EIA forecasts Brent crude oil spot prices will average $65 per barrel (b) in 2020 and $68/b in 2021, compared with an average of $64/b in 2019. EIA expects West Texas Intermediate (WTI) crude oil prices will average about $5.50/b lower than Brent prices through 2020 and 2021, compared with an average WTI discount of about $7.35/b in 2019.

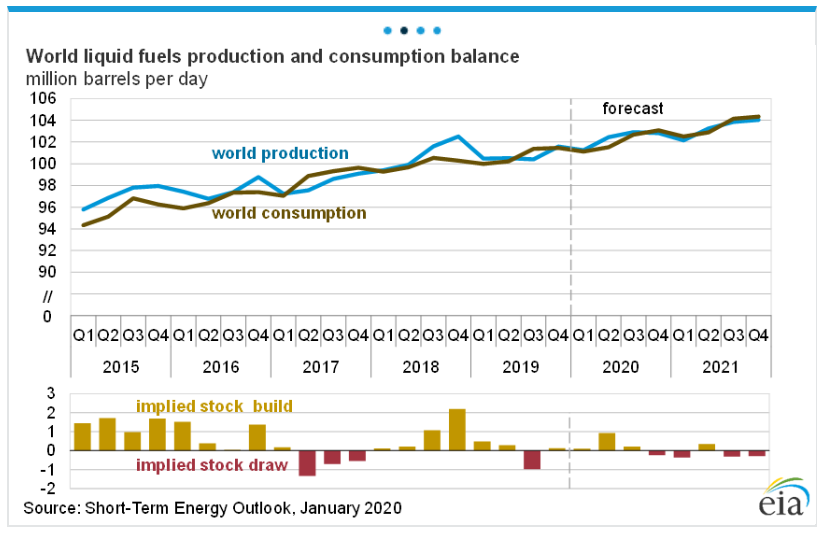

Global liquid fuels inventories were mostly unchanged in 2019, and EIA expects they will grow by 0.3 million b/d in 2020 and then decline by 0.2 million b/d in 2021.

On January 1, 2020, the International Maritime Organization (IMO) enacted Annex VI of the International Convention for the Prevention of Pollution from Ships (MARPOL Convention), which lowers the maximum sulfur content of marine fuel oil used in ocean-going vessels from 3.5% of weight to 0.5%. EIA expects this regulation will encourage global refiners to increase refinery runs and maximize upgrading of high-sulfur heavy fuel oil into low-sulfur distillate fuel to create compliant bunker fuels. EIA forecasts that U.S. refinery runs will rise by 3% from 2019 to a record level of 17.5 million b/d in 2020, resulting in refinery utilization rates that average 93% in 2020. EIA expects one of the most significant effects of the regulation will be on diesel wholesale margins, which will rise from an average of 43 cents per gallon (gal) in 2019 to a forecast peak of 53 cents/gal in March 2020 and an annual average of 50 cents/gal in 2020. EIA expects diesel margins to decline to 49 cents/gal in 2021.

U.S. regular gasoline retail prices averaged $2.60/gal in 2019, and EIA forecasts that they will average $2.63/gal in both 2020 and 2021.

EIA estimates that U.S. crude oil production averaged 12.2 million b/d in 2019, up 1.3 million b/d from 2018. EIA forecasts U.S. crude oil production will average 13.3 million b/d in 2020 and 13.7 million b/d in 2021. Most of the production growth in the forecast occurs in the Permian region of Texas and New Mexico.

U.S. net imports of crude oil and petroleum product fell from an average of 2.3 million b/d in 2018 to an average of 0.5 million b/d in 2019, and EIA estimates the United States has exported more total crude oil and petroleum products than it has imported since September. EIA forecasts that the United States will be a net exporter of total crude oil and petroleum products by 0.8 million b/d in 2020 and by 1.4 million b/d in 2021.

U.S. dry natural gas production set a new record in 2019, averaging 92.0 billion cubic feet per day (Bcf/d). EIA forecasts dry natural gas production will rise to 94.7 Bcf/d in 2020 and then decline to 94.1 Bcf/d in 2021. Production in the Appalachian region drives the forecast as it shifts from growth in 2020 to declining production in 2021.

EIA forecasts that Henry Hub natural gas spot prices will average $2.33 per million British thermal units (MMBtu) in 2020, down from $2.57/MMBtu in 2019. EIA expects that natural gas prices will then increase in 2021, reaching an annual average of $2.54/MMBtu.

Balance more or less achived in H2 but plenty of oil over the medium term. That is roughly in line with my own view, which is pretty remarkable given the falling US rig count.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.