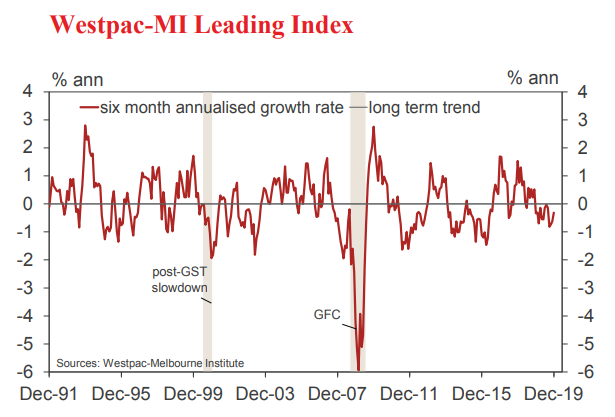

Despite the lift, the Leading Index growth rate remains below zero, indicating momentum tracking well below trend. In fact the December print represents the thirteenth straight month where the Index growth rate has been negative. This has been consistent with the persistent below trend growth we have seen for the Australian economy.

The latest update points to weak economic momentum continuing in the first half of 2020 and is consistent with Westpac’s view that growth will remain around a 2% pace in the first half of 2020.

The Leading Index growth rate deteriorated over the second half of 2019, moving from –0.03% in July to –0.32% in December. The main components driving the 0.28ppt shift have been a sell-off in commodity prices (–0.61ppts) and a more mixed performance on the Australian share market (–0.42ppts). This has been partially offset by a stabilisation in the Westpac-MI Unemployment Expectations Index (+0.25ppts) a reduced drag from declining US industrial production (+0.21ppts), a modest lift in aggregate hours worked (+0.13ppts) and a widening yield spread as the RBA’s cuts in the cash rate have lowered short term rates (+0.10ppts).

The Reserve Bank Board next meets on February 4. Westpac expects that the Board will decide to hold the cash rate steady at its February meeting. That decision will be in response to the surprise fall in the unemployment rate from 5.3% to 5.1% since the last Board meeting in December.

However, we expect that decision to be a temporary pause in the rate cut cycle. The recent falls in the unemployment rate are expected to be unsustainable with this becoming apparent by the April meeting when we expect the next cut.

It is clear that the Board is confident that lower rates will boost the economy through a more competitive exchange rate; improved cash flows to households; and rising asset prices. However, the policy debate should not be around ‘either monetary policy or fiscal policy’.

The policies are not mutually exclusive and while Westpac expects a second rate cut in August we also support the use of fiscal policy to boost demand. Our preference is to lift household incomes through bringing forward the stage two tax cuts phased over two years. A rise in expected demand should be more effective in boosting business investment than tax incentives.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.