Below is preliminary analysis from Westpac Economics on the economics of the current bushfire crisis:

Summary

Bushfires are currently affecting large parts of south eastern Australia with elevated risk of further fires in coming weeks.

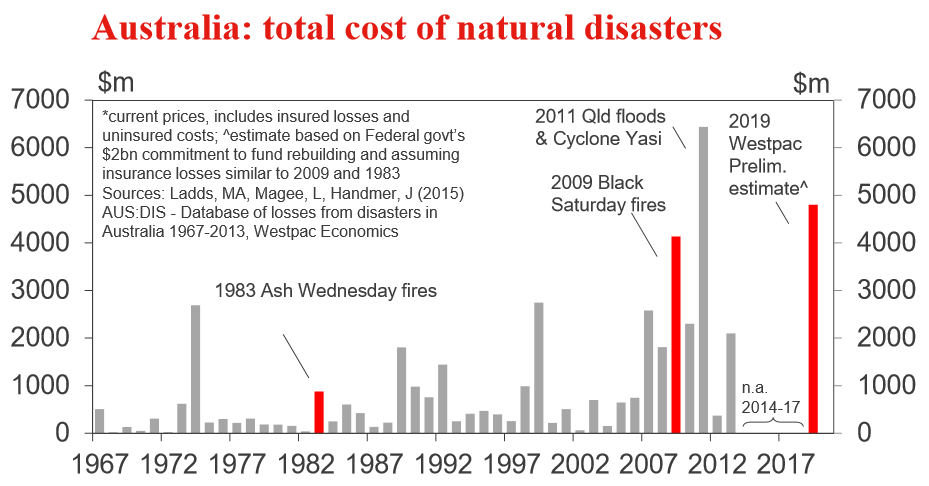

We estimate total losses to date are likely to be around $5bn – higher than the 2009 bushfires in Victoria but smaller than the Queensland floods in 2010-11.

The economic impact is highly uncertain. Activity in the most severely affected areas accounts for around 1% of the Australian economy and is focussed on agriculture and tourism.

Initial indications suggest the main direct negative impacts will be on local tourism activity with potential disruptions from smoke pollution affecting the major capital cities. Indirect effects through a hit to confidence and impacts on the wider tourism industry are much harder to assess but could be similar in scale.

Our balance we see a total GDP impact of 0.2-0.5%.

Insurance figures suggests 2019 similar to 2009

The Insurance Council of Australia declared a bushfire catastrophe on Nov 8. As at Jan 10 there have been 10,550 claims lodged with an insured valued of $939m. The Council estimates that 1,838 insured homes have been destroyed within the fire region.

By way of comparison, the most recent large bushfire disasters in Australia were in 2009 (the Black Saturday fires in Victoria) and 1983 (the Ash Wednesday fires in Victoria and SA). The 2009 fires saw 2,029 homes destroyed, and the 1983 fires saw 3,700 homes destroyed. Both resulted in insurance losses of $1.8bn (in 2017 prices).

A rough rule of thumb for disasters is that the total cost – including both insured and uninsured losses requiring government assistance – is about double the insured loss.

Total cost of the disaster to date likely to be ~$5bn

Initial estimates suggest the cost of the disaster to date is comparable to the ‘Black Saturday’ fires in Victoria in 2009, which saw 2,029 homes destroyed but a much higher loss of life. That would put the cost in terms of insured and uninsured losses at around $5bn.

Note that this is smaller than the impact of the 2010-11 Queensland floods which had an estimated total cost of $6.4bn. Bushfires in general tend to incur less damage than other disasters due to the more localised nature of the event.

Much of the loss associated with bushfires will be met by insurers.

Alongside this, the Federal government has designated $2bn over two years to help rebuild bushfire affected regions. It can also draw down $150mn a year (possibly more) from a $3.9bn Emergency Response Fund created in the April budget. The NSW state government has also allocated $1bn over two years to help rebuild affected areas.

Economic impact highly uncertain

Assessing the economic impact of disasters is always very difficult, particularly when the full extent of damage is still unknown.

There are additional challenges in assessing the impact of the current bushfires stemming from:

pre-existing drought conditions

many agricultural producers would have already been operating at low levels;

complex seasonality – including a mix of low activity for businesses that close over the holiday period, high activity for most tourism operators and diverse patterns within the agricultural sector;

smoke haze over major capital cities

an element that has not been a prominent feature of previous bushfires.

Adding to this, previous major bushfires in 2009 and 1983 also coincided with major economic developments, the GFC and early-80s recession, that make their impact difficult to quantify.

A negative shock followed by rebuild stimulus

It should be noted that the standard profile of the economic impact of most disasters is an initial negative shock followed by a positive shock as recovery and rebuilding occurs.

The size of the negative shock typically relates to the extent to which regular activity is disrupted – i.e. reflecting both the scale and the duration of any disruption. Both are heavily influenced by the damage to infrastructure – power, transport, water etc. Bushfires typically result in less damage to infrastructure than other disasters although this is an aspect that bares close monitoring with key risks around power transmission, transport and the potential contamination of water supplies.

The period of above trend economic activity that follows typically relates to rebuilding, particularly housing, much of which is insurance funded and comes through gradually. Initial figures suggest this could add about 0.3-0.5% to new dwelling completions over a two year period.

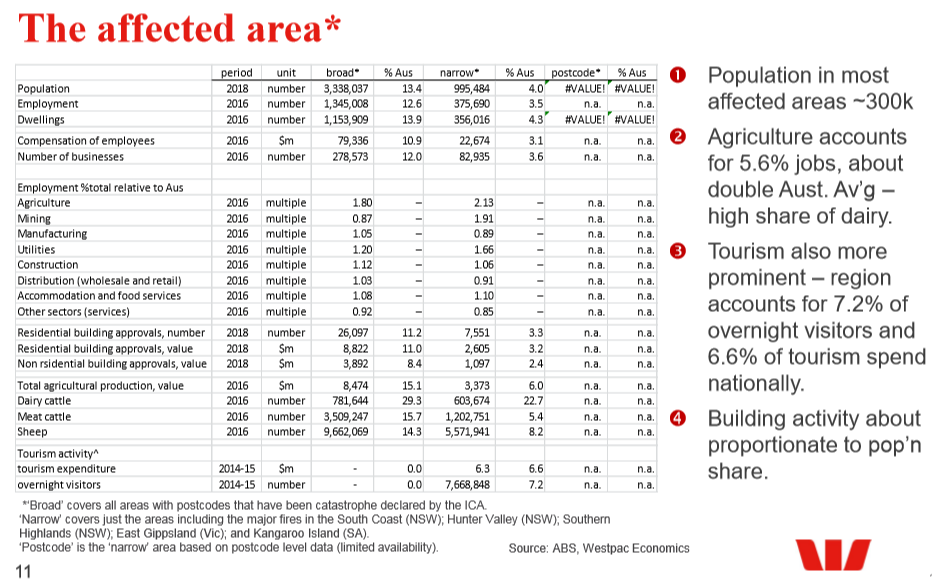

Most severely affected area ~1% of economy; agriculture & tourism focussed

The most severely affected areas account for about 1% of the Australian economy, the wider regions around these areas is closer to 3.5%.

Agriculture and tourism are the dominant sectors – directly accounting for 16% of total employment in the wider areas. This is likely to be much higher once related sectors are included, i.e. agricultural suppliers and processors, tourism-linked retailing etc.

The wider area accounts for a particularly high share of dairy production, accounting for 22.7% of all dairy cattle in Australia, and incorporates some significant wine-making regions.

The wider tourism regions account for 7.2% of overnight visitors and 6.6% of tourism spending nationally.

Mining and utilities are also more prominent in the wider area. Building activity is about proportionate to population share.

Estimated economic impact: 0.2-0.5% off GDP

Population: 1mn in areas around major fires (4% of Aus) with 300k in most heavily affected postcodes (1.2% of Aus). Employment: 375k in areas around major fires (3.5% of Aus).

Direct impact small – applying crude population/employment ratios, assuming the broad region affected by bushfires accounts for around 2% of national GDP and assuming bushfires result in 75% below ‘normal’ activity and a recovery and rebuilding profile that returns activity to pre-bushfire levels by April this would result in a direct 0.1% reduction in annual GDP nationally.

Wider impacts on tourism, confidence and pollution disruption are much harder to assess. These could easily be of a similar magnitude and possibly larger – our initial assumption is of a combined effect in the 0.1-0.4% of GDP range.

That would give a total GDP impact of around 0.2-0.5%.

Estimated economic impact: timing and risks

Timing-wise, the main direct negatives will land in Q1 and could see a larger quarter to quarter hit of around 0.3% GDP in the March quarter. Wider effects on tourism and confidence nationally may come through more gradually. Repair and rebuilding work will provide a boost as the year progresses with the net effect likely to be a positive by year end.

While there are numerous uncertainties, we see the key risks to this assessment as being around:

The potential for further significant bushfire events in coming weeks particularly if these affect urban areas or critical infrastructure;

The size of the impact on the wider tourism sector;

The impact on consumer sentiment; and

The effects of smoke pollution on major urban areas.

Policy implications

Westpac expects the RBA to cut rates by 25bps at its February meeting with a further 25bp cut in June and a move to unconventional policy easing in the second half of the year – a view we set out prior to the bushfires.

While the bushfires may provide additional reason for the RBA to ease policy, particularly if consumer confidence is heavily impacted, it is unlikely to have a significant bearing on the RBA’s decisions.

The Bank’s response to the Queensland floods in early 2011 provides a clear guide. The Governor’s statement following the Board’s February meeting stated that: “In setting monetary policy the Bank will, as on past occasions where natural disasters have occurred, look through the estimated effects of these short-term events on activity and prices. The focus of monetary policy will remain on medium-term prospects for economic activity and inflation.”

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.