DXY was up again last night:

The Australian dolar bounced a little too:

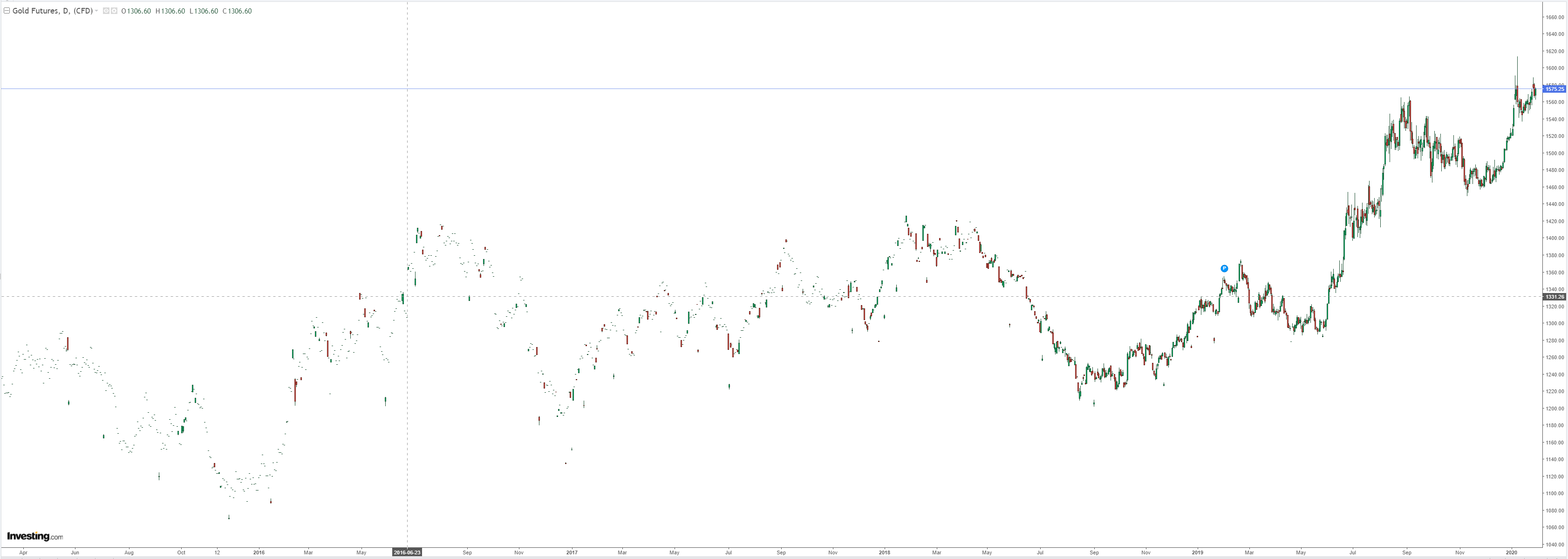

As did gold:

Not oil:

Nor metals:

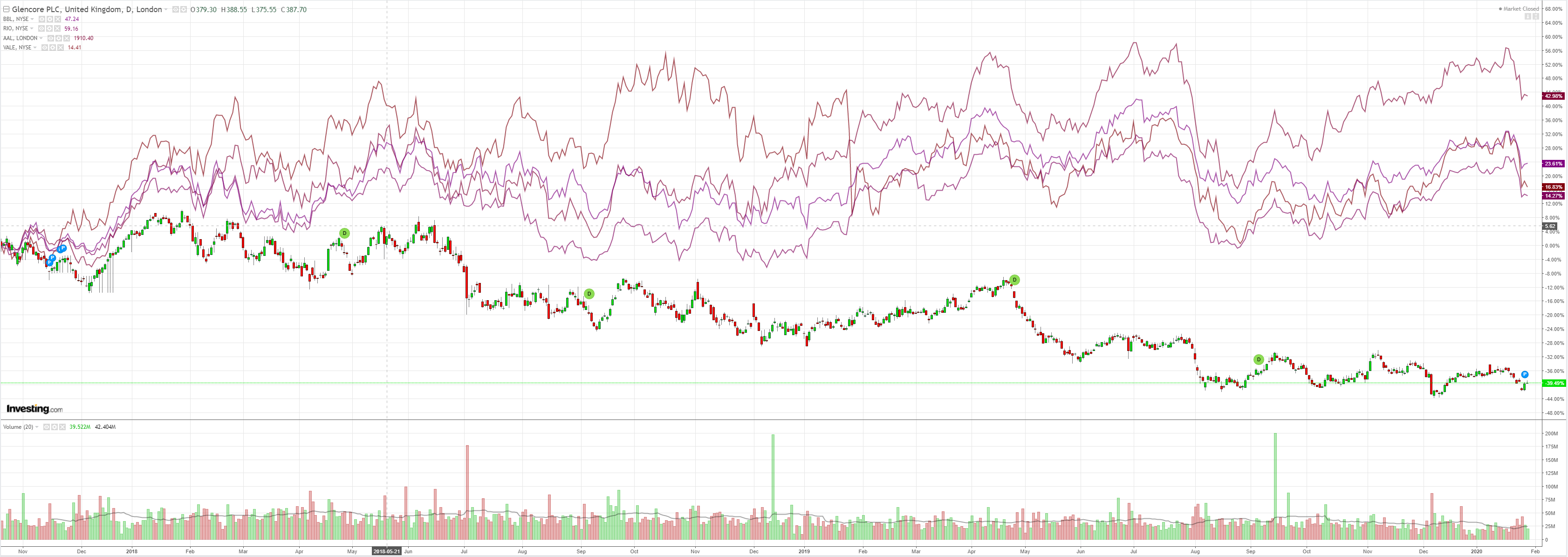

Big miners are clinging on:

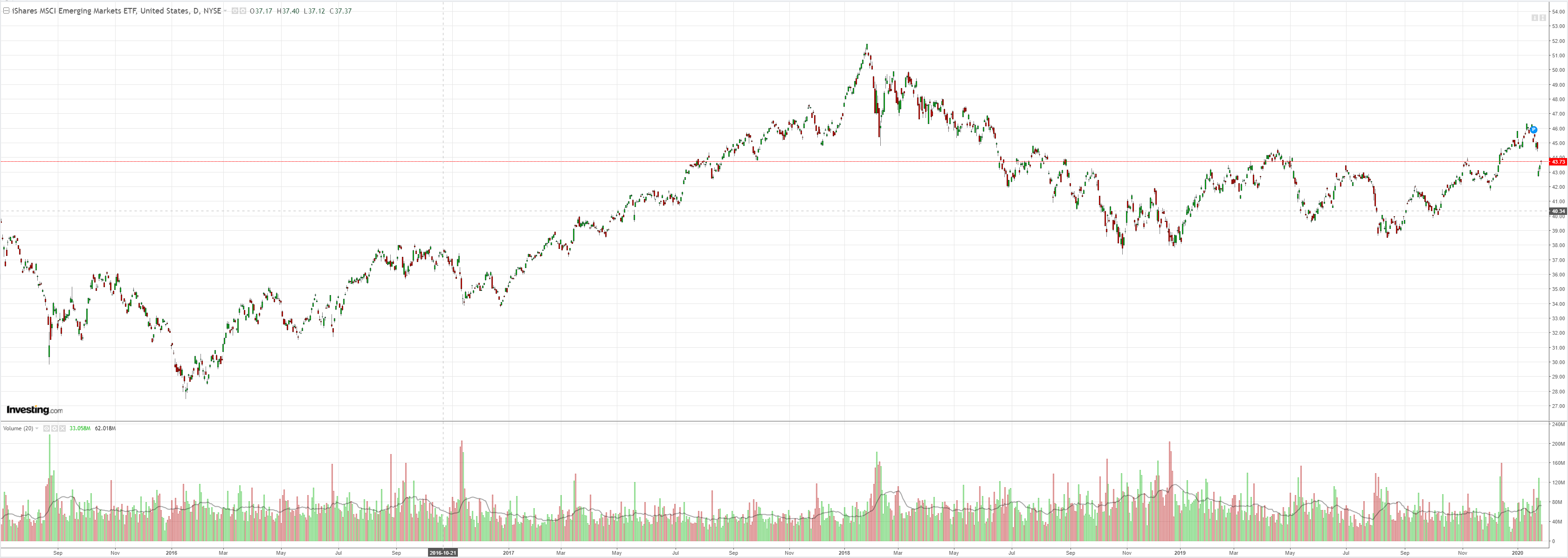

And EM stocks:

Junk should not be so strong:

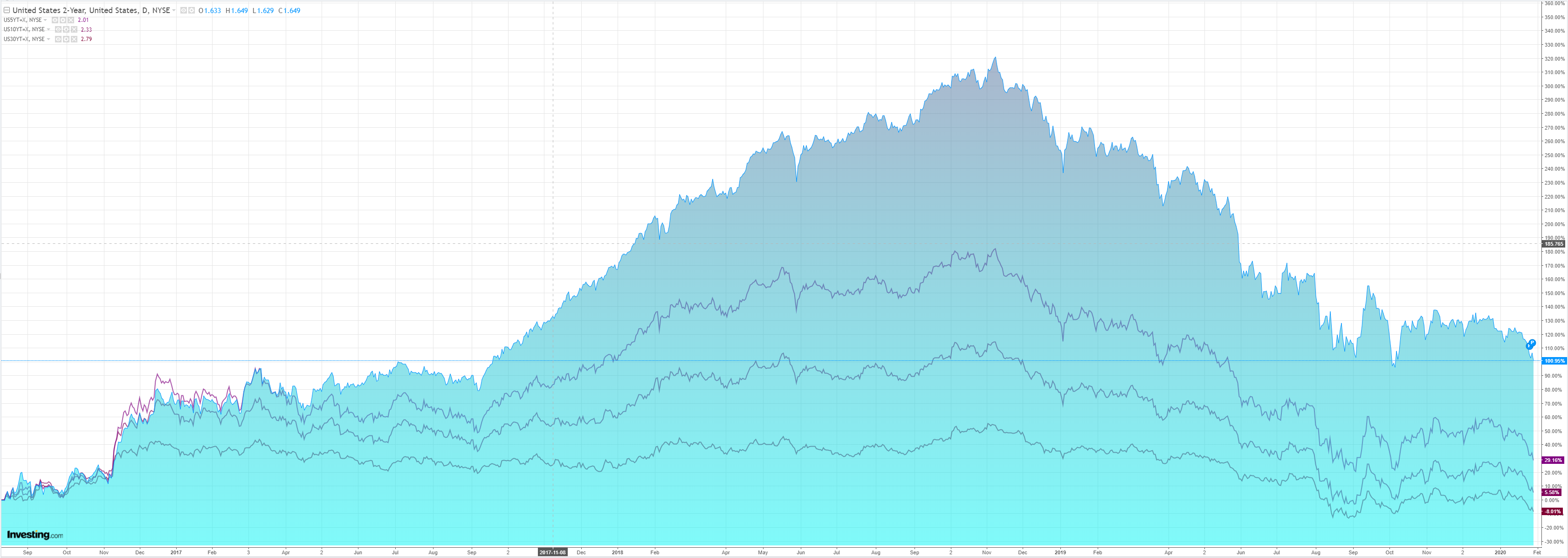

But bonds are tearing it up:

Supporting stocks:

Westpac has the data wrap:

Event Wrap

As was widely expected, the FOMC kept its main policy rate unchanged with a target range of 1.50%-1.75% and repeated its guidance from the December meeting – that settings are “appropriate to support sustained expansion of economic activity”. There were some minor narrative tweaks, with policy deemed appropriate to support “inflation returning to the committee’s symmetric 2% objective” (vs supporting inflation “near” the 2% objective). It downgraded its assessment of household spending to “moderate” (vs “strong”). The decision was unanimous (10-0), as was December’s.

Coronavirus update: China has confirmed 6,065 cases, with 132 deaths. There have been no reported deaths outside China.

The EU Parliament approved (voting 621 to 49) PM Johnson’s Brexit deal, allowing the UK to leave the EU (which it joined in 1973) on 31 January with an agreement over exit terms and a transition phase.

Event Outlook

Australian import prices are expected to rise by a modest 0.5% in Q4 on the back of higher fuel prices and a weaker AUD. Export prices are, in contrast, expected to fall sharply (circa 5%) due to a pull-back in commodity prices.

In New Zealand, the trade position is expected to narrow in December to be broadly balanced, a seasonal lift in dairy exports supporting.

In Europe, confidence indicators will be released for January, so too the unemployment rate for December. All should remain constructive for the outlook. However, the main event in European trade will be the BoE policy decision. No change is expected at this meeting, but the signalling of an impending move is.

In the US, Q4 GDP is likely to print in line with potential, circa 1.7%. Business investment remains weak, and now consumer discretionary spending is moderating. Below-trend growth is our expectation come 2020.

The Fed administered the vaccine of last resort to the Australian dollar:

Information received since the Federal Open Market Committee met in December indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a moderate pace, business fixed investment and exports remain weak. On a 12‑month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee decided to maintain the target range for the federal funds rate at 1‑1/2 to 1-3/4 percent. The Committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation returning to the Committee’s symmetric 2 percent objective. The Committee will continue to monitor the implications of incoming information for the economic outlook, including global developments and muted inflation pressures, as it assesses the appropriate path of the target range for the federal funds rate.

That she’ll be right attitide help stabilise risk and the AUD.

Good for a day but nothing has changed. The virus gets worse and the AUD crashes. The virus improves and up she goes.

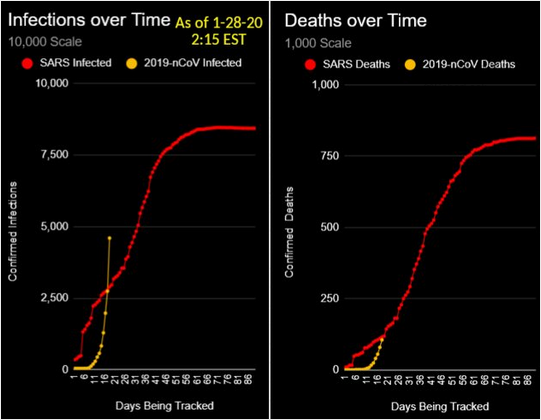

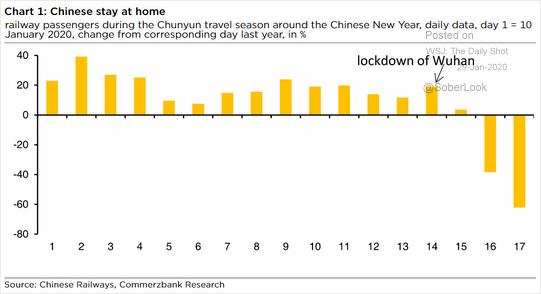

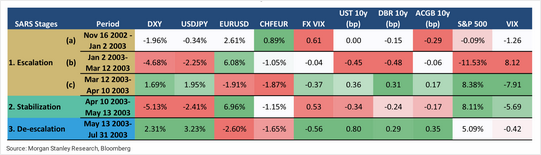

The signs versus SARS remain poor:

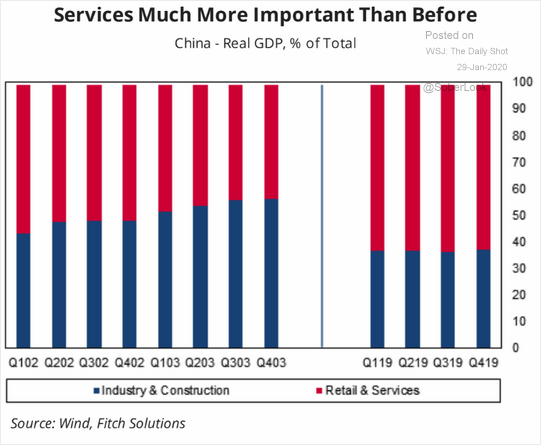

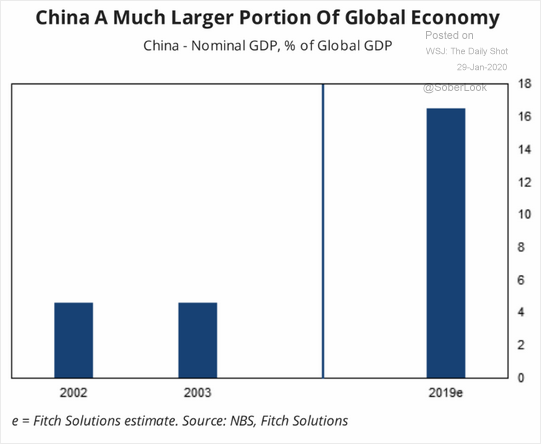

People-to-people services a much bugger economic segment now:

Yuk:

Global fallout larger too:

It should be worse than SARS:

I still see lower.