We are releasing the latest data from our household surveys to January 2020 relating to segmented buying intentions and home price expectations. This is using data from our rolling 52,000 households nationally.

In overview, households have got the memo from the Government, that home prices are expected to rise – and this is influencing their forward expectations and buying intentions; to an extent. However, high prices and the significant debt burden, along with no income growth, and overall financial pressures are working against this intent. And property investors remain on the side-lines while first time buyers are lining up to take advantage of the Government scheme which has just commenced. There are 10,000 guarantees available now, and a further 10,000 in the next financial year. Not enough to meet demand.

As normal we will begin with our cross segment comparisons, before looking in more detail at the highlights of specific groups.

The intention to transact in the next 12 months is supported by two segments, first time buyers and down traders. The former are trying to get into the market for the first time, the latter are trying to exit the market to release capital. There are net more exits than entrants, so this suggests a supply demand disequilibrium. Investors remain sidelined.

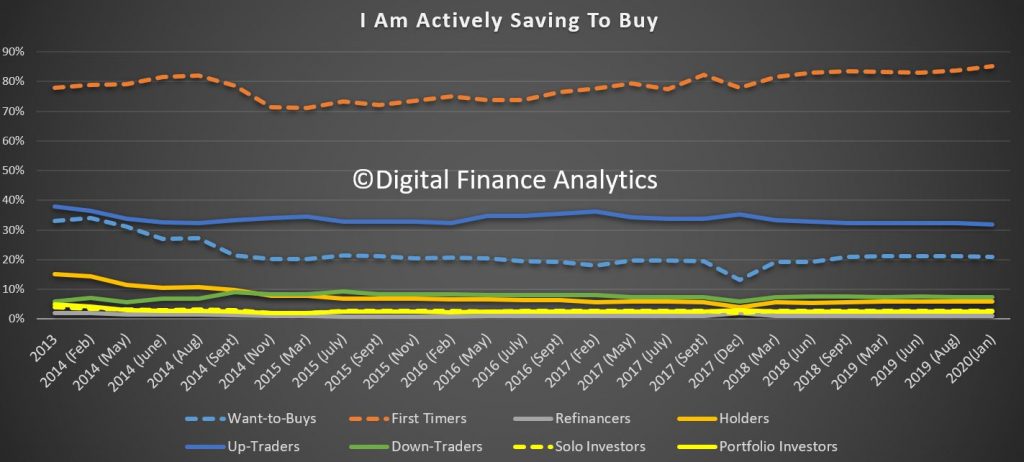

We find that first time buyers and want-to-buys are savings hard, though lower interest rates are making the task harder. Up traders (people planning to up-size) are also saving, but at a slightly slower rate.

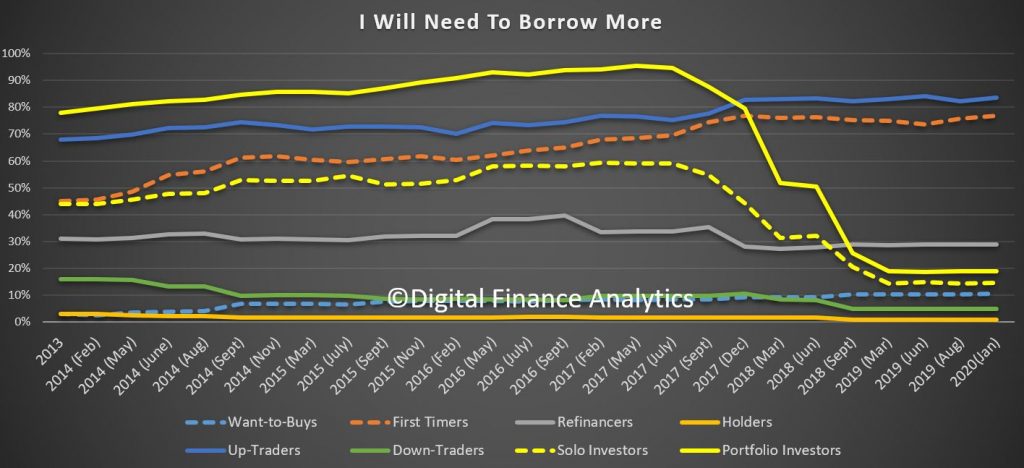

The intention to borrow is an important measure as it drives prospective mortgage growth ahead. The survey results suggests demand will be anemic and be driven by first time buyers and up traders, rather than investors. Not enough to suggest a significant lending recovery, yet.

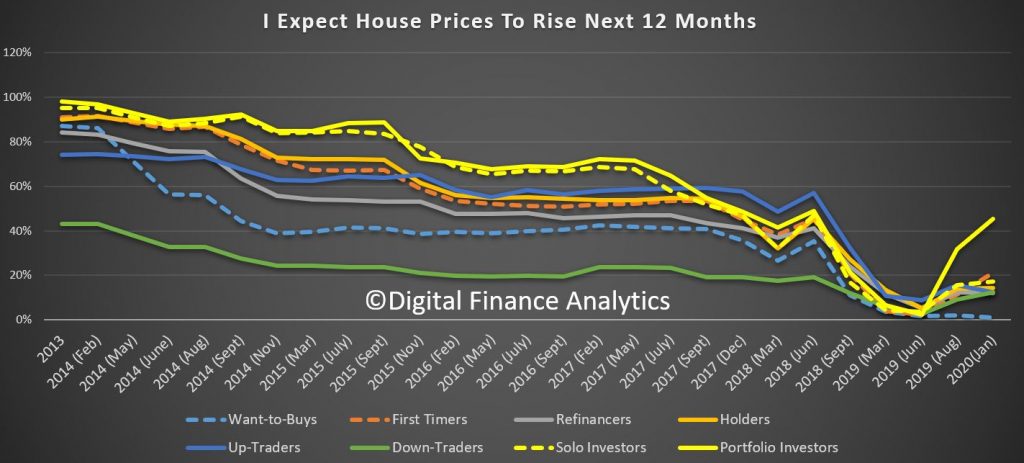

Price growth expectations are rising, led by property investors, up 14% from September, and first time buyers up 10%. Other segments appear less convinced however.

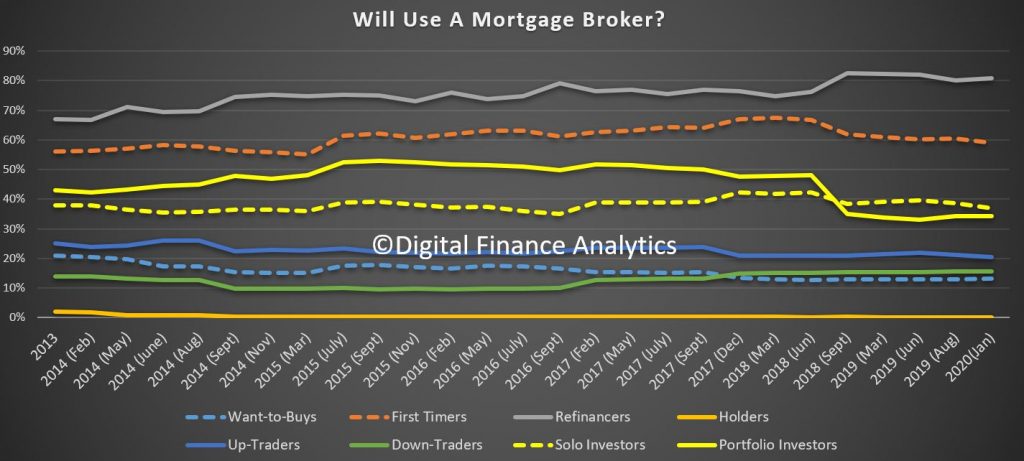

Across the segments, the preference for using a mortgage broker remains close to longer run averages.

