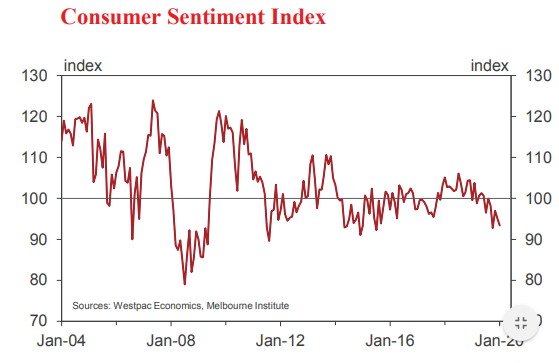

It is entirely reasonable to have expected that the Index would have fallen during this period of devastating bushfires. Perhaps it is somewhat surprising that the fall in the Index was not more severe particularly in light of the 5.8% fall we saw during the Queensland floods in 2011.

However the fall in the Index during the floods was from 111.0 to 104.6 – overall confidence levels during that period were very high – much higher than we are currently experiencing.

Indeed, since the lows of the Global Financial Crisis where the Index averaged only 89 over a 15 month period from March 2008 to May 2009 there have only been seven monthly readings where the Index has printed below 93.4.

In short, Confidence has been further eroded by the bushfires but because the Index was starting from such a modest level it was likely that the fall in Confidence would be less than some may have expected.

Arguably, because the survey occurred in a week where there was widespread rain the negative impact of the bushfires was somewhat reduced. If the survey had been conducted a few weeks earlier then the Index is likely to have fallen by even more, notwithstanding the very low starting point.

This low level of Confidence is consistent with the generally lack lustre reports on consumer spending. The surprising jump in retail sales which was reported for November is likely to have largely reflected the “Black Friday” effect. A more widespread boost to spending will be required before there are credible grounds to dispute the downbeat signals associated with the consistently low levels of the Index.

Apart from the fires, which would have been the dominant influence on Sentiment for this survey, other factors should have been somewhat supportive. Optimism around financial markets and the global economy has lifted, with the Australian share market up by 6% since the start of the year.

Furthermore, the housing related components of the survey also pointed to ongoing confidence in the housing market.

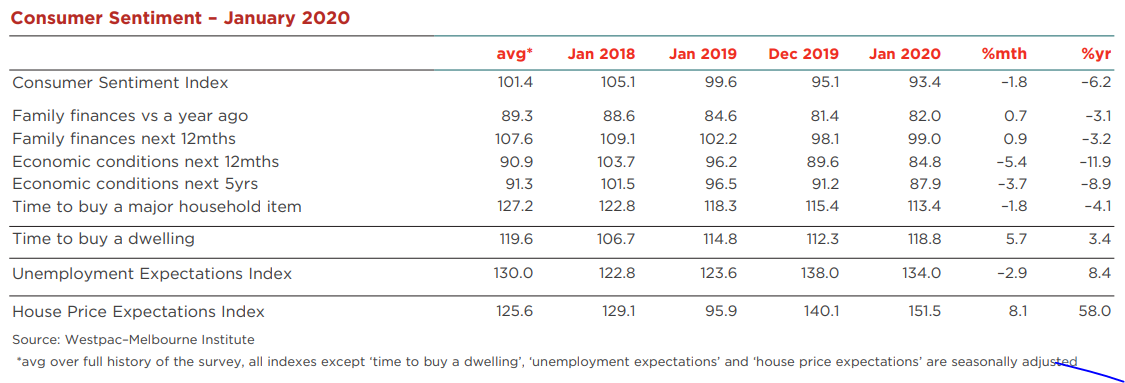

All the economic components of the Index recorded declines in January.

The ‘economy, next five years’ sub-index fell 3.7% in January and the ‘economy, next 12 months’ sub-index fell 5.4%. Both are down sharply on a year ago (–8.9% and –11.9% respectively).

The ‘time to buy a major household item’ sub-index fell 1.8% in January. At 113.4, the sub-index is well below its long run average of 127 and 4.1% down on last year, suggesting consumers are likely to be extra cautious, particularly in December and January.

Consistent with improved performance of financial markets and housing we saw the “own finances” components remain broadly steady.

The ‘finances vs a year ago’ sub-index rose 0.7% in January and the ‘finances, next 12 months’ sub-index increased by 0.9%.These components are down by 3.1% and 3.2% respectively on a year ago.

The Westpac-Melbourne Institute Unemployment Expectations Index fell 2.9% to 134 in January, up 8.4% on this time last year (recall that higher readings indicate that more consumers expect unemployment to rise in the year ahead). The readings are consistent with a slowdown in jobs growth and steady increases in the unemployment and underemployment rates over the year ahead. Note that Westpac is expecting the unemployment rate to lift to 5.6% from 5.2% over the course of the first half of 2020.

Housing-related sentiment was strong in January, with views on time to buy lifting while price expectations continued to surge.

The ‘time to buy a dwelling’ index rose 5.7% in January to 118.8, nearing the long run average of 120. Despite the increase in this index we expect that it has peaked in this cycle. The index is down by 6.4% from its peak in August, shortly after the low point for prices which occurred in June.

Note that, similarly, the index bottomed out at 90.0 in May 2017 – coinciding with the peak in prices in the previous cycle.

On that basis (current level of 118.8 compared to low point of 90.0 in the previous cycle) it certainly appears that price gains have further to run. If, as we expect, this Index loses ground through 2020 then the pace of house price appreciation may slow. Sydney’s low point in the previous cycle was 74 in May 2017. Melbourne’s low point was 83 a little later in August 2017. Currently the Sydney index sits at 117.4 and Melbourne’s is at 105.8, off recent peaks of 130 and 133 respectively.

The Westpac-Melbourne Institute Index of House Price Expectations Index rose 8.1% in January to 151.48, up a staggering 58% over the year. While the Index has reached higher levels in previous price cycles the boost in optimism has not been as dramatic as we are witnessing in this cycle. Before, the previous peak (which had outstripped the current level of 151.48) the annual lift in the index was “only” 26.7%.

“The “Time to Buy” Index and the “House Price Expectations “Index are both likely to provide useful lead indicators of the shape of this current house price cycle. For now, the indexes are indicating that this current period of positive price action is unlikely to end in the near term.

The Reserve Bank Board next meets on February 4. Westpac expects that the Board will decide to cut the cash rate by 0.25% to 0.5%.

Markets are not convinced. Market probabilities for a rate cut are priced at around 50%.

The other complication around this meeting is that there has, understandably, been no public communication from the Reserve Bank for the weeks of the holiday period.

The minutes of the last Board meeting therefore take on considerable importance. From our perspective the key observations were that the Board would review the outlook in February (unusual to be so specific in minutes); the ongoing concern with weak wages growth; and the emphasis on the effectiveness of monetary policy.

In fact, the Governor has previously emphasised the boost to spending from a positive wealth effect of higher house prices and the direct impact of rising housing turnover on expenditure on household goods.

There has been recent media criticism about the effectiveness of monetary policy but the Reserve Bank Board is very clear in the minutes, “While members recognised the negative confidence effects for some parts of the community arising from lower interest rates, they judged that the impact of these effects was unlikely to outweigh the stimulus to the economy from lower interest rates”.

Finally, it is always reasonable to point to the limited further scope the Reserve Bank has with respect to easing rates. However the Board has also been clear on that point, arguing that it is the level rather than the change in rates that counts, so if lower rates are needed then best to move regardless of whether there is limited further scope.

The decision to cut the cash rate in February is also expected to be supported by a downgrade in the growth forecasts for 2020.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.