DXY is up and away as EUR and CNY sink:

The Australian dollar reversed all jobs report gains:

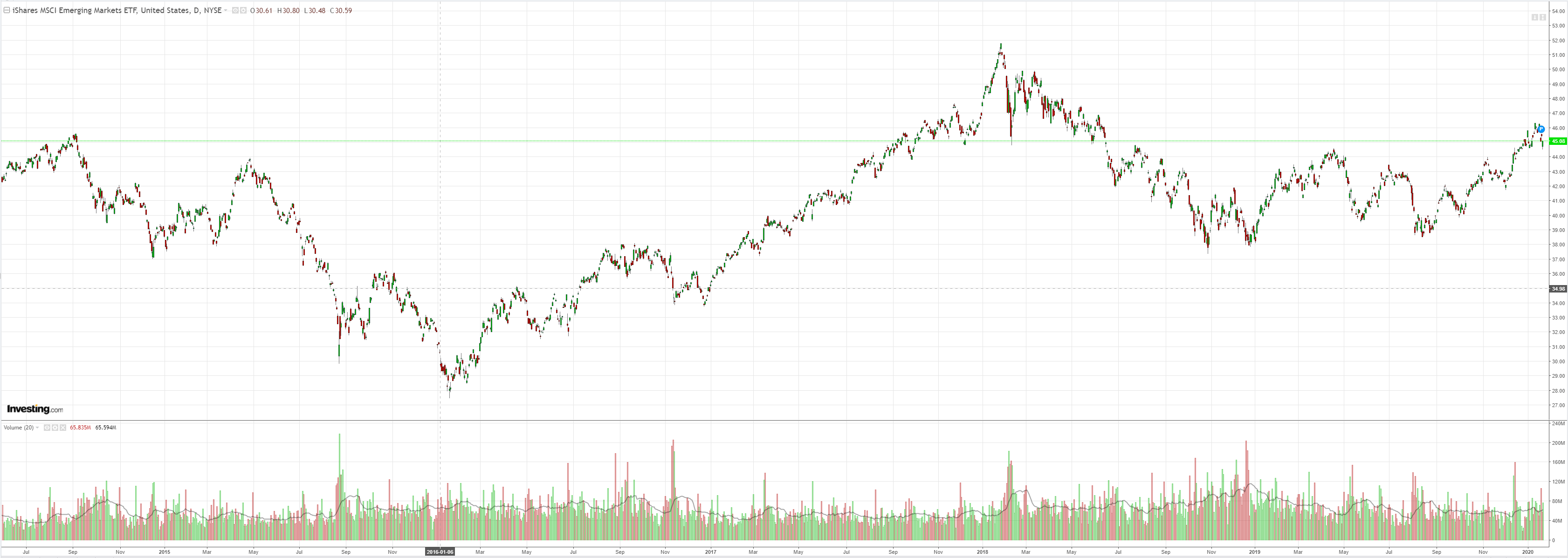

Did a bit better against EMs:

Gold is strangely strong:

Oil is weak as coronavirus demolishes air travel:

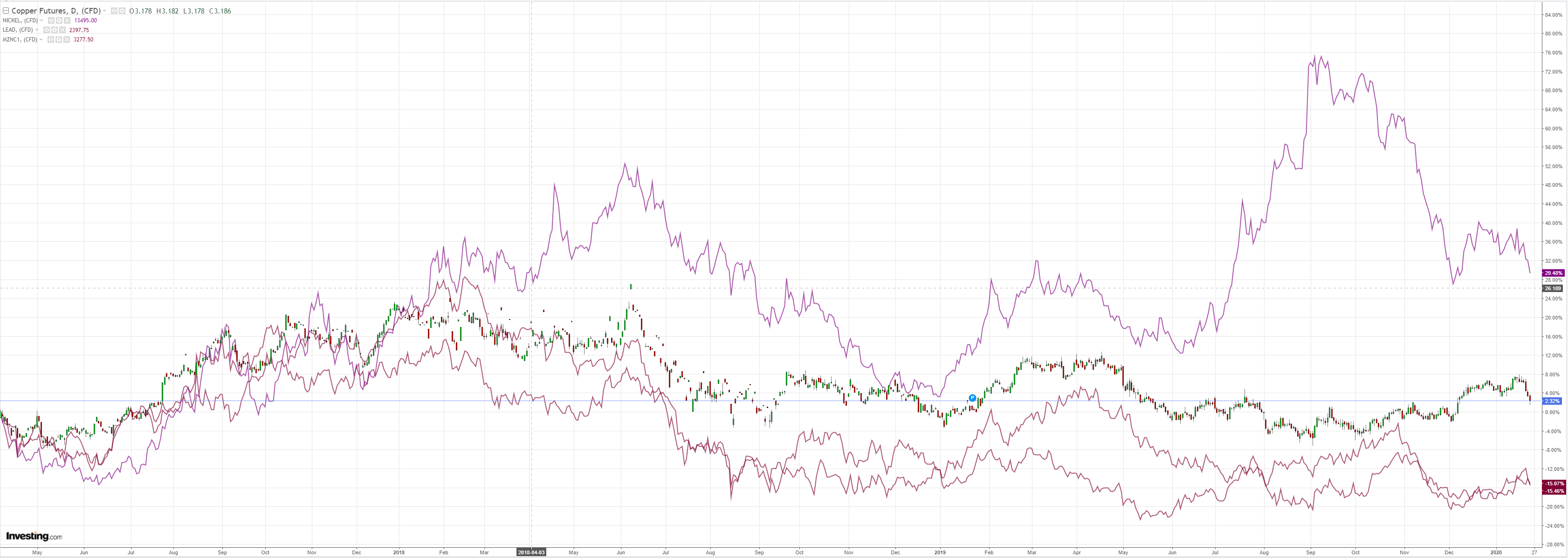

Base metals are catching on now:

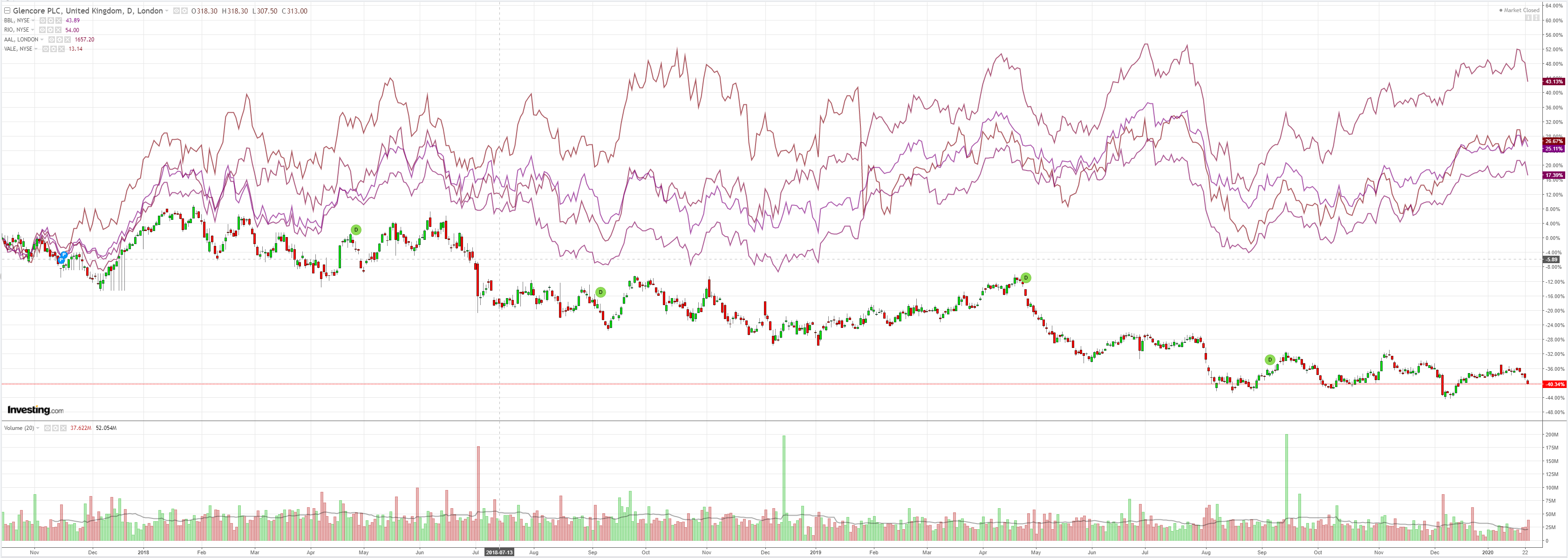

And miners as iron ore also wilted:

EM stocks did OK despite the Shanghai crash:

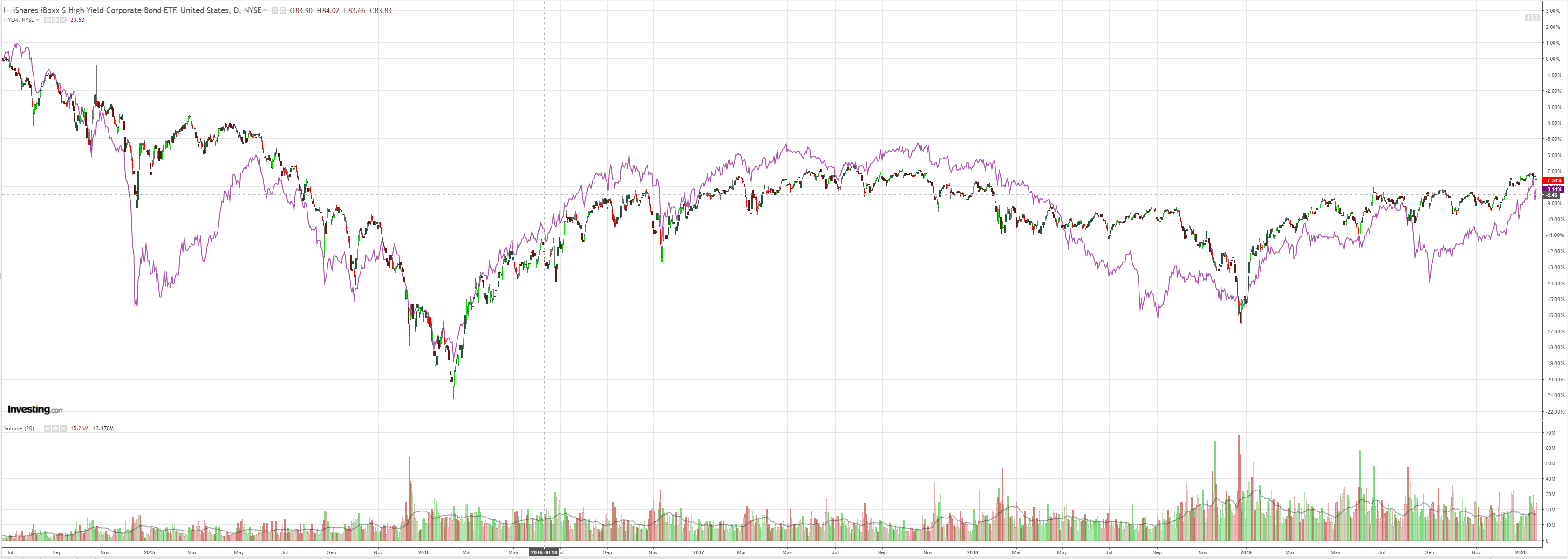

Junk did better too:

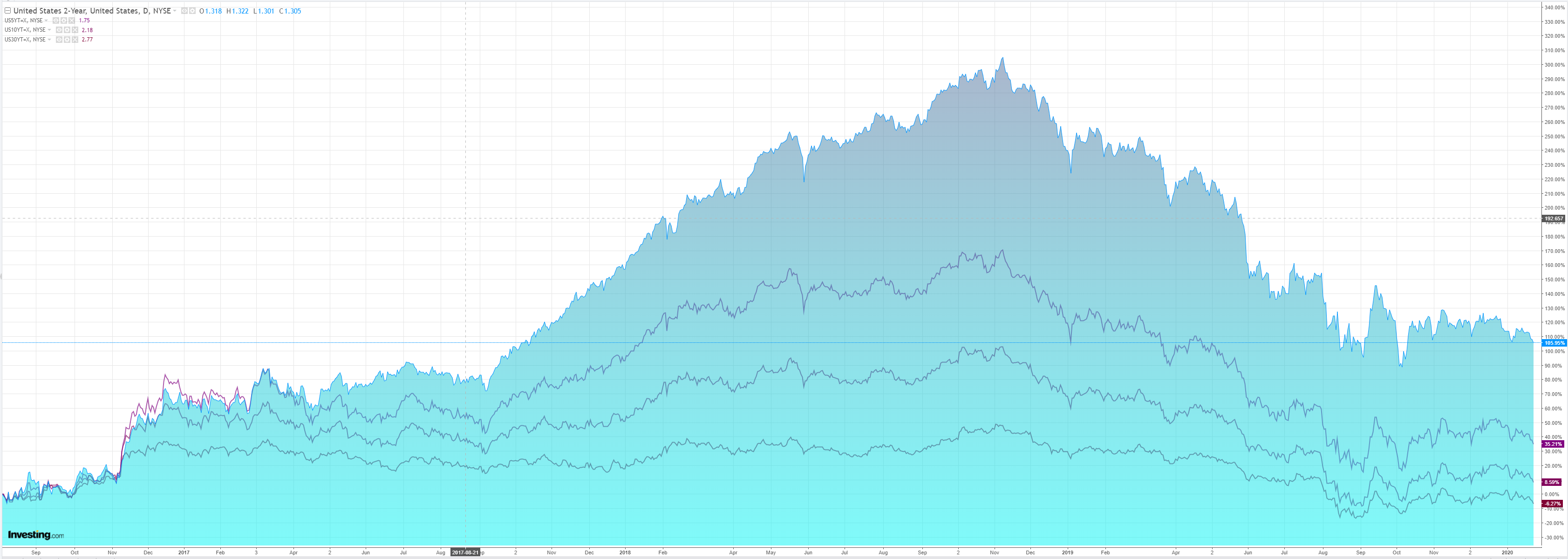

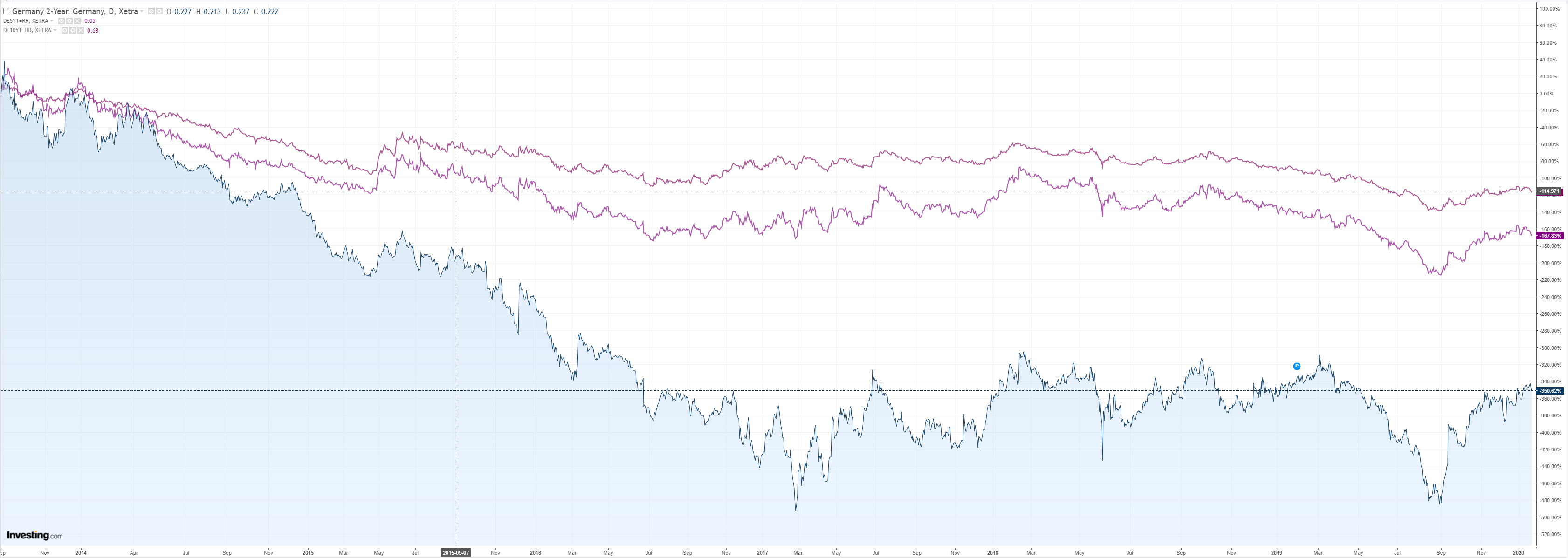

Bonds are bid bigly:

Which aided stocks:

Westpac has the data wrap:

Event Wrap News of spreading and increasing cases of the coronavirus overshadowed markets

ECB left policy unchanged, as widely expected. However, the duration of their extensive review of policy, tools and strategy into late 2020 was cited as a reason for their policy to remain unchanged despite tentative signs of stability and moderate (rather than mild) underlying inflation.

Data releases were light and generally second tier. US jobless claims were again benign and the Jan. Kansas Fed survey showed sound new order and employment components as it edged towards zero (-1, est. -6, prior -8)

The UK Brexit Bill gained royal assent to become law and affirm UK’s exit from EU at the end of January

Event Outlook

The Q4 NZ CPI report will be the focus of today’s Australasian session. A 0.4% rise in prices in Q4 is expected to leave the annual rate at 1.8%yr. Tobacco excise, international airfares and construction costs all look set to support inflation in the quarter. Muted growth in the price of many retail goods will act as a partial offset. Note, Westpac and the market’s forecast of 0.4% is above that of the RBNZ, 0.2%.

Japan’s December CPI is also set for release. Inflation pressures remain absent there, with annual headline inflation expected to print at just 0.7%yr in December.

Also out today are January PMIs for Japan, the UK, Euro Area and US.

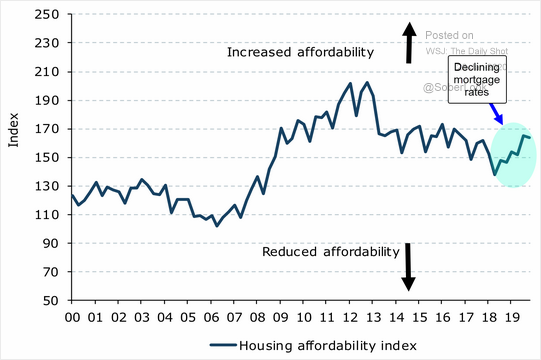

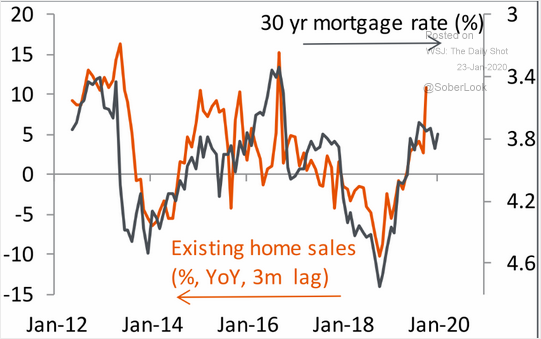

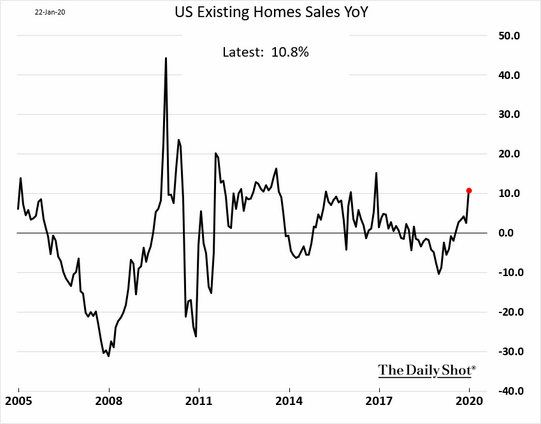

Some more on the US housing market today. It is booming and the coronavirus impact on interest rates is setting us up for more:

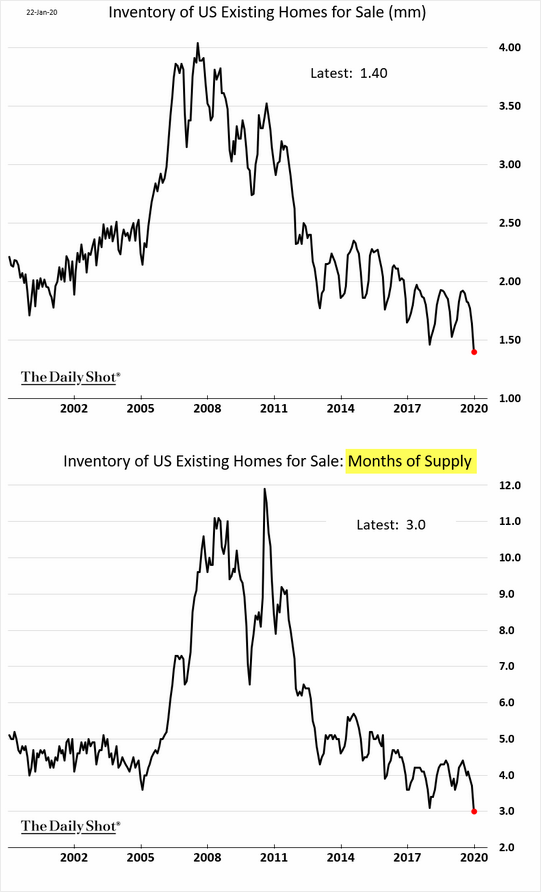

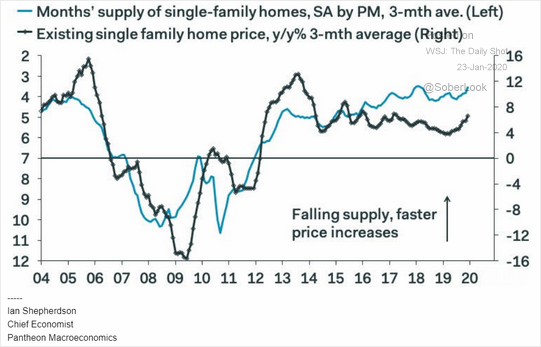

Inventories are very now, pushing price gains as well:

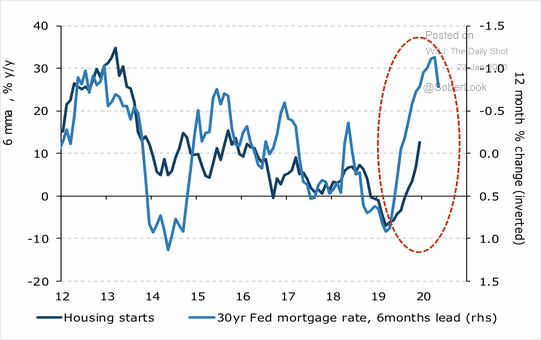

And building!

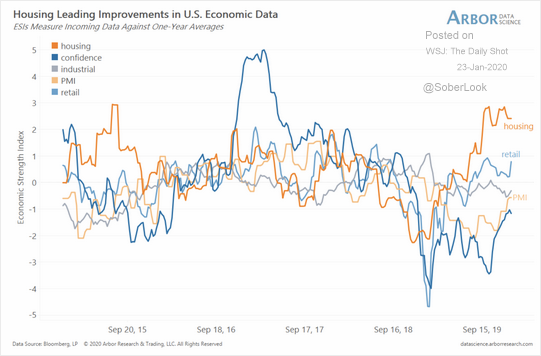

Leading the economy:

There is nothing like this in any other developed market. The US is revving for another mini-cycle. Then there is this:

Treasury Secretary Steven Mnuchin said Thursday that the White House is already crafting a package of tax cuts for the middle class as President Donald Trump hopes to secure a second term in November.

In an interview with CNBC from the World Economic Forum in Davos, Switzerland, Mnuchin said Trump has already directed his economic team to begin on what the administration is calling “Tax 2.0.”

“They’ll be tax cuts for the middle class, and we’ll also be looking at other incentives to stimulate economic growth,” Mnuchin said.

Trump has repeatedly dangled additional tax cuts, including before the 2018 midterms. Mnuchin’s renewed promise of tax cuts for average Americans comes more than two years after the President signed into a law a massive $1.7 trillion tax package that slashed corporate tax rates, among other things.

China is going to get smashed over the next six months fighting coronavirus. Tarrifs are still in place too. Europe can’t recover as China sags.

Markets are positioned for more Fed action and global growth convergence. Instead, the US economy is going to stretch its growth and inflation leadership over the rest of the world in 2020.

Irrespective of QE4, the US dollar is poised for a major bid.

Australian dollar look out.