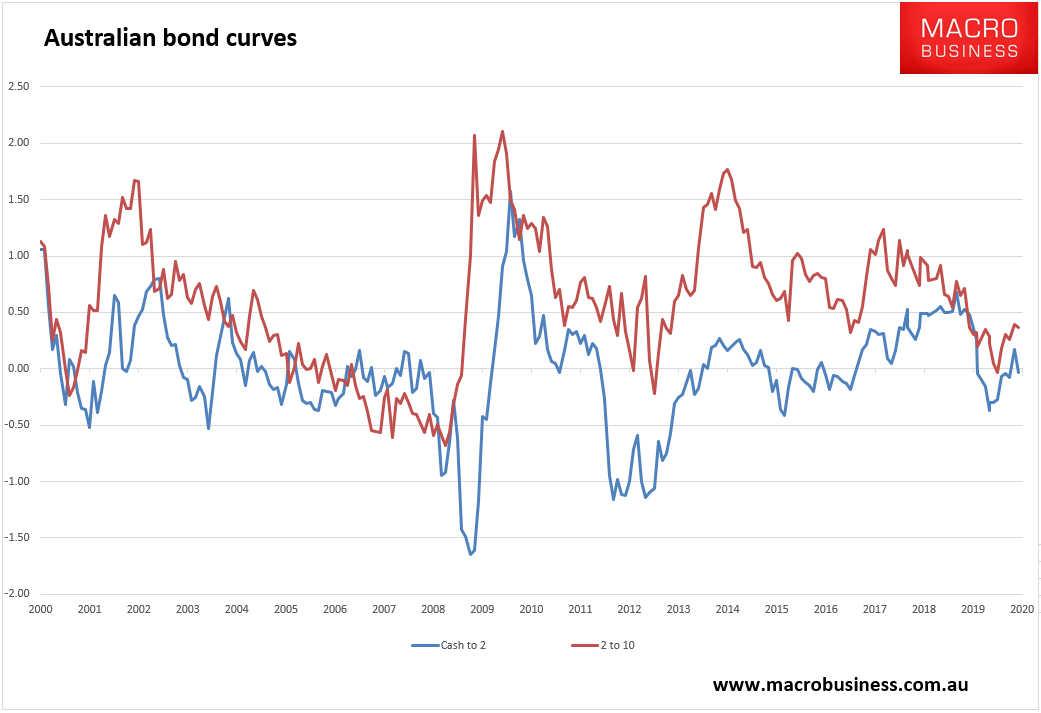

And it ain’t pretty. The Aussie bond market boom is back with more 2020 highs (yield lows):

It has steepened a little since last year, but the curve is still inverted out to the five year indicating weak growth at best and high recession risk for years ahead:

Advertisement

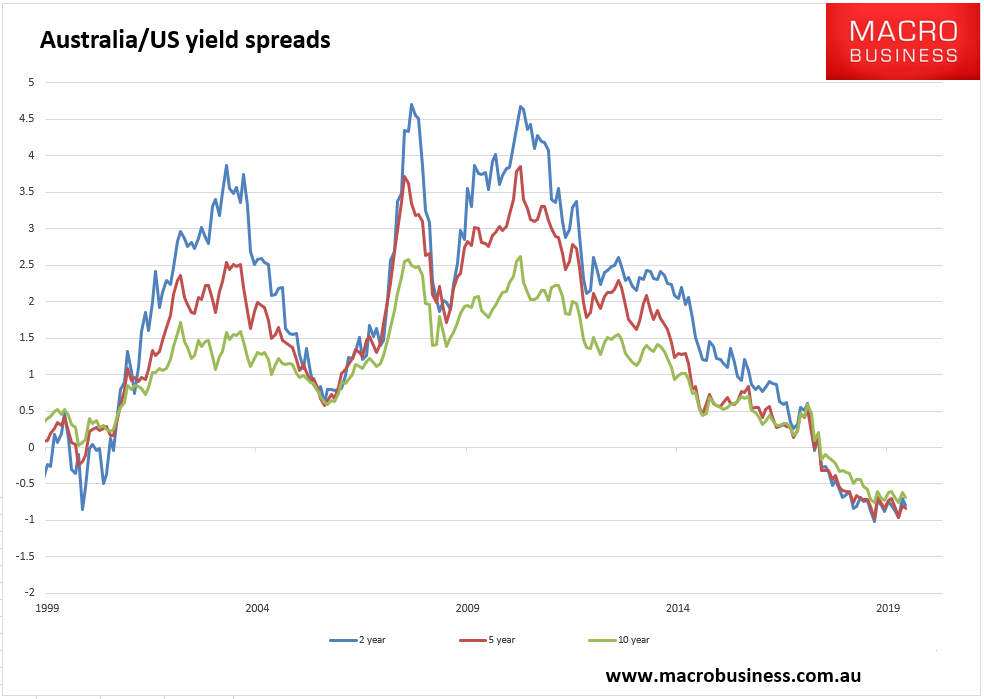

In turn, this has spreads falling versus the US again: