As our clients will know, we have long been sceptical about the accuracy of China’s official GDP data. To gain a better insight into true economic activity we developed the China Momentum Indicator (CMI), first published in 2014. This combined rail freight volumes, electricity production and nominal bank lending; all three of which were identified by Premier Li Keqiang as providing a better gauge of economic activity than the official estimate of GDP. Since then we have expanded our measure so that it better reflects new-model growth, with our latest estimate (the CMI 3.0) combining twelve measures of economic activity, including retail sales, unoccupied housing and net trade. Although the headline measure is similar to its predecessor, the CMI 2.0, there are key differences in the way that we now capture China’s trade and housing data, as well as small methodological adjustments. According to our CMI 3.0, the slowdown in China’s economic activity halted around the middle of last year, with our most recent reading nudging up to 4.7% in the twelve months to November.

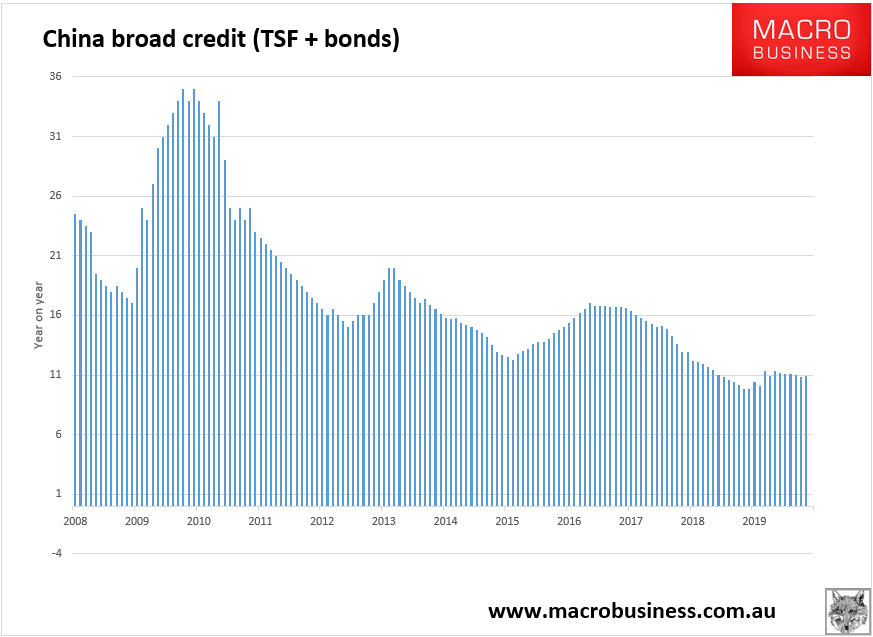

I completely agree. There is nothing to suggest an imminent Chinese growth lift. Indeed, the key leading indicator of broad credit suggests ongoing slowing:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.