That leaves the Australian dollar nowhere to go but down:

Advertisement

Gold fell:

