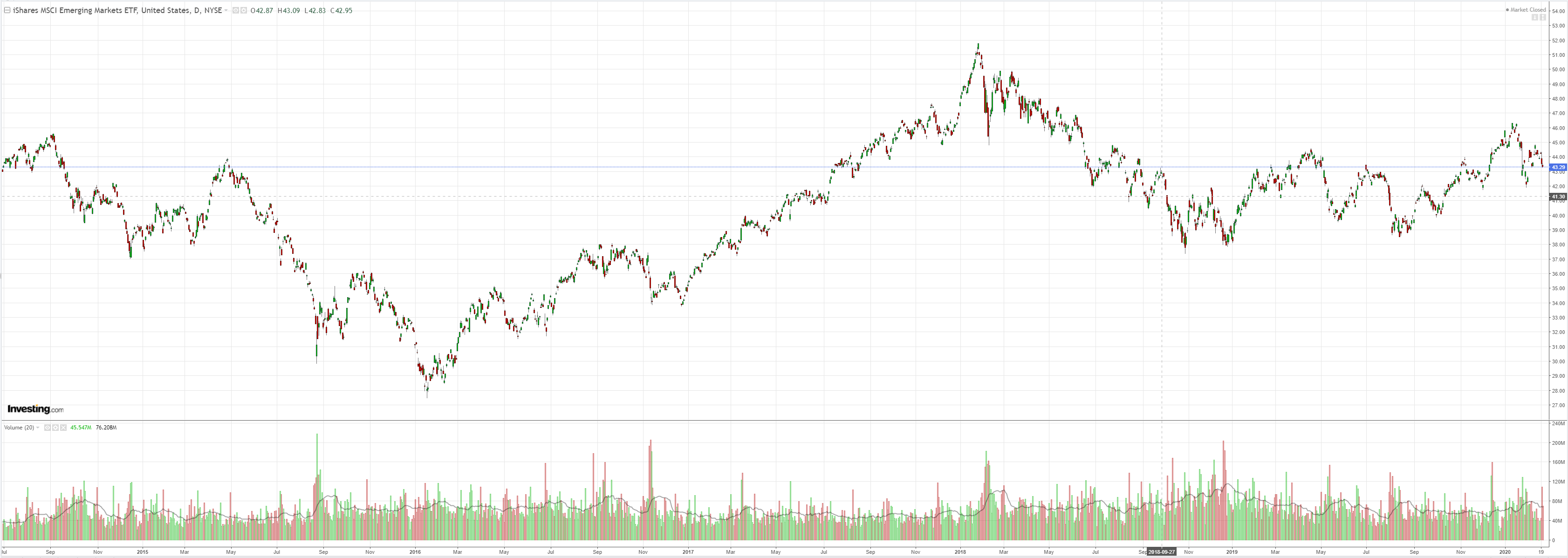

EM stocks fell:

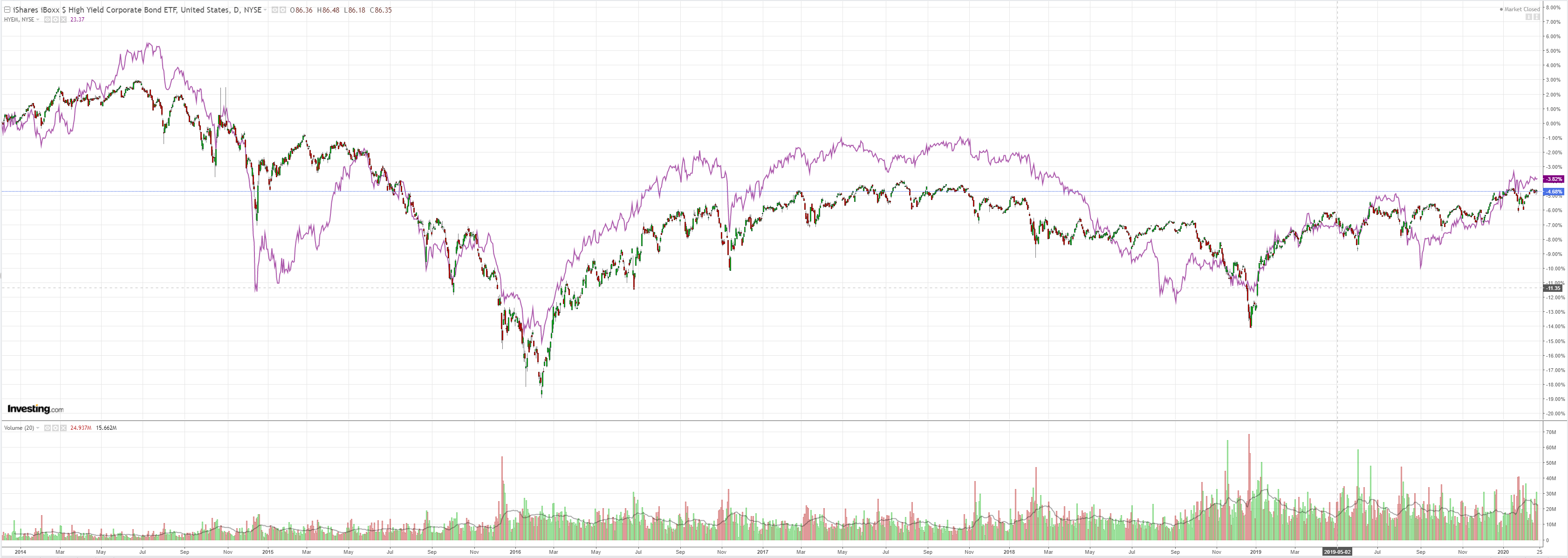

But the dash for trash continues. This will be a bloody mess when it wakes:

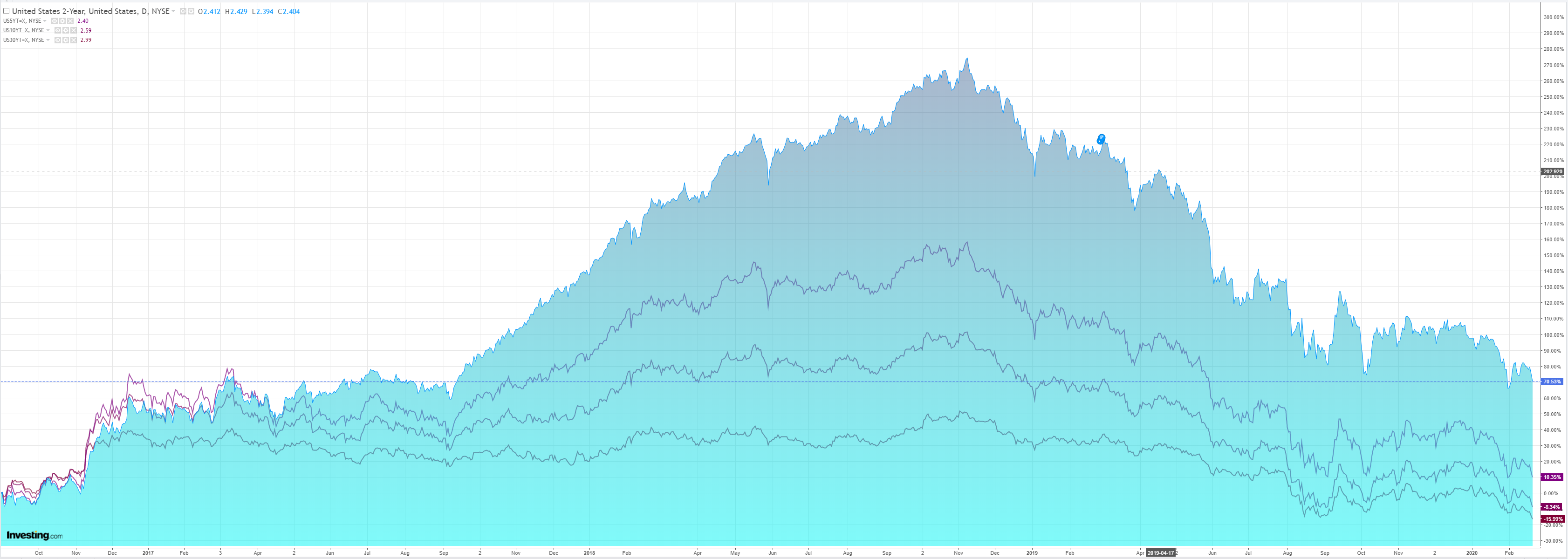

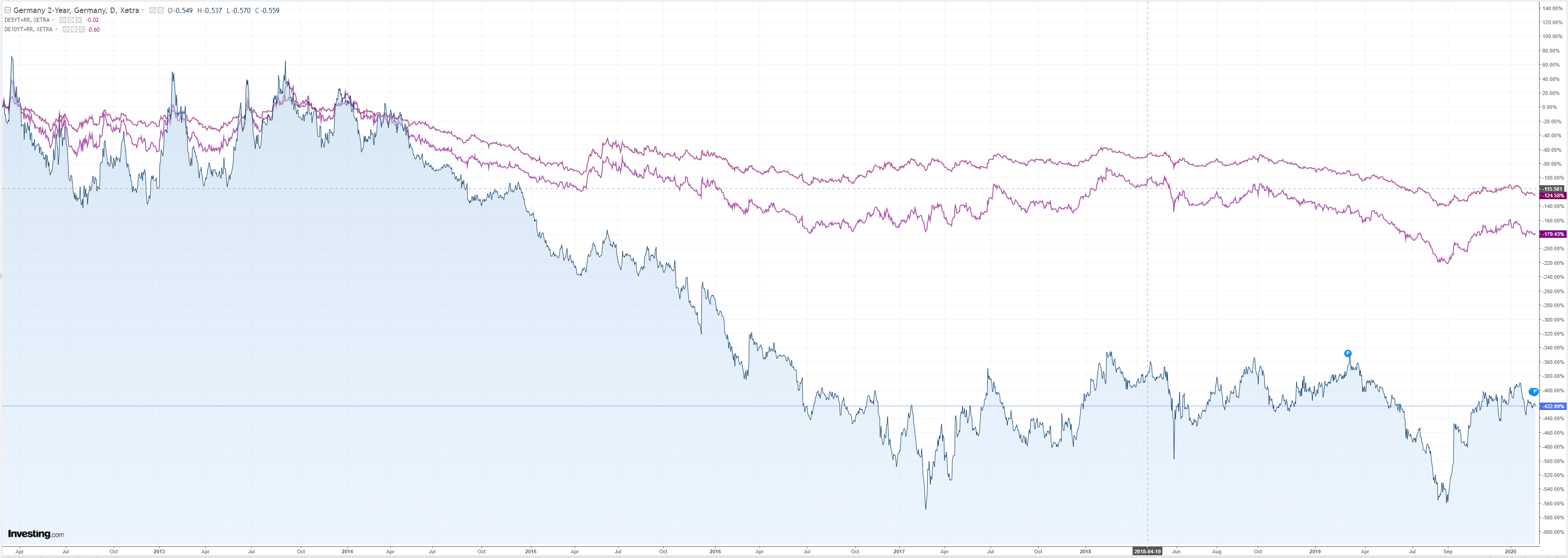

Bonds were bid, bid, bid:

Stocks were hit hard:

Westpac has the wrap:

Event Wrap

US manufacturing PMI fell more than expected, from 51.9 to 50.8 (vs 51.5 expected), taking the index to a low since August. The services index also fell, taking the composite level to the lowest since 2013. These readings indicate a negative economic impact from the coronavirus pandemic.

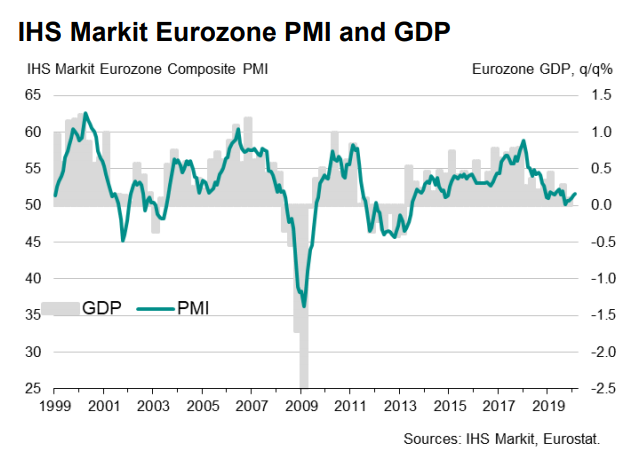

In contrast, Eurozone PMIs unexpectedly rose, the manufacturing index up from 47.9 to 49.1 (vs 47.4 expected). UK PMIs also rose, with the pandemic mentioned in survey comments but not reflected in the headline numbers.

Fed Governor Brainard said policy may need to remain accommodative to reach the 2% inflation target, and even supported an inflation overshoot to achieve average inflation of 2%. Bullard and Bostic said they are watching for pandemic effects but hadn’t changed their outlooks yet, noting the US economy is strong.

Event Outlook

In New Zealand, monthly spending gauges indicate that Q4 real retail sales will remain strong, with an expected increase of 0.8% (Westpac at 1.4%). This has been spurred by the housing market appreciation, increases in government spending, household income growth and the Black Friday sales.

In Germany, the February IFO business climate survey will be released, and followed in the US by the January Chicago Fed activity index as well as the February Dallas Fed index. The Federal Reserve’s Mester will speak on the economy.

T’was the virus that did the equity damage but it was data that dented forex. The DXY over EUR bid was upset by a better Eurozone PMI:

Versus worse USPMI:

I don’t expect it to last. The more important ISM should rebound based upon partials:

While the supply chain shock is approaching Europe by land and sea, not to mention the Italian outbreak.

DXY and gold remain the safe havens. New lows likely ahead for AUD.