Wholesale electricity price futures are sharply lower

Our updated wholesale electricity price forecast expects prices will average $74/MWh across the National Electricity Market (NEM) in CY20, declining to $70/MWh in CY21—reflecting a material revision down from our prior forecast. Baseload futures through CY20-21 are sharply lower than 3 months ago and our mark-to-market updates recognise realised prices in the Dec-19 half were >20% lower in some NEM regions. We still expect >4GW of new renewable capacity to come online over CY20-21 to apply downward pressure on average prices and earnings headwinds for baseload generation. However, our thesis hasn’t changed—grid constraints and slow connection processes will continue to stifle the full impact of renewables led price relief.

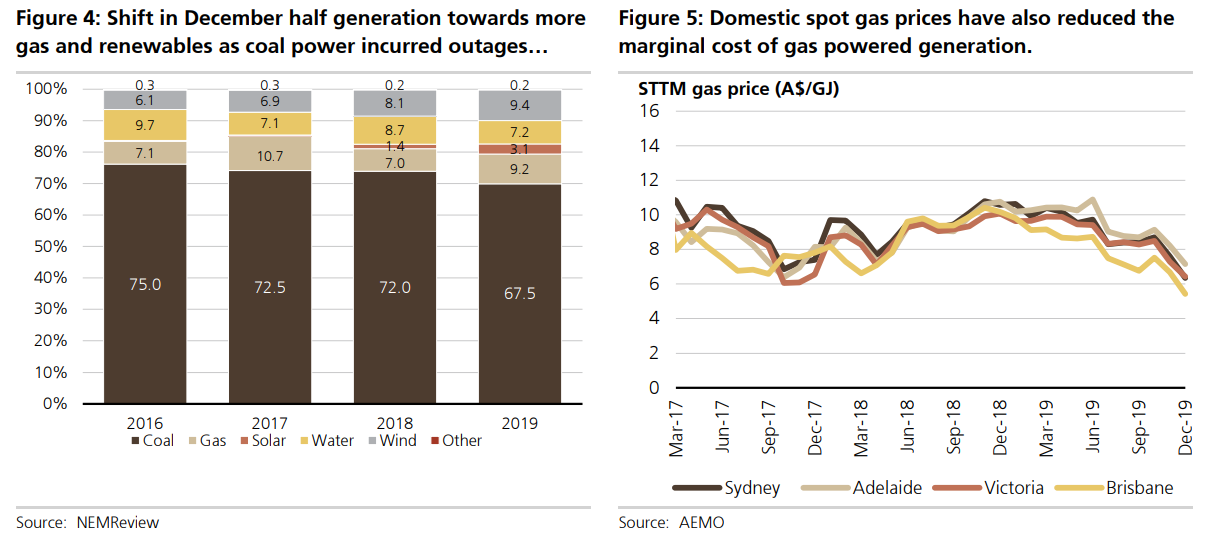

Soft Asian spot LNG prices drag Australian domestic gas prices lower

The key change to our wholesale electricity price forecast arises from lower domestic gas prices (Dec-19 hub prices ~$2/GJ lower y/y). With gas the price setting marginal supplier of electricity to the NEM, changes in domestic gas prices have a material impact on wholesale electricity prices. Australian domestic gas prices are influenced directly by Asian spot LNG (JKM) prices (via an LNG netback equivalent price). Average JKM spot prices for the Dec-19 quarter were down 37% y/y and we expect soft JKM spot prices to prevail over the next two years due to excess global LNG supply and moderating gas demand growth in China as coal-to-gas furnace switching slows.

Only if the Australian Domestic Gas Security Mechansim (ADGSM) forces spot prices lower and then psuhes them into the gas contract market which it has so far failed to do.

The Morrison Government must MAKE IT HAPPEN via the ADGSM review.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.