Late last year, The Australian’sAdam Creighton labelled the Aged Pension “an economically costly inheritance preservation scheme” given its largesse towards wealthy home owning retirees.

This claim came about after it was revealed by Creighton that elderly Australians living in $1m-plus homes are claiming $6.3 billion in pension payments:

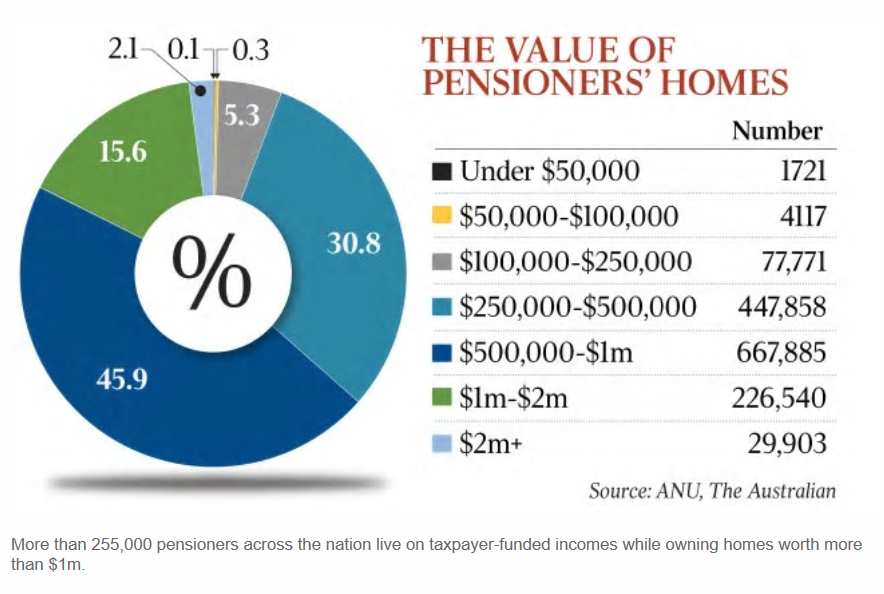

Retirees living in $1m-plus homes are receiving more than $6.3bn a year in age pension payments, enough to fund income tax cuts that would supercharge economic growth.

More than 255,000 pensioners across the nation, mainly in elite pockets of Sydney and Melbourne, live on taxpayer-funded incomes while owning homes worth more than $1m — a more than twentyfold increase in a decade — according to analysis of social security data by ANU.

Almost 30,000 age pensioners lived in homes worth more than $2m this financial year — two-thirds of them in Sydney and a fifth in Melbourne — receiving $680m in pension payments annually, according to the analysis…

Ben Phillips, an associate professor at ANU, said such pension payments meant workers were paying higher rates of tax to protect sizeable inheritances…

Now, The AFR reports that baby boomers in Sydney and Melbourne are living in giant property nest eggs worth millions of dollars, which dwarfs their modest superannuation savings. And this has prompted calls for them to use reverse mortgages to fund their retirements:

Advertisement

Boomers in Melbourne and Sydney are potentially sitting on giant nest eggs because the homes they bought 40 years ago have compounded in value to be among the world’s most expensive residential property…

An estimated 4.5 million retirees have equity in their homes that is on average about four to five times their super savings, which for male Baby Boomers is about $150,000 and for females about $80,000…

“There is a huge unmet need for retirement funding,” said Josh Funder, Household Capital’s chief executive and founder, Rhodes scholar, venture capitalist and former business consultant, including for Boston Consulting Group…

“Most Australians can double their available funding at retirement through reverse mortgages”…

Nick Sherry, a former superannuation minister and chairman of Household Capital, said releasing home equity needs to be encouraged to top up modest retirement savings…

Reverse mortgages allow retirees to draw 15 per cent of household equity at 60 and increase withdrawals by 1 per cent a year for the next 20, or a cap of 35 per cent.

There’s no doubt that Australia’s retirement system is not functioning effectively, given younger Australians are facing the prospect of never owning a home (or being enslaved in mortgage debt), whilst also having to pay ever-rising taxes to subsidise retirees that are far better-off financially than they will ever be.

The obvious solution is to:

Advertisement

Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2022), thus allowing current retirees and prospective retirees adequate time to make arrangements; and

Significantly raise the overall pension asset test threshold as well as the base rate.

Under this solution, house-rich pensioners choosing to remain in place could continue to receive an income stream as they do now under the Aged Pension via the Pension Loans Scheme (the federal government’s official reverse mortgage scheme), but with less drain on the Budget and on younger taxpayers. But they would similarly be incentivised to move as the family home would no longer be a tax free shelter.

Poorer retirees that do not own a dwelling would also be made better-off via the increase in the overall assets test (thus allowing greater financial assets to be held without cutting-off access to the pension), as well as the increase in the base rate.

It’s a solution that would greatly improve equity and ensure that Australia’s welfare system is better targeted towards those in genuine need.

Advertisement

It would also ensure that the pension system evolves alongside the structural reduction in home ownership rates, by making the system more neutral towards property ownership and financial assets.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.