The Australian dollar was hopsitalised across the board:

Gold hung on:

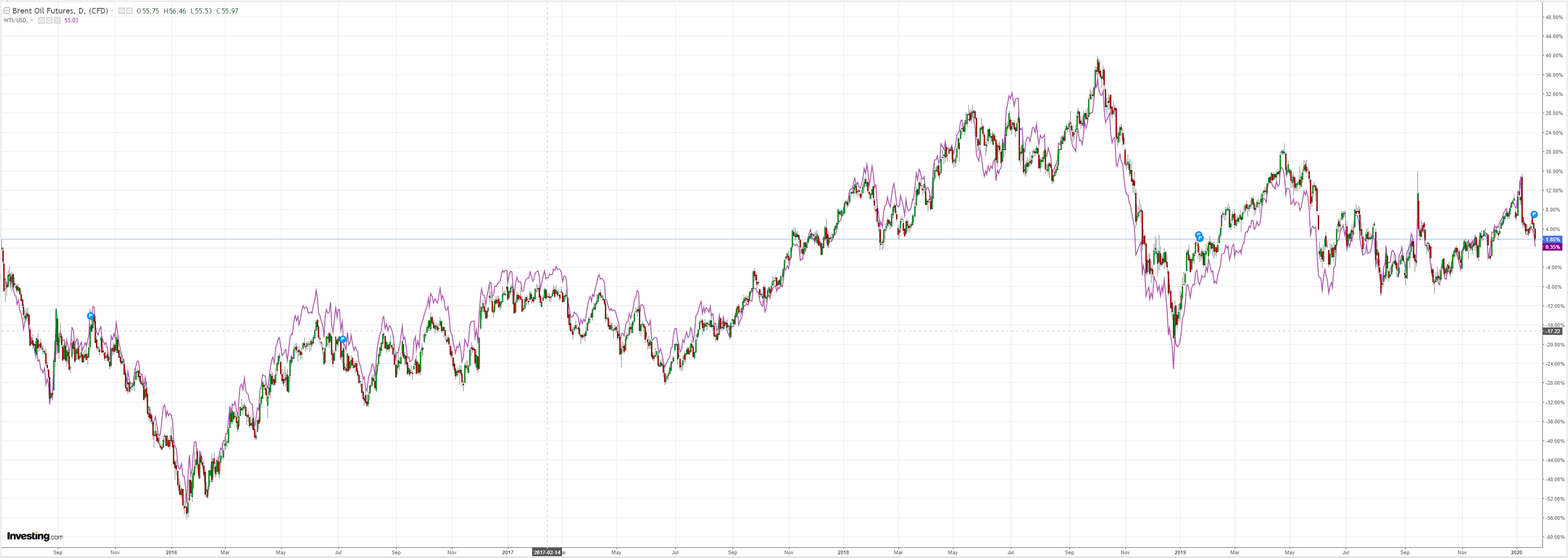

Oil gave in:

Advertisement

As did metals:

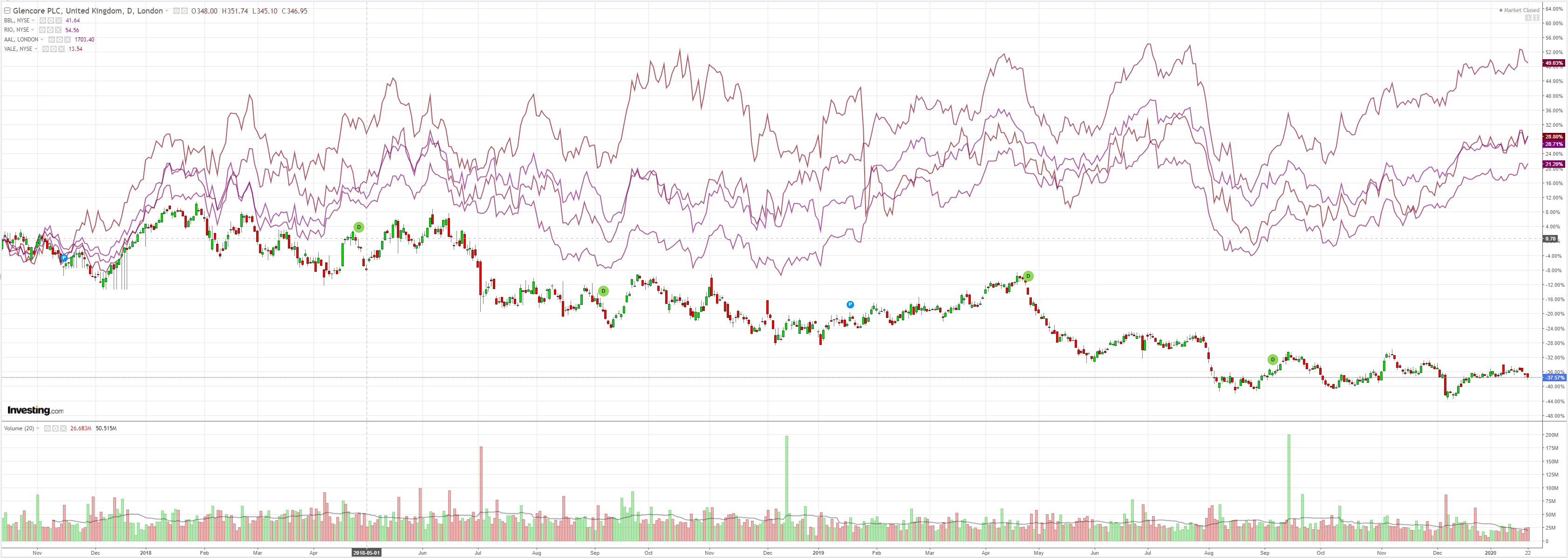

Miners only care about iron ore:

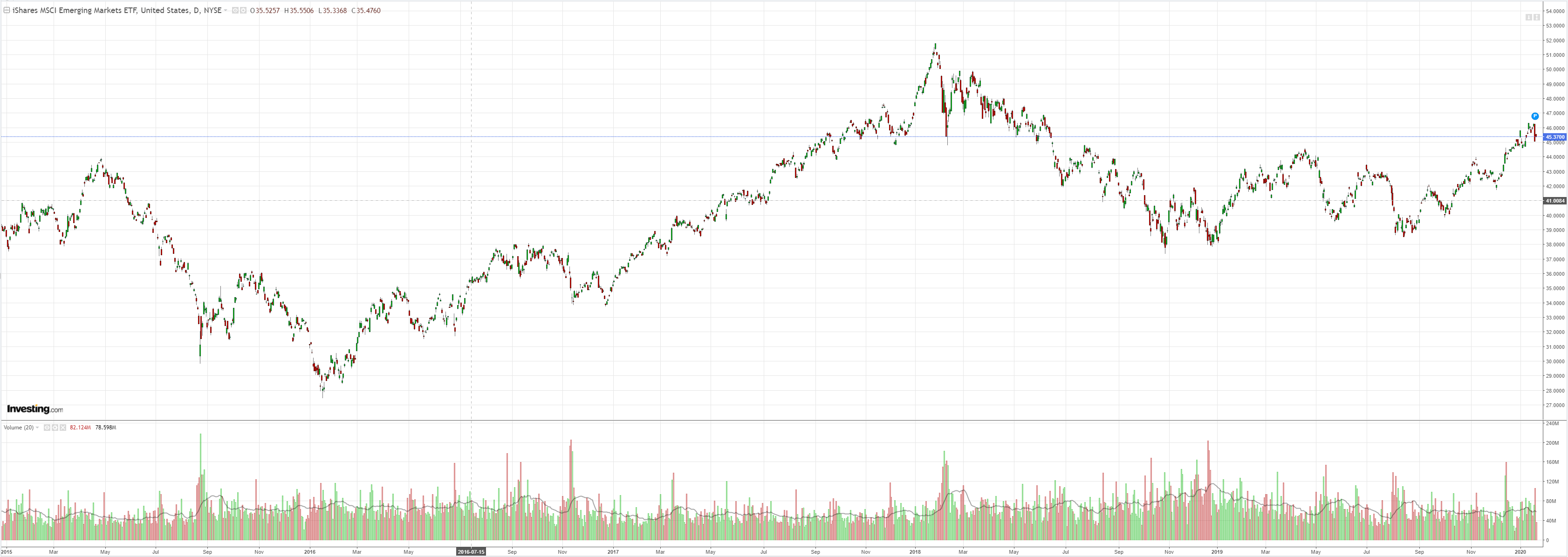

EM stocks bounced:

Advertisement

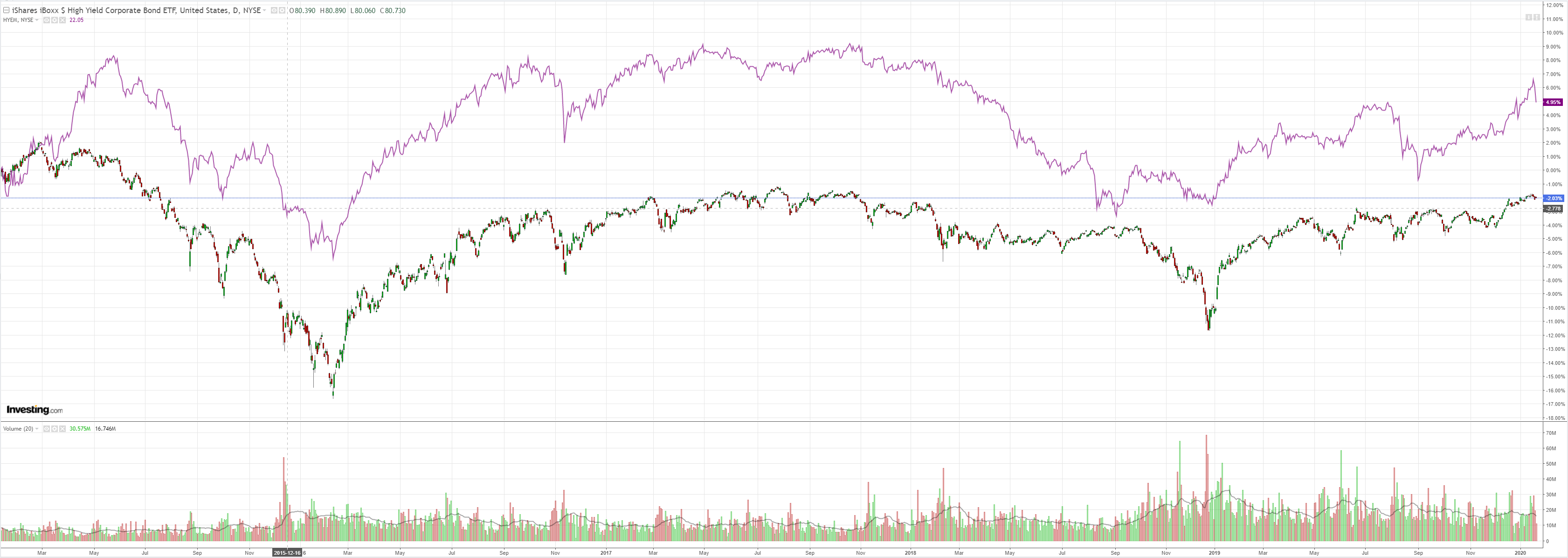

But junk is signalling possible trouble:

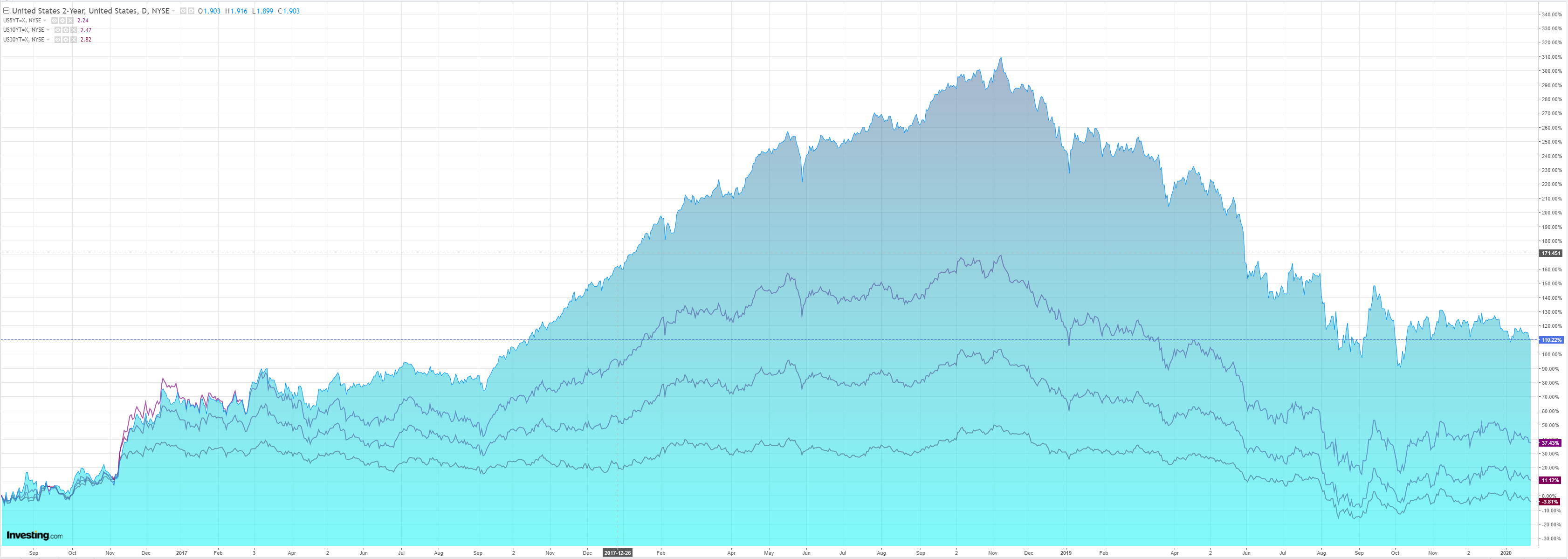

Treasuries were bid:

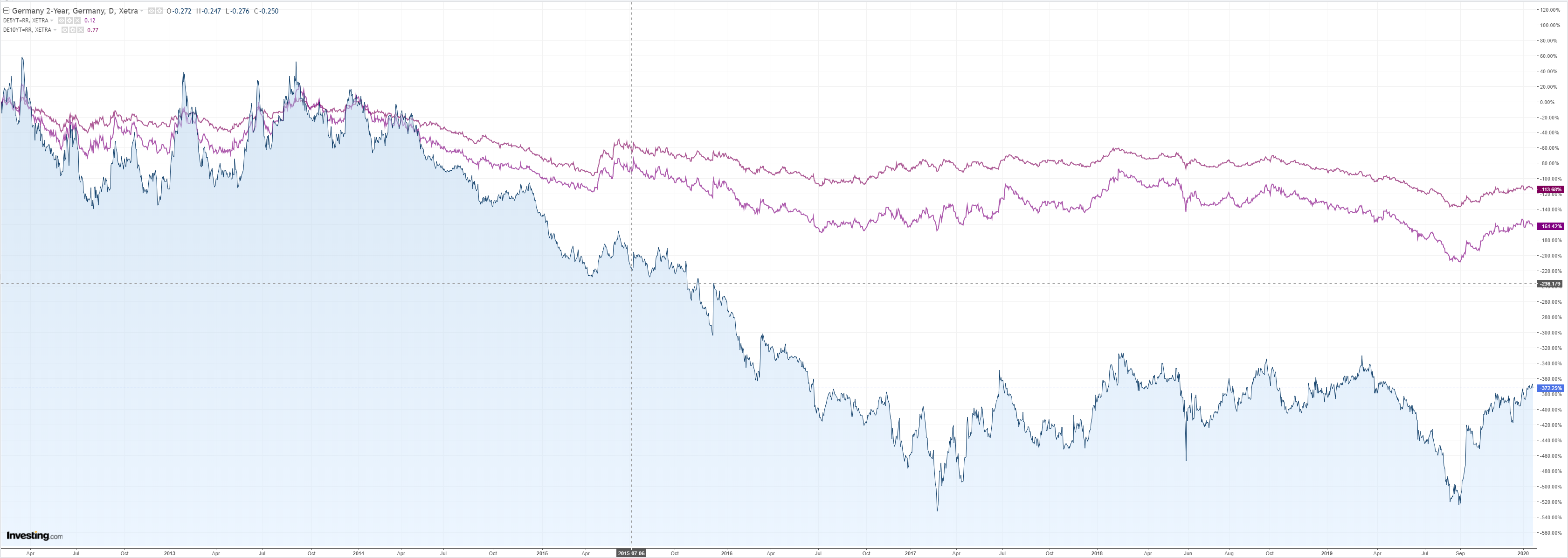

Bunds too:

Advertisement

Aussie most:

Stocks to the moon again:

Westpac has the data wrap:

Advertisement

Event Wrap UK’s firm CBI business survey and the softer BoC stance were the dominant events.

UK CBI Jan. business optimism surged to +23 (est. -20, prior -40) in the first clear sign that post-election sentiment is improving and cited rising investment intentions though they may be contained due to constraints in the labour market.

BoC left rates unchanged (as expected) but adopted a more dovish, data watching stance. Governor Poloz stated that the “door is open to a rate cut if needed” and cited the mixed data performance into end 2019.

Canada’s Dec. headline CPI of 2.2%y/y missed expectations (2.3%y/y) and the core components were on average -0.1% below expected levels.

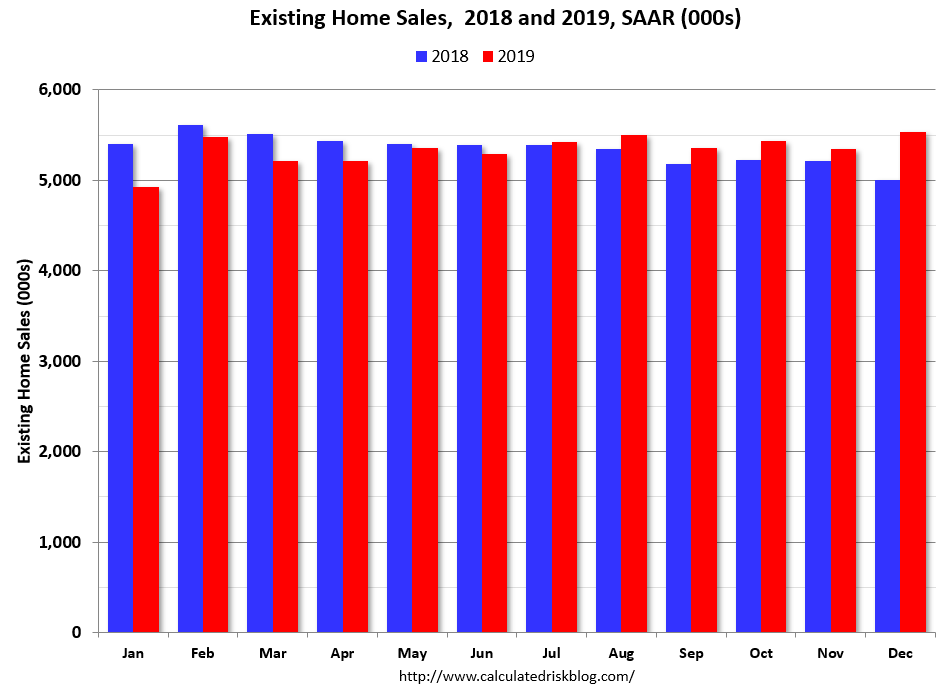

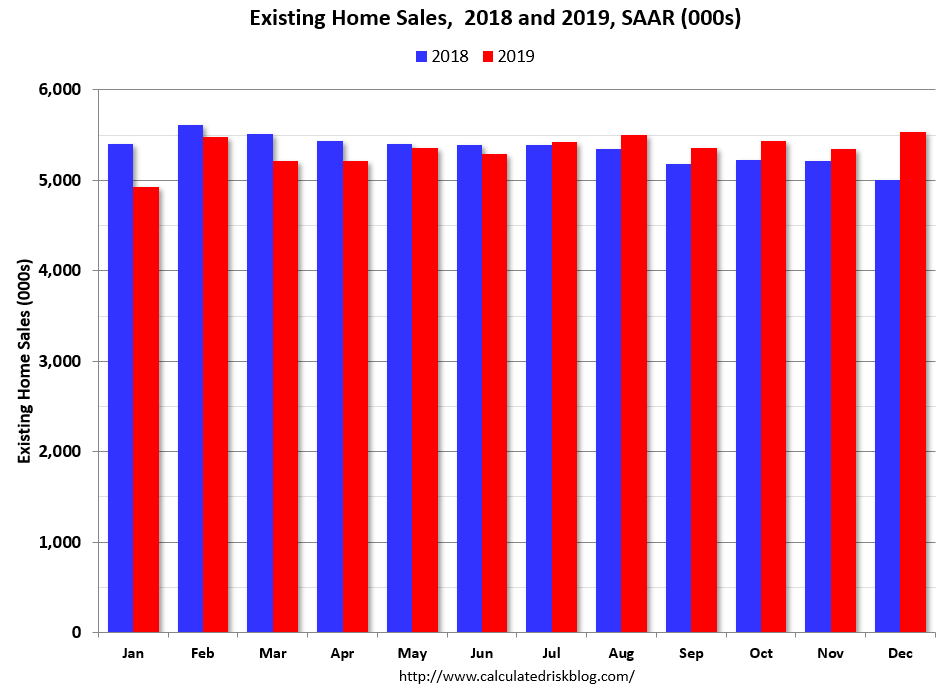

US Dec. Existing home sales rose +3.6% (est. +1.5%) to an annualised level of 5.54mn and the supply ratio to sales fell to a record low of 3 months.

Offsetting some of the housing strength was a miss in the Dec. Chicago Fed Index which slipped to -0.35 (est. +0.13, prior +0.41) but remained close to its average for a volatile 2019.

Event Outlook

The December labour force survey for Australia is expected to see the trend deceleration in employment growth apparent since May persist. Following November’s outsized 37k gain, we look for a 5k decline in December (mkt +12k). Holding participation flat, the unemployment rate is likely to lift to 5.3%.

The ECB’s January policy meeting is today’s other major event. The December meeting minutes were more sanguine on the outlook, showing a belief that downside risks had diminished. Given market sentiment, this view will be reaffirmed in January. Nonetheless, expect support for the current asset purchase program to remain in place and a clear willingness to act further, should conditions warrant it, to be shown.

Existing-home sales grew in December, bouncing back after a slight fall in November, according to the National Association of Realtors®. Although the Midwest saw sales decline, the other three major U.S. regions reported meaningful growth last month.

Total existing-home sales, completed transactions that include single-family homes, townhomes, condominiums and co-ops, increased 3.6% from November to a seasonally-adjusted annual rate of 5.54 million in December. Additionally, overall sales took a significant bounce, up 10.8% from a year ago (5.00 million in December 2019).

…Total housing inventory at the end of December totaled 1.40 million units, down 14.6% from November and 8.5% from one year ago (1.53 million). Unsold inventory sits at a 3.0-month supply at the current sales pace, down from the 3.7-month figure recorded in both November and December 2018. Unsold inventory totals have dropped for seven consecutive months from year-ago levels, taking a toll on home sales.

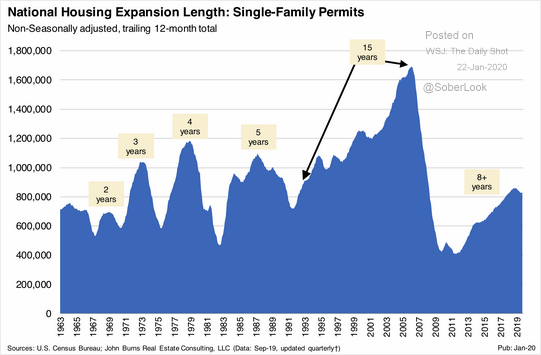

Aided by nice weather but there is no end in sight:

Advertisement

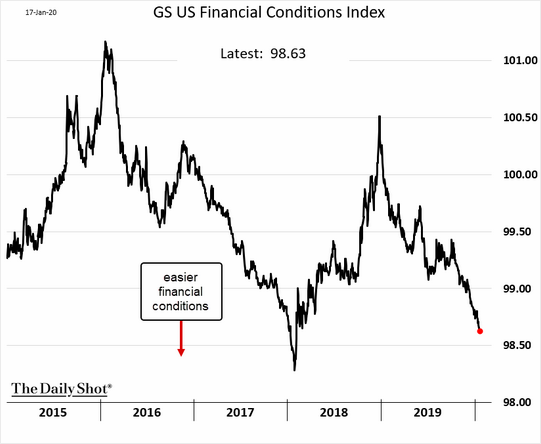

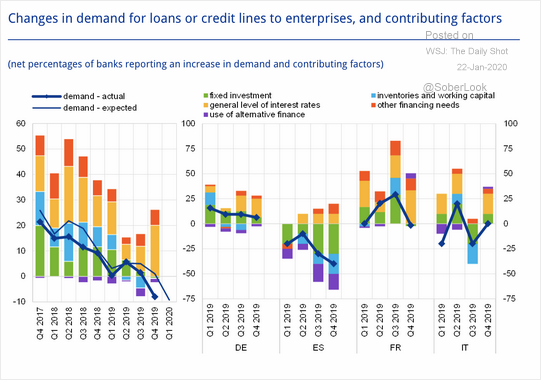

As financial conditions ease:

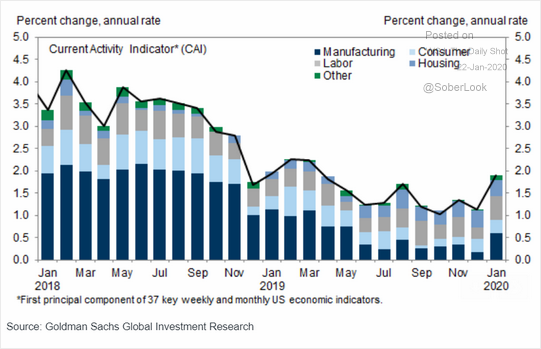

It is now lifting broader activity:

Advertisement

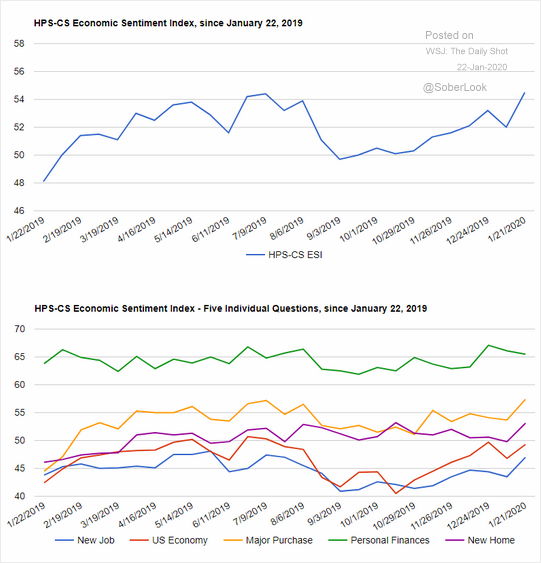

Via the consumer:

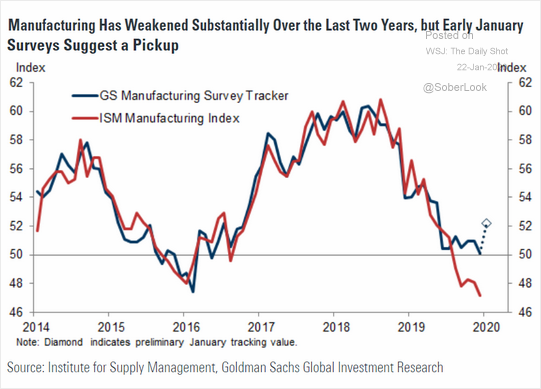

And manufacturing is next:

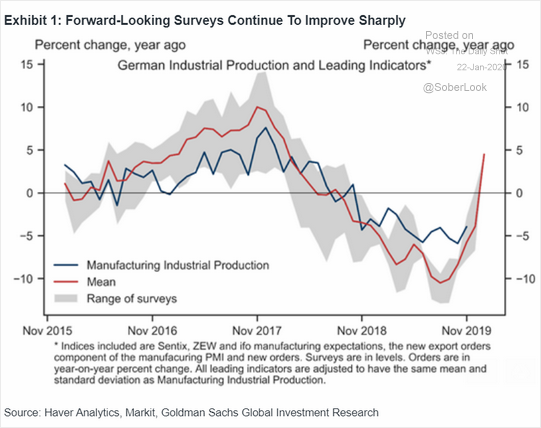

There is some hope of spillovers to the rest of the world even if less than previous cycles:

Advertisement

But Europe is still weak:

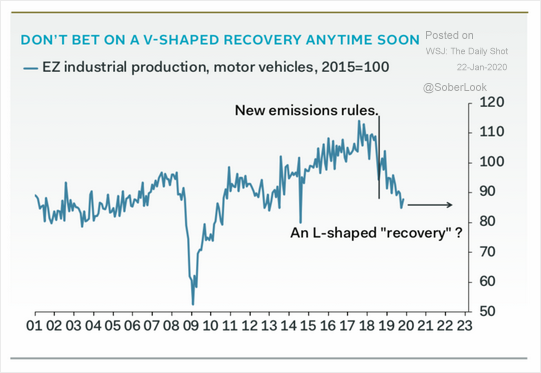

And cars are a key problem:

Advertisement

I still can’t Europe catching up to the US enough to roll DXY. China is now under mounting pressure form the virus crisis as well (more in a separate post).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

{kind=link}