Australian dollar holds again as virus panic barely clears throat

DXY fell again last night as EUR lifted:

The Australian dollar fell heavily against all but the USD:

EM forex was even worse:

Gold was hit by profit taking:

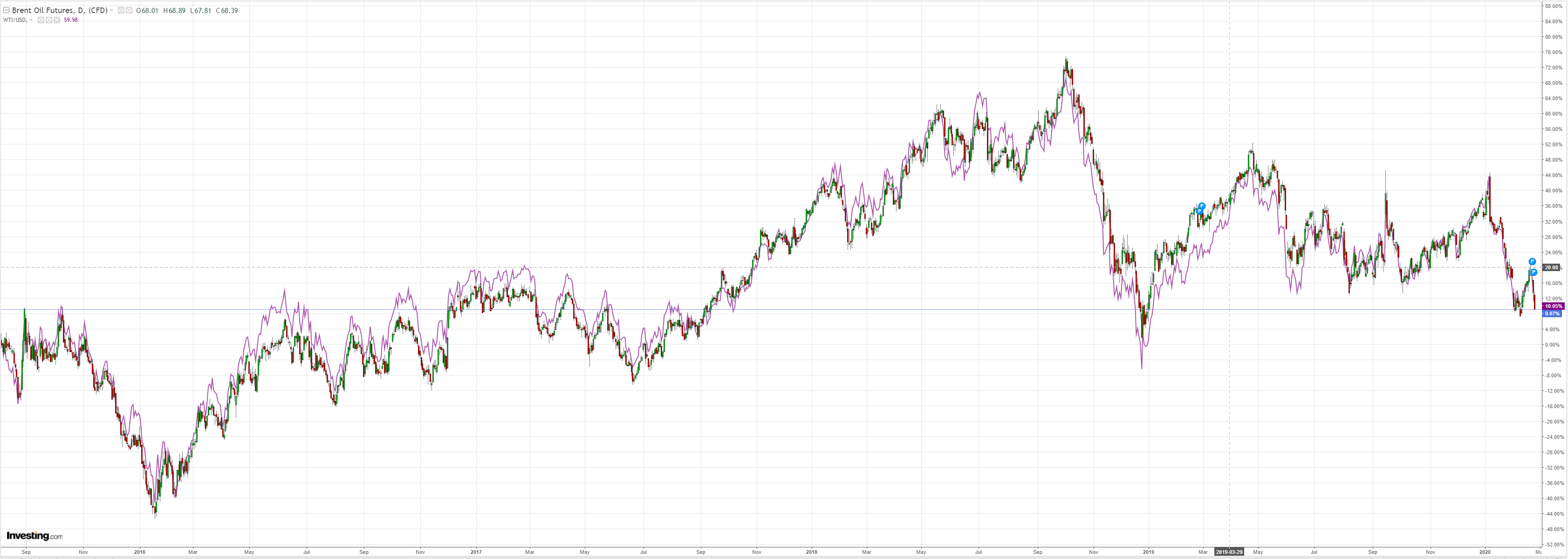

Oil was squashed. It has much more downside:

Metals the same:

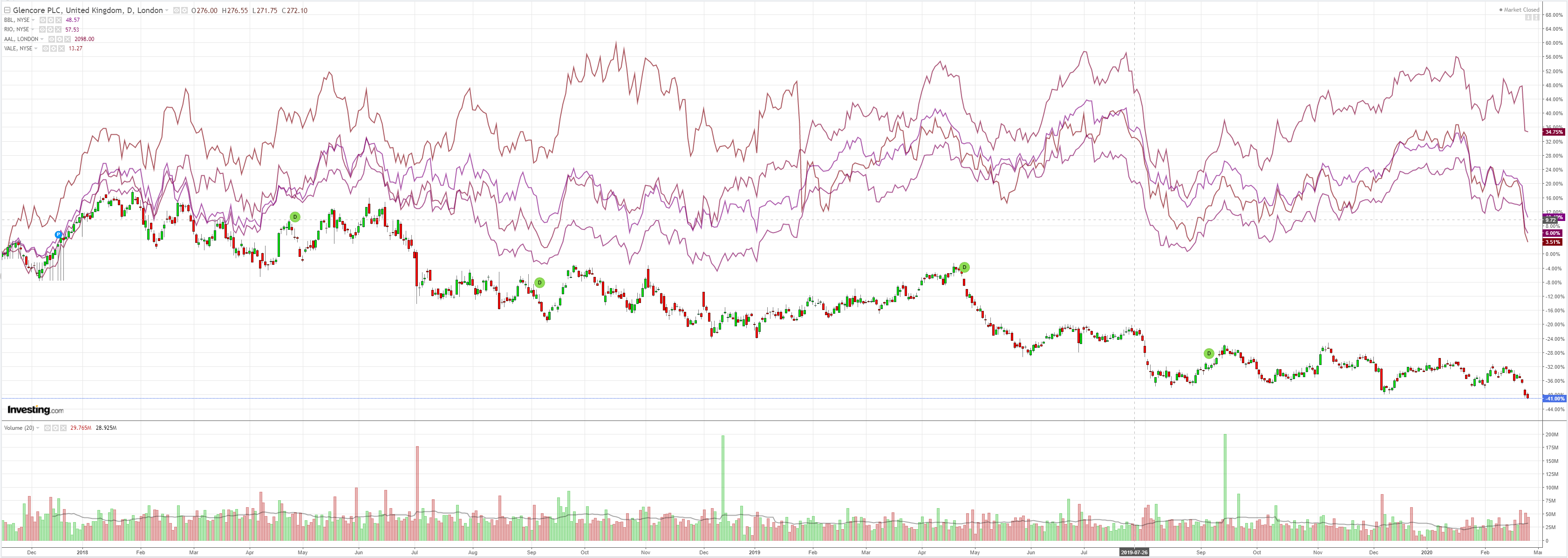

Miners are not buying the iron ore bid:

EM stocks tried and failed:

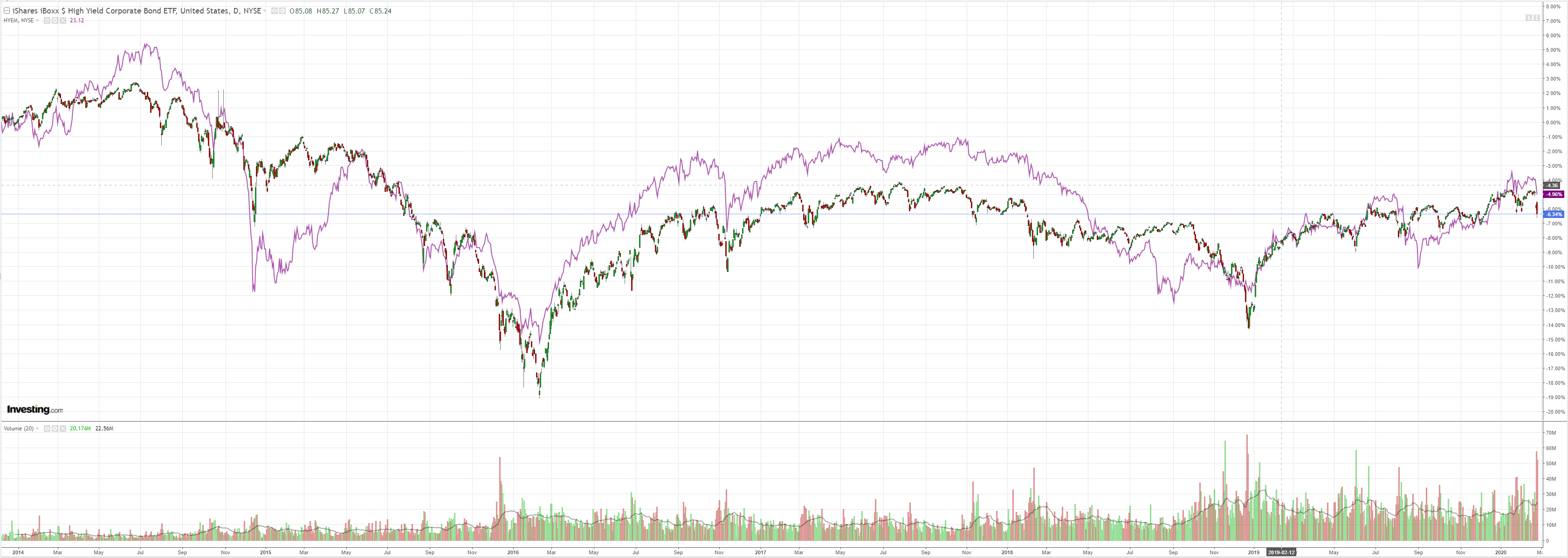

Junk finally took a hit. But it’s barely started. Check out the 2016 lows. Oil is the key:

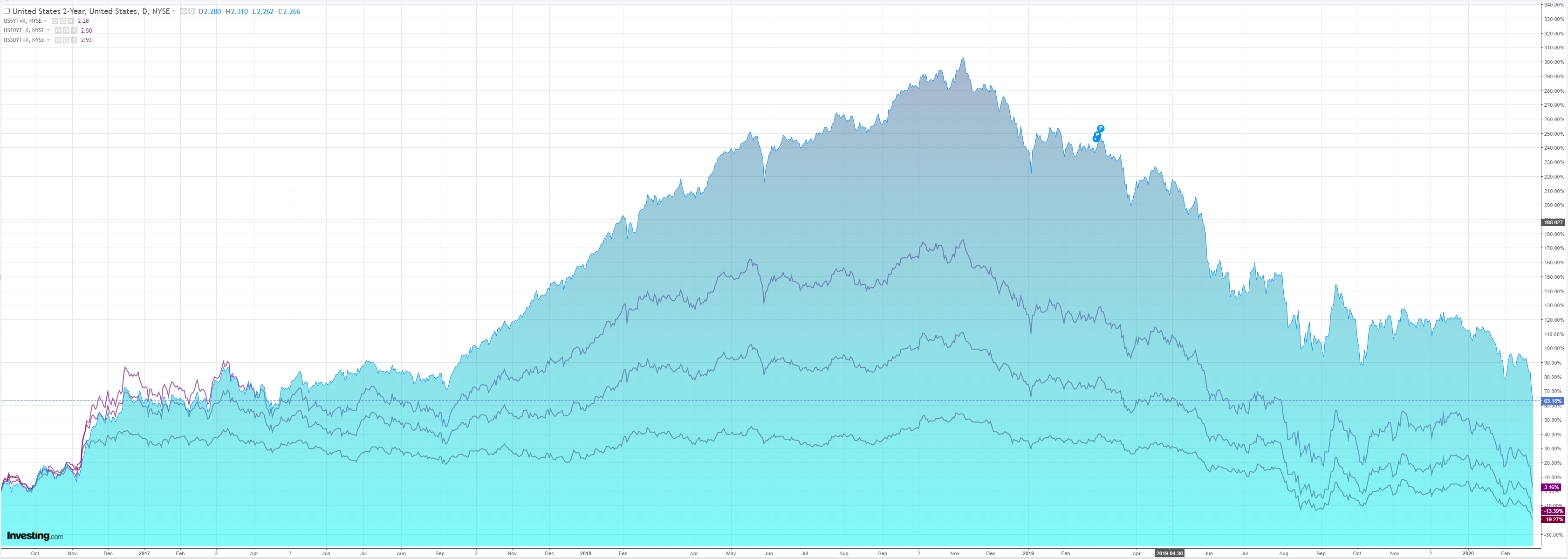

All bonds were bid:

Stocks were smashed again:

Westpac has the data wrap:

Event Wrap

Once again, the continuing spread of the COVID-19 coronavirus dominated market sentiment. The Italian department of infectious diseases (ISS) announced during the European afternoon that cases of the virus had risen to 322 with 10 deaths, adding that the infections had mainly affected the elderly. New outbreaks occurred in Austria, Switzerland and mainland Spain.

US Dec. S&P CoreLogic CS house prices were in line with expectations, with 20-City prices +2.9%y/y and a national gain of+3.8%y/y. The Richmond Fed’s activity survey disappointed at -2 (vs estimate of 10 and the prior reading of 20), but the detail of this recently volatile report showed 3-month averages of the key components remaining solid. Conference Board consumer confidence disappointed at 130.7 (vs estimate of 132.2, and prior revised from 131.6 to 130.4).

Federal Reserve Vice Chair Clarida disputed suggestions that the central bank suffers from a “hall of mirrors” problem under which it slavishly follows financial-market expectations for monetary policy. He said they place at least as much weight on surveys of Fed watchers as price signals from the market in trying to determine expectations for policy.

Germany’s final 4Q GDP was unchanged from its initial prior release at 0.0% s.a. and +0.4% work day adjusted.

Event Outlook

In Australia, Q4 construction work is expected to edge lower by -0.6% (market -1.0%). Having fallen 10% over the past 5 quarters, the pace of decline appears to be moderating – however, a downside risk for Q4 is disruption from bushfire smoke.

In Hong Kong, the market anticipates that Q4 GDP will fall 2.9%yr, reflecting broad-based weakness across their economy. Singapore’s industrial production is expected to show further weakness in January, declining by 0.7%.

US January new home sales are meanwhile expected to increase by 717k as the upswing in residential construction continues.

The market has barely cleared its throat in this virus panic. The selling is orderly. Credit has hardly budged. All we’ve done is blow a little froth off the top of equities. They’re still trading at 18x forward.

If markets have to discount a global recession, complete with credit events, then this is absolutely nothing so far, which is why the Australian dollar has been OK.

I’d guess the same applies to the USD/EUR relationship. DXY can fall when all we’re doing to unwinding some stock euphoria. But as Europe’s broken borders succumb to COVID-19 faster than the US does it will be a different story.

We ain’t seen nuthin’ yet…