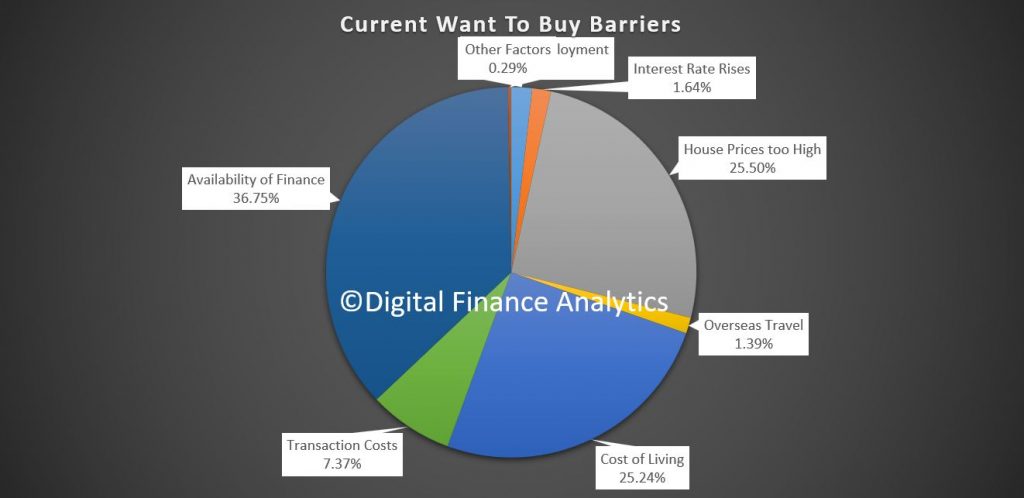

Now, looking in more detail at the segments, those 500,000 households wanting to buy are largely limited by access to finance (37%) (often because their incomes are insufficient or uncertain), that prices are too high (26%), high costs of living (25%) and transaction costs, like stamp duty, LMI premiums, and legal costs (7%).

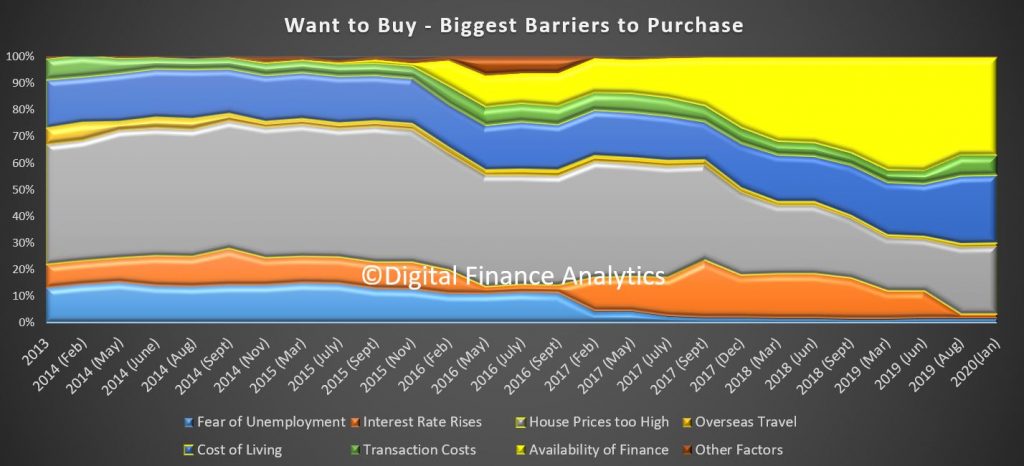

In trend terms, the availability of finance has eased, down from 43% to 37%, while high home prices and rising costs of living have become a more significant barrier recently.

Turning to first time buyers, there are around 350,000 households who are actively saving with an intention to buy when they can, and the count has been rising in the past few months, partly thanks to the announced Government-back deposit scheme, which is discussed recently in our post: First Time Deposit Scheme: Fish Or Fowl? Loan approvals are running around 10,000 per month, so only a small proportion of the first time buyer pool will be able to take advantage of the scheme, which may put upward pressure on property in the target zones! 22% intend to use the scheme, so more than the guarantees available.

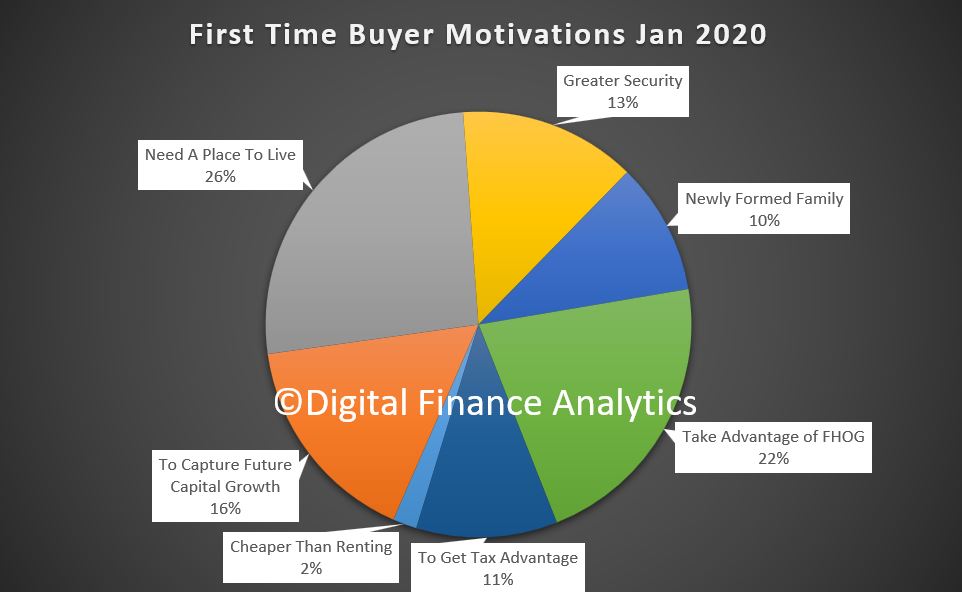

First time buyers are motivated by needing a place to live (26%), with greater security than renting (13%) and to capture future capital growth (16%), or tax advantages (11%). Around 10% transact as part of a newly formed family.

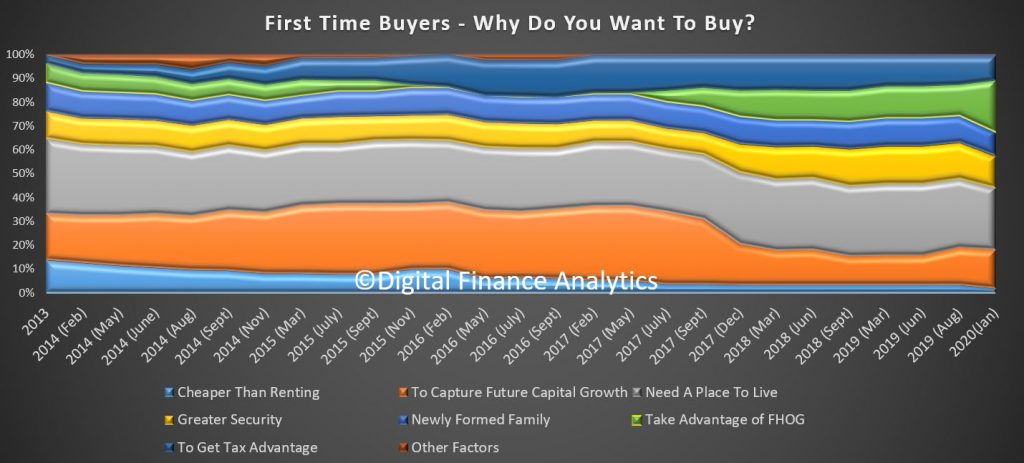

The trends highlight the impact of the new Government scheme, and the rising expectations of future capital gains, compared with a few months ago.

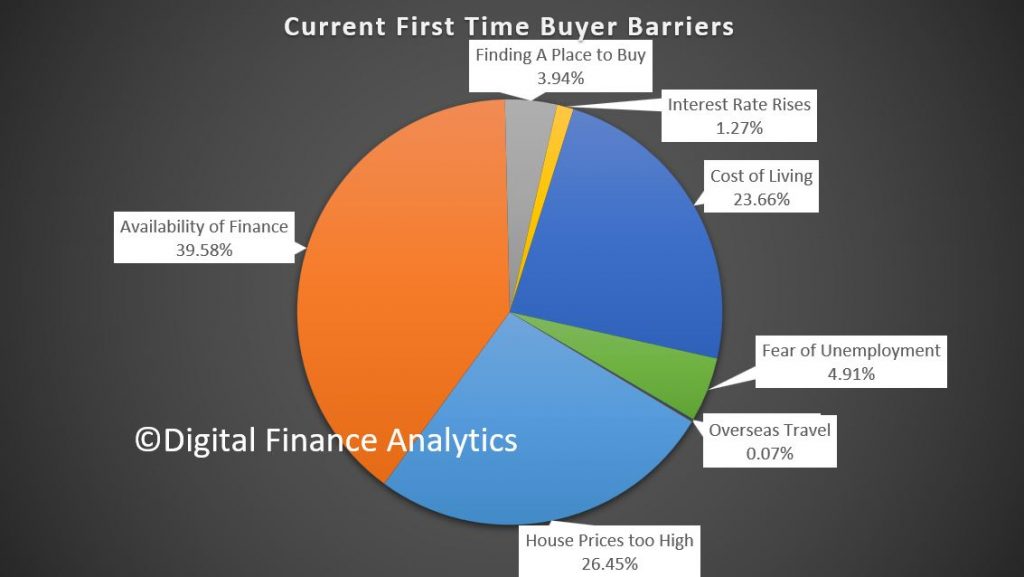

But first time buyers are still facing considerable barriers, including availability of finance (40%), prices too high (26%) and pressure from costs of living rises (24%). Property availability and fear of rising interest rates have both dissipated.

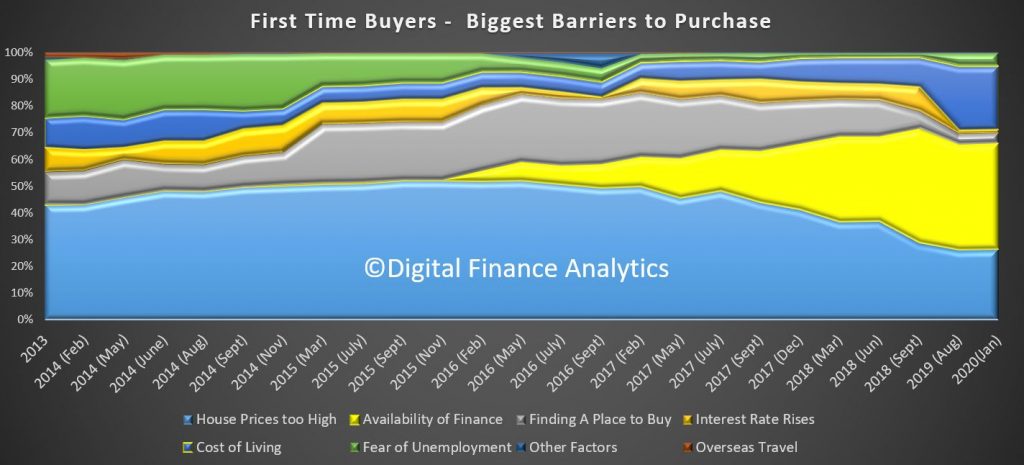

The trends highlight how finance availability remains an issue, and home price concerns are rising again, while there has been a big spike in costs of living in recent times. So many will struggle to buy.

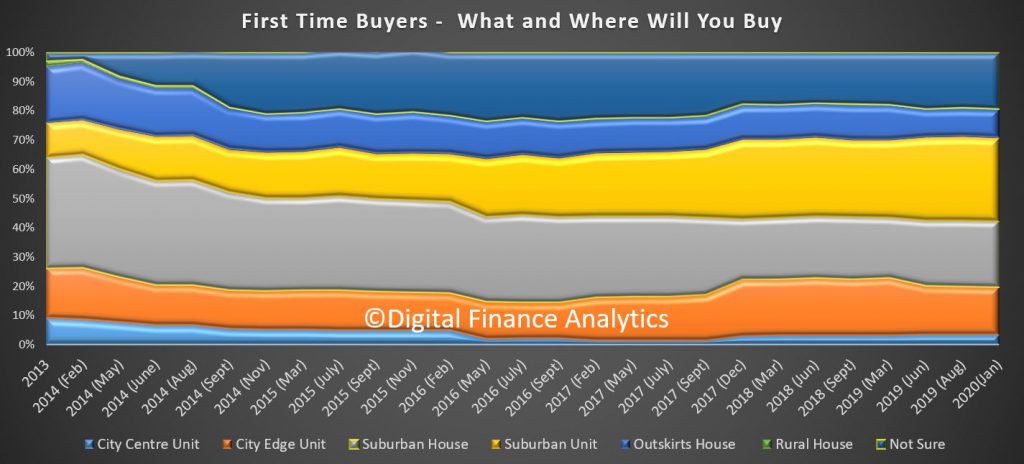

We also see a greater focus on purchasing houses rather than units, a reflecting on the bad publicity in recent times relating to the poor quality of construction and flammable cladding issues.

