by Chris Becker

Housing prosperity continues to fall as house prices hit another high in the December quarter – up 4% according to CoreLogic:

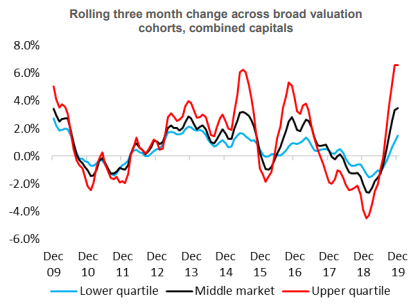

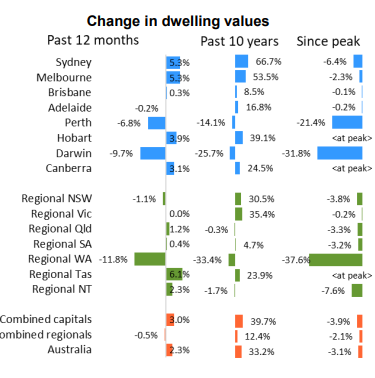

Dwelling values rose by 1.1% over the month of December and by 4.0% over the quarter to finish out 2019 on a positive note according to the CoreLogic national home value index. This result represents the fastest rate of national dwelling value growth over any three month period since November 2009. Darwin was the only region amongst the capital cities and ‘rest-of-state’ areas to record a fall in values over the month, with a -0.5% decline.

CoreLogic head of research Tim Lawless said, “Although the monthly capital gains trend remains fast-paced, the 1.1% rise in December was softer relative to the 1.7% gain in November and the 1.2% rise in October. This would suggest that the pace of capital gains may have been dampened by higher advertised stock levels or worsening affordability pressures through early summer.”

Here’s the full release: