DXY softened last night after its bull run:

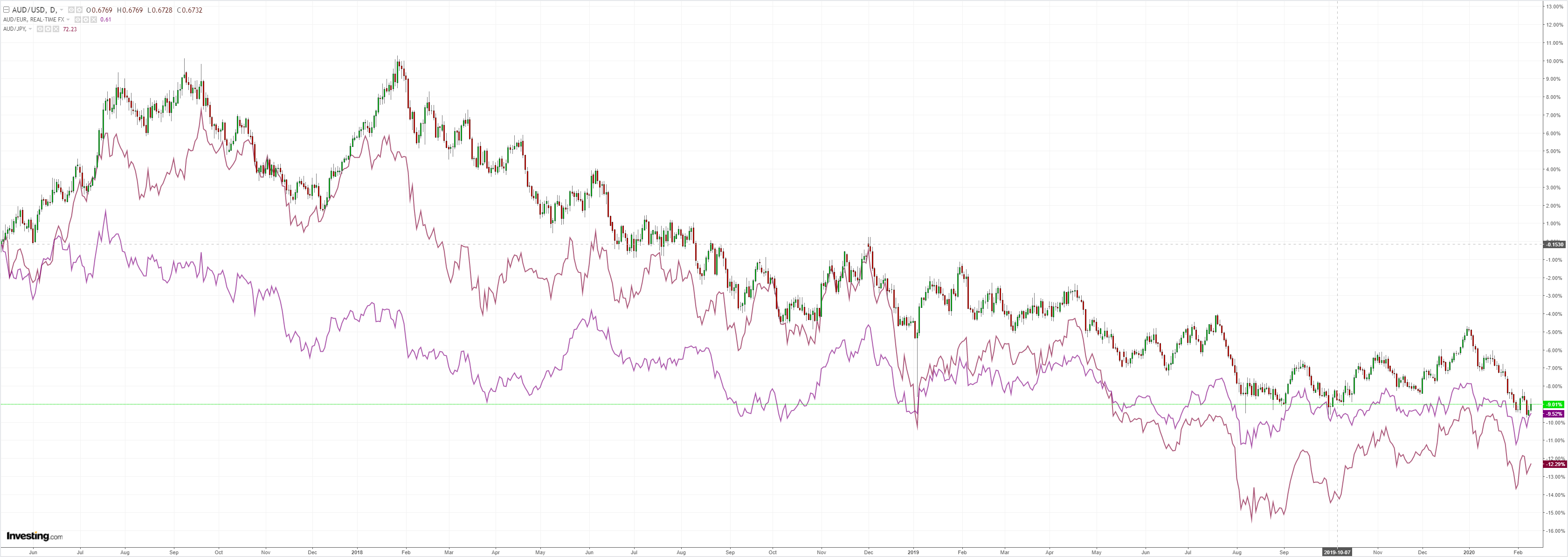

The Australian dollar lifted on virus hopes:

Gold is still hanging in there:

Oil was clubbed again:

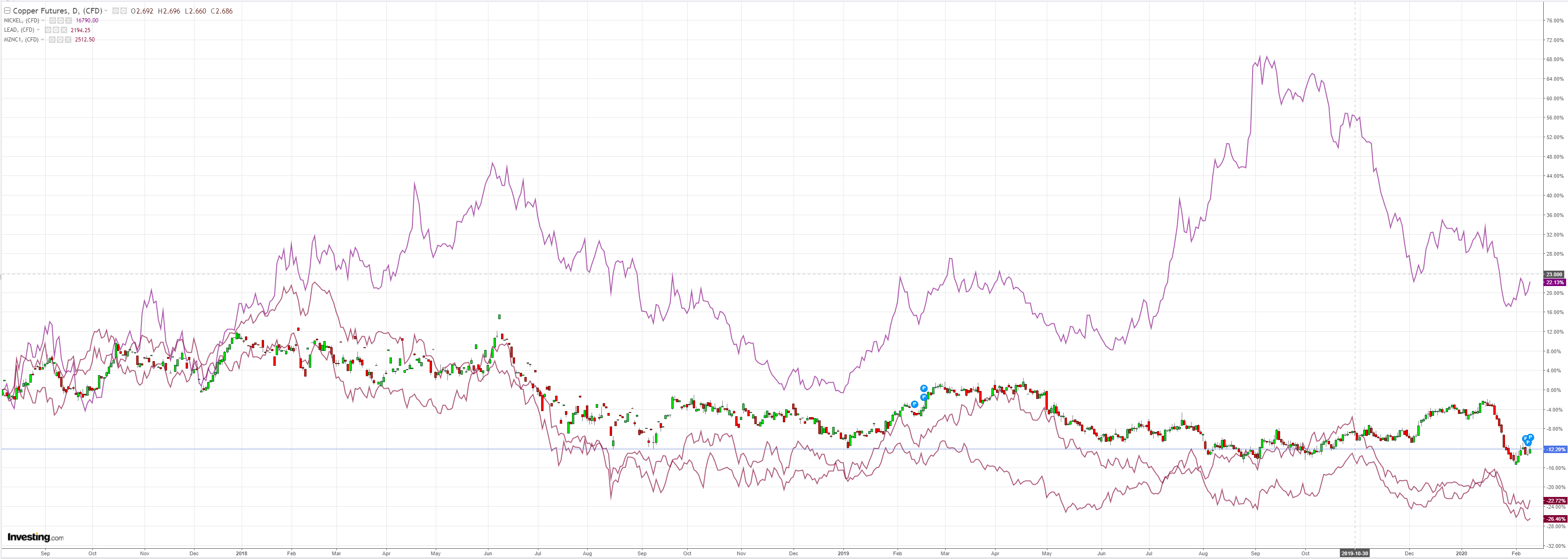

But metals are trying:

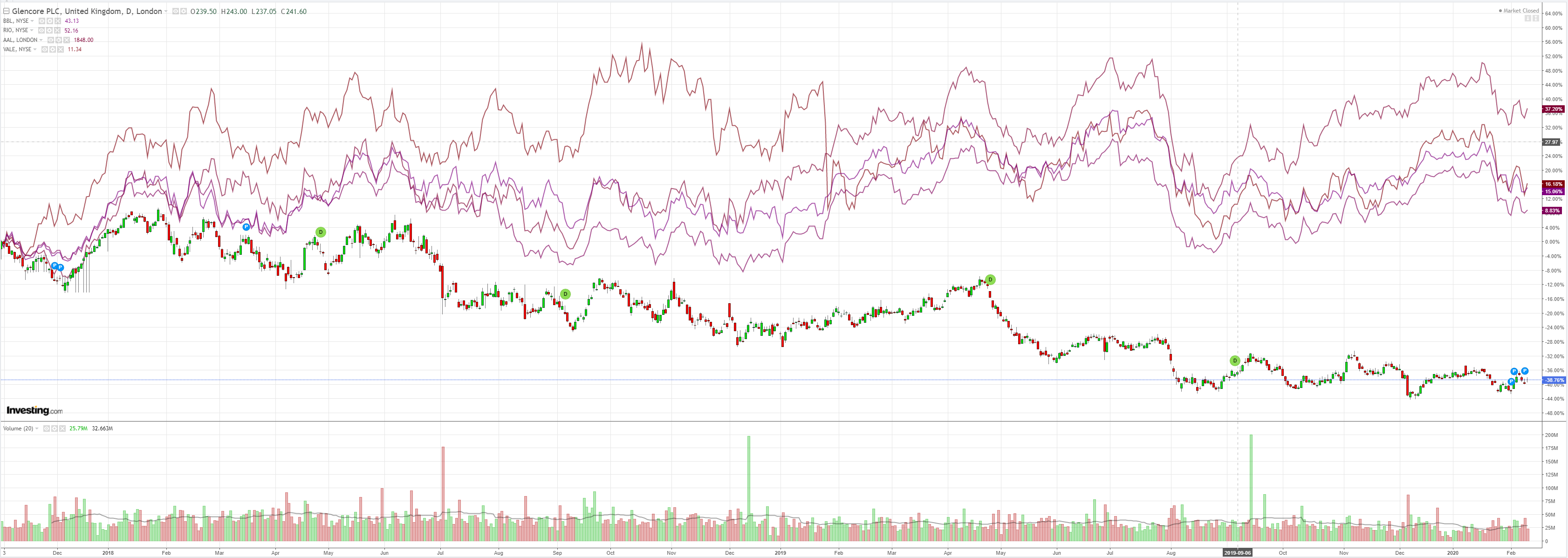

Miners rebounded:

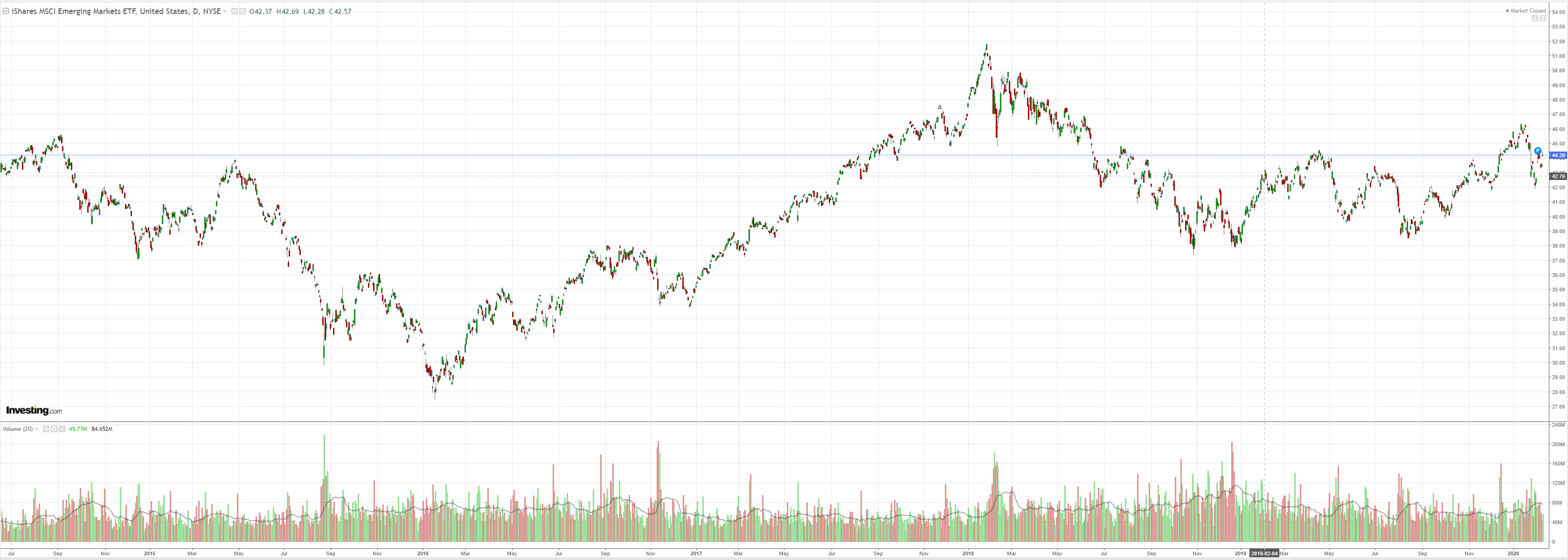

And EM stocks:

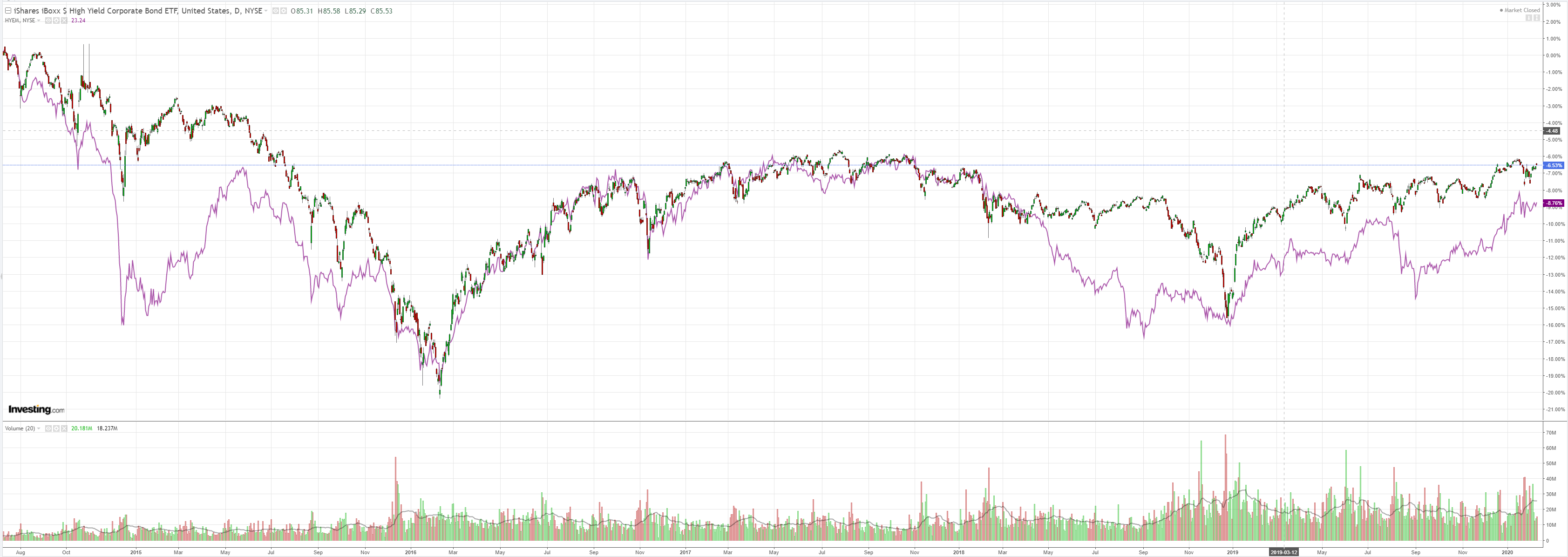

Junk hasn’t a care in the world:

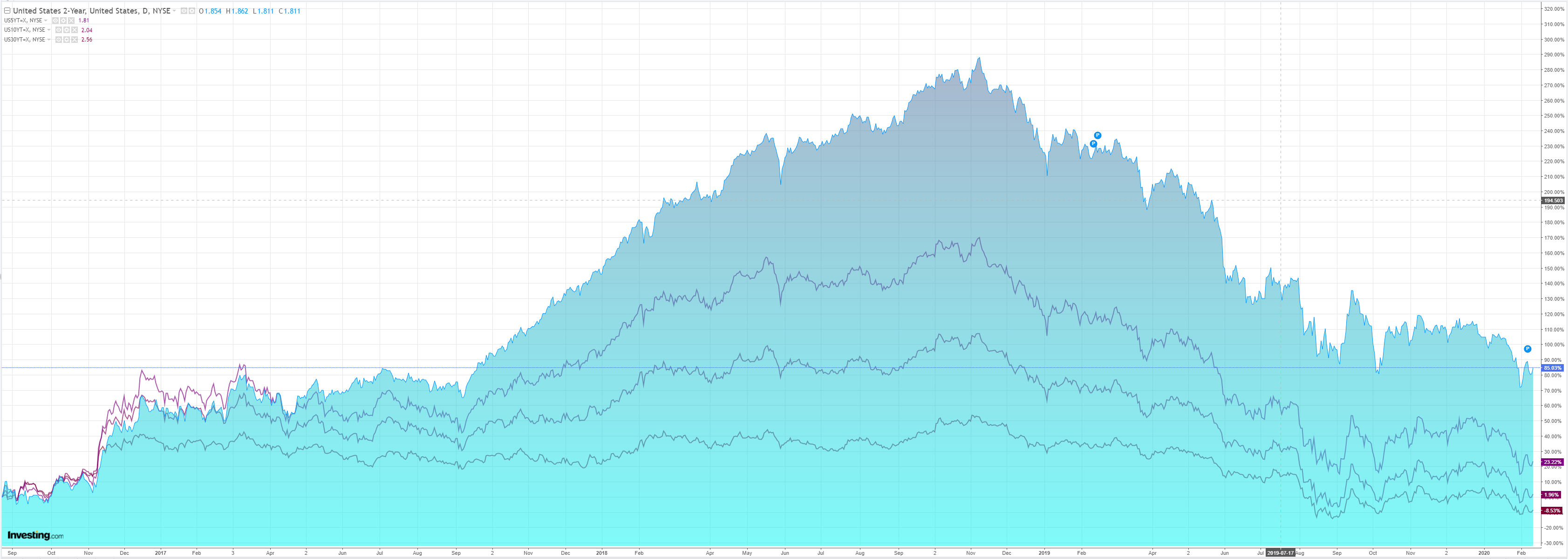

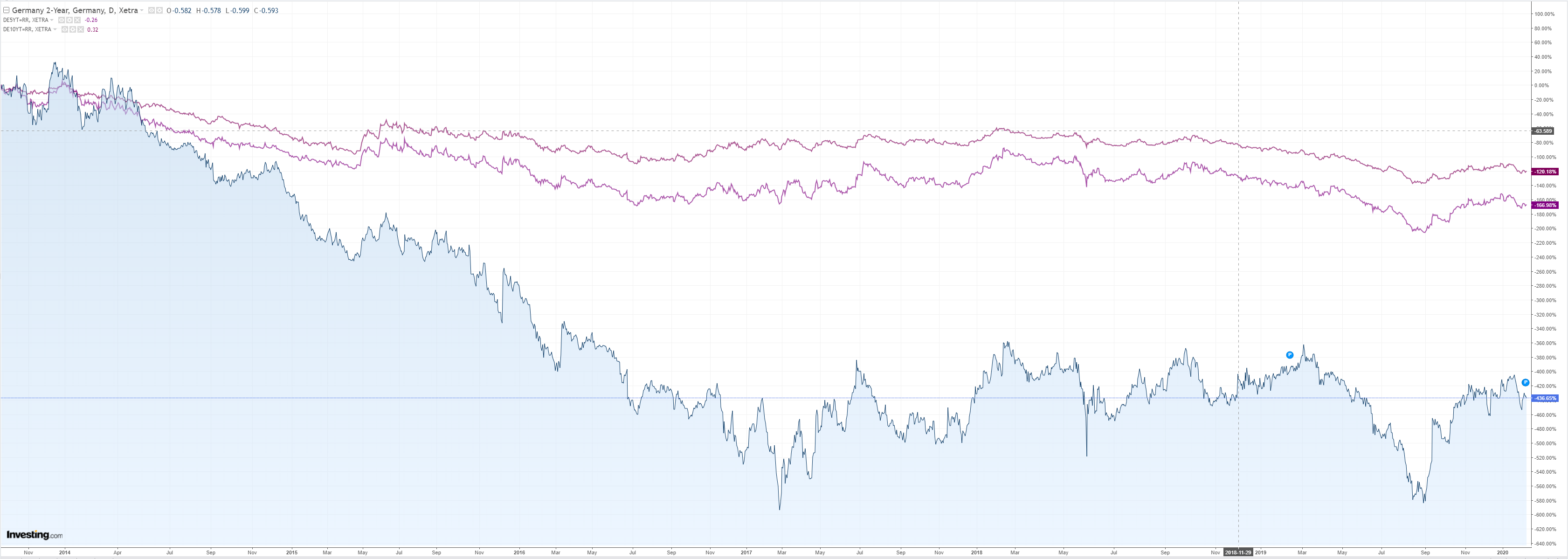

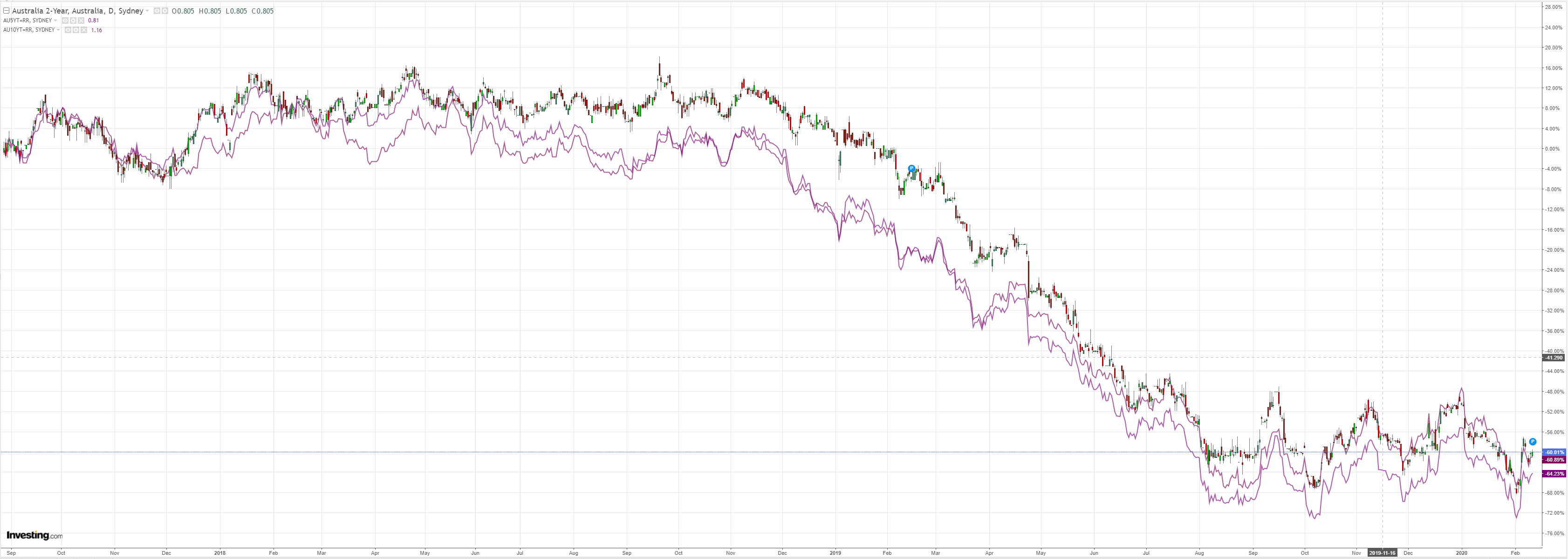

Bonsd were all hosed off:

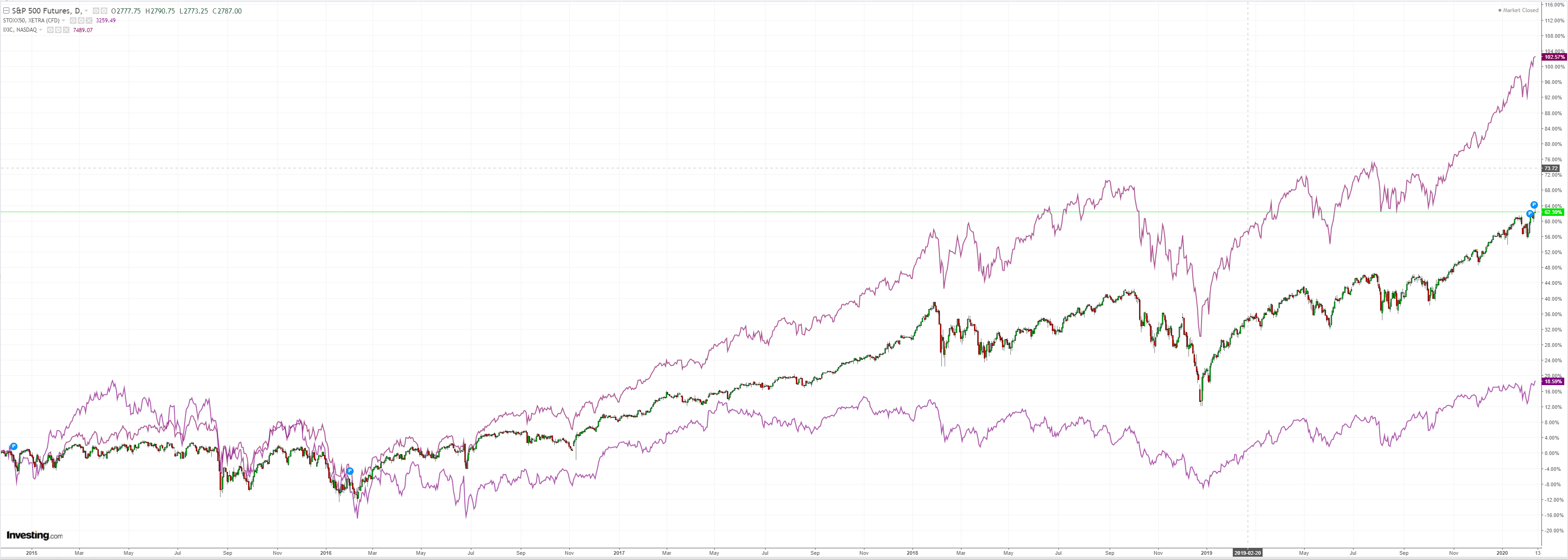

As stocks managed weak gains:

Westpac has the wrap:

Event Wrap

US NFIB small business survey beat expectations (104.3 vs est. 103.5, prior 102.7), though remains within its recent high range. Survey respondents continue to cite an expanding economy with positive expectations, and their main concern being the shortage of skilled labour.

FOMC Chair Powell delivered his initial Congressional testimony, repeating the positive outlook for the economy in the Monetary Policy Report and that policy was appropriate. He also repeated that there are downside risks are from an extended coronavirus outbreak and that this would continue to be monitored.

The UK avoided a 4Q GDP contraction. Although it was flat q/q (as expected), revisions to earlier quarters meant that the 1.1% y/y level beat expectations (est. +0.8%y/y). Govt. activity and solid exports offset weak capital formation and stalled private consumption. Dec. industrial (+0.1%m/m, est. +0.3%m/m) and manufacturing (+0.3%, est. +0.5%) production were weak in annual terms but a lift in construction (+0.4%m/m, est. -0.4%m/m) and a better Dec. trade balance (+GBP6.7bn, est. -GBP2bn) offset the negatives.

Event Outlook

The RBNZ’s Monetary Policy Statement today is expected to see the OCR unchanged, with its easing bias becoming a conditional one (dependent on the severity of the coronavirus pandemic). Virus uncertainty aside, the domestic economy has been stronger than expected since the previous MPS. In NZ there’s also Jan electronic retail spending data to watch.

In Australia, the Westpac consumer confidence survey for Feb is due. The sentiment reading has been trending lower since mid-2018.

Eurozone industrial production in Dec is expected to have fallen 2.0%.

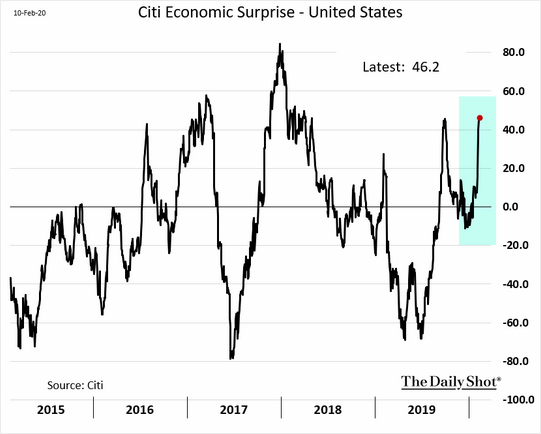

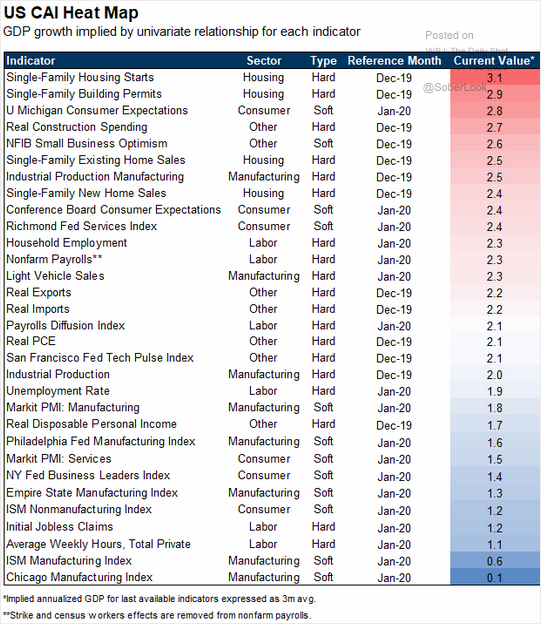

The big picture story remains simple. The US is powering on:

Led by housing:

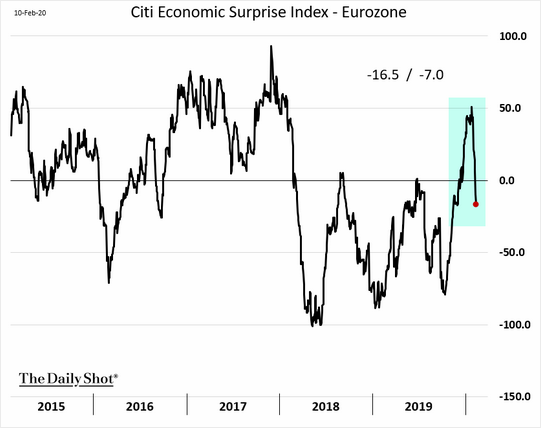

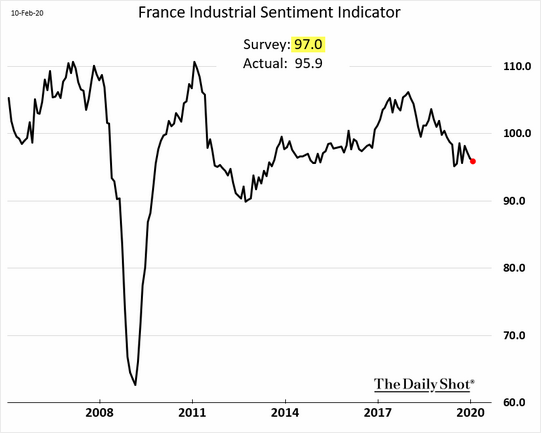

While Europe wilts:

Led by industry:

And both trends are made worse by nCoV. Keeping the trend alive:

While EUR is weak, DXY is strong. Both of those equal a weak AUD.