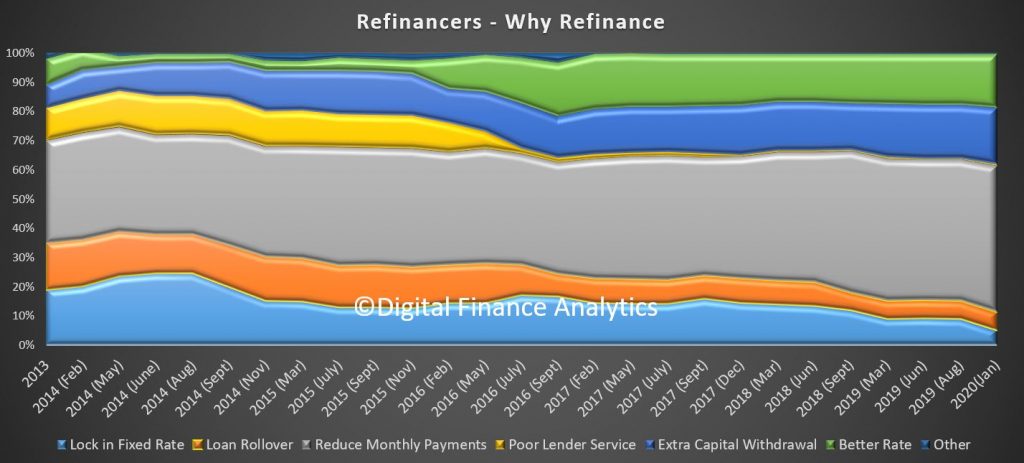

Turning to refinancing, we see the primary motivation is to reduce monthly costs (50%) , capital extraction (19%) and seeking a better rate (19%). Intention to lock in a fixed rate has fallen to 5%, on the expectation that rates will fall further ahead.

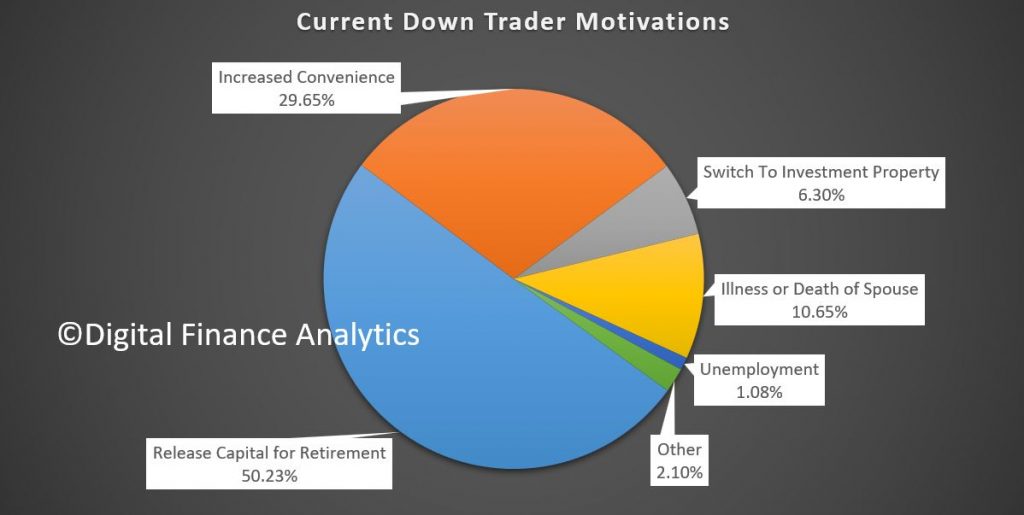

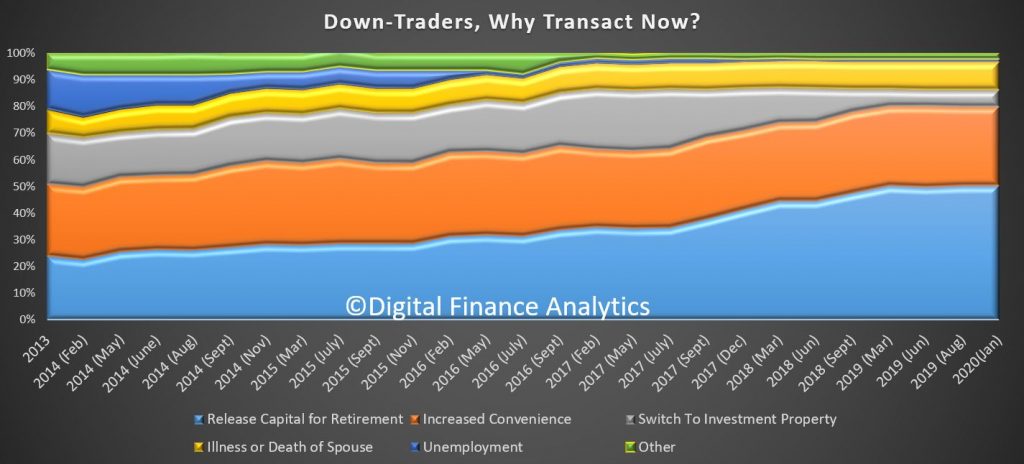

Among those seeking to sell and release capital – and perhaps buy a smaller place – our down trader segment, with more than 1.2 million are in this category, and 56% are hoping to transact. The main drivers are to release capital (56%), increased convenience (30%) and illness or death of spouse (11%).

In trend terms, interest in investment property remains at a low 6%, compared with 23% back in 2017.

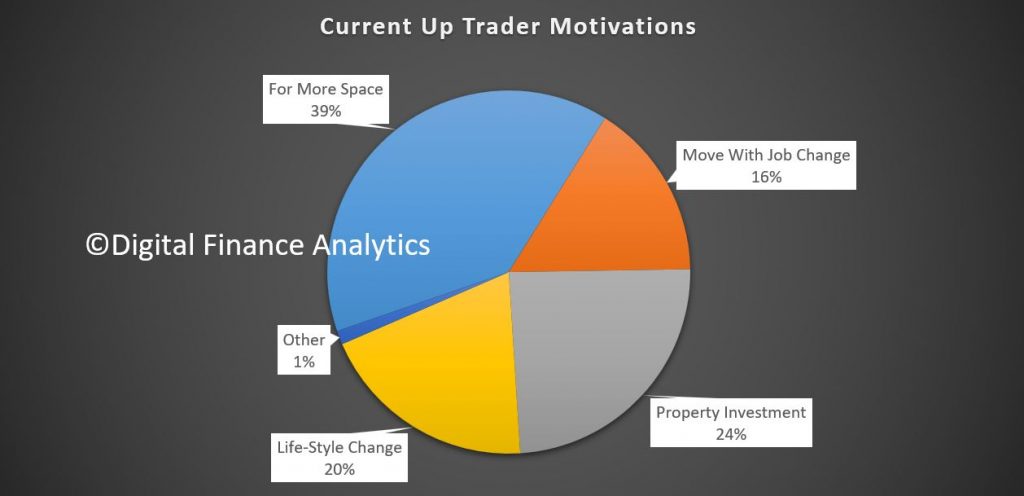

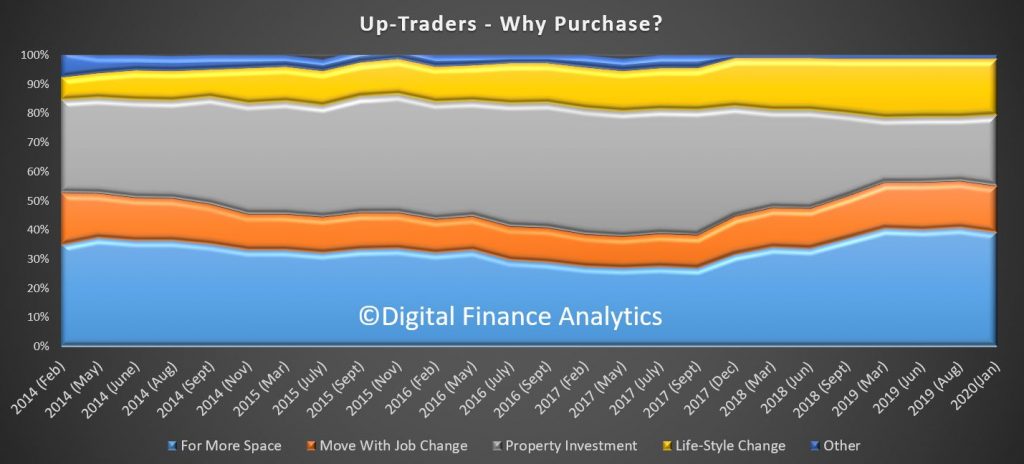

Up traders remain active but there are around 500,000 actively in this category. The main motivations are a desire for more space (39%), life-style change (20%), and job change (16%). 24% are driven by the expectation of future capital growth.

The trend tracker shows the property investment driver is weaker now, while more space and life-style are stronger drivers.

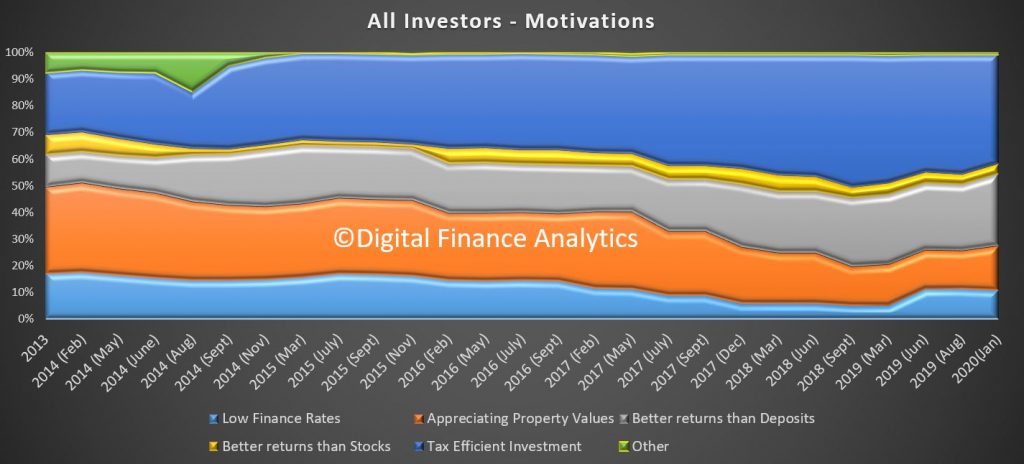

Turning to property investors, tax efficiency features as the strongest driver at 41%, down from 50% back in 2018. Better returns than deposits rose to 27%, reflecting the recent cash rate cuts. Low finance rates also feature at 11% and appreciating property values at 17%, higher than a few months ago. Within the investor segments, portfolio investors (those with multiple investor properties) are most hopeful of capital growth.

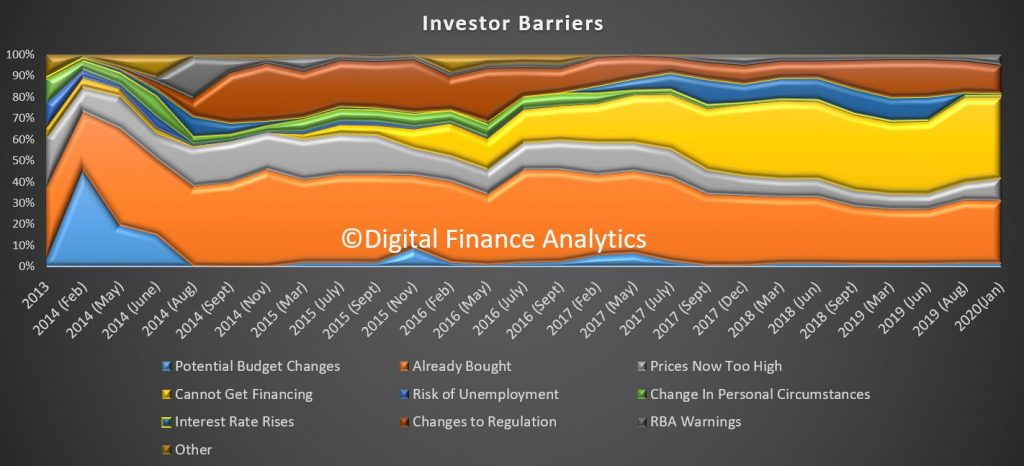

Barriers for investors include they have already bought property (30%), they cannot get financing (38%), down 2% from September, and changes to regulation (13%), including tighter rules on income and cost assessments.

There are around 1.3 million property investors, and many remain on the sidelines, due to low rentals, higher vacancy rates, and financial pressures. Of course the switch from interest only loans continues to bite too.

So, in summary, while there are some signs of interest in property, the segments really active are primarily first time buyers, and those trading down and up. There are more sellers than buyers in these groups, so if investors remain on the sidelines, we doubt prices can continue to drive higher, unless mortgage lending really accelerates (who would borrow?) or rules on loan serviceability are loosened further. The first time buyer deposit scheme will not be sufficient to turn the market around, though it may help some builders to shift newly completed or vacant property in the short term.

Nevertheless, households appear more bullish about future home price growth than a few months back – despite the fact the levers of growth appear disconnected from reality judging by these survey results.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.