Not much point with charts today with the US closed. A little material from Westpac gives us the right take on the immediate outlook for the Australian dollar:

RBA policy will be stretched to its maximum in 2020 – two more cash rate cuts from the RBA, to reach the effective lower bound for the overnight cash rate of 0.25%, to be followed by open-ended Quantitative Easing (QE) via asset purchases. QE will therefore be the defining feature and driver of Australian rates market price action across 2020. In the interests of minimising potential adverse market shifts, we expect the RBA to purchase both government and semi-government bonds with maturities across the term structure, rather than concentrating only on shorter maturities.

That will keep the yield curve flatter than it would otherwise have been.

Given the deterioration we expect in the US economy, as well as the view that our own labour market will come under strain in 2020, we think that there will be little reason for the market to quickly pre-empt the beginning of the next tightening cycle.

So that informs our view to maintain a “range-trading” discipline, while holding either long or neutral duration.

It is too early to adopt a strategic medium term short duration position, as neither the RBA nor Fed have completed their policy accommodation and the market is yet to fully factor-in our rate cut expectations in either market.

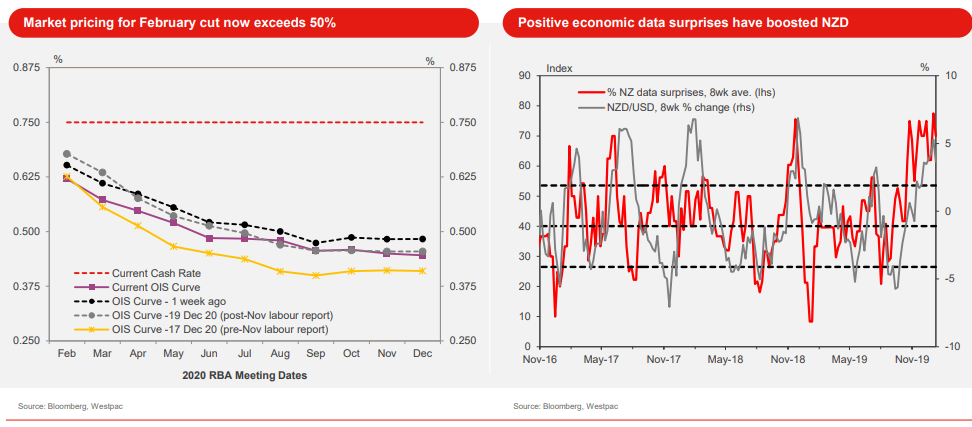

This week, the Westpac-MI consumer sentiment survey will be an important insight, especially in light of the difficult bushfire season, as will this Thursday’s first look at the employment and unemployment data, especially as there is just around a 50% chance of a February rate cut factored-in.

In terms of bonds, for now see both 3yr and 10yr maturities as firmly in the middle of their recent ranges and unlikely to shift for now. Given our policy view, we continue to remain better buyers on dips to price range lows.

Unemployment rate expected to rise to 5.3% from 5.2%

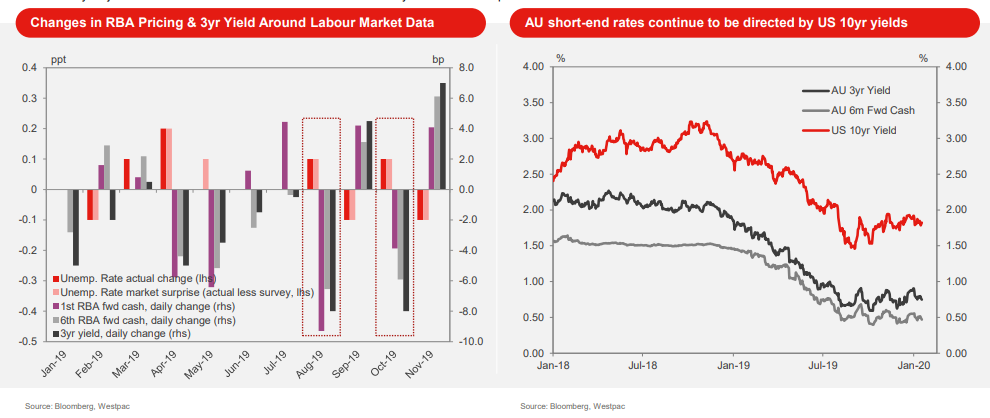

Changes in RBA Pricing & 3yr Yield Around Labour Market Data AU short-end rates continue to be directed by US 10yr yields.

Thursday’s December labour report will be of key interest this week. Westpac expects that the unemployment rate will rise to 5.3% from 5.2%, which would surprise the market where the expectation is for the unemployment rate stay constant at 5.2%. To gauge what that surprise might mean for market pricing, we took a look at recent changes in the unemployment rate against the daily changes in RBA OIS pricing and 3yr yields (chart at left). The last time the unemployment rate rose more than the market expected was the October labour report and on that day (14 November) the market factored in an additional 6bp of easing in to 6 month forward cash and 3yr yields fell by 8bp. Interestingly, this is the almost the exact same changes we saw following the August labour report where the market was also surprised by a 0.1ppt increase in the unemployment rate. So if our forecast prevails, it would likely be supportive of AU bonds.

Another key driver, outside of domestic data, is movement in offshore markets (chart at right). US 10yr yields have been range-bound between 1.70-1.95% over the past three months. The impeachment trial of Trump is set to begin this week, but given the market’s alibility to absorb the escalation of tensions in the Middle East, the signing of the U.S.-China trade deal, ongoing good data in the US and a record-setting run in stocks within this range, it is difficult to foresee any major valuation shift this week. So that should clear the way for some AU outperformance on the back of domestic data outcomes.

The US-China trade deal remains widely seen as a positive for A$. At the very least, it is better for risk appetite than trade war by tweet, and so improving sentiment has helped AUD/USD grind back from 0.6850 to the low 0.69s. But attention will now swing back to the domestic economy, with the Jan consumer sentiment survey a vital update on the public response to the bushfire crisis. This is followed by what will be the unemployment rate the RBA ponders as it reviews policy in Feb. It is interesting to see pricing for the rate cut Westpac expects tick back above 50% (chart at left). Soft data could spark a test of the 100dma at 0.6840.

I think we can pretty much say the same for the ASX bubble. A rise in unemployment will be supportive and vice versa.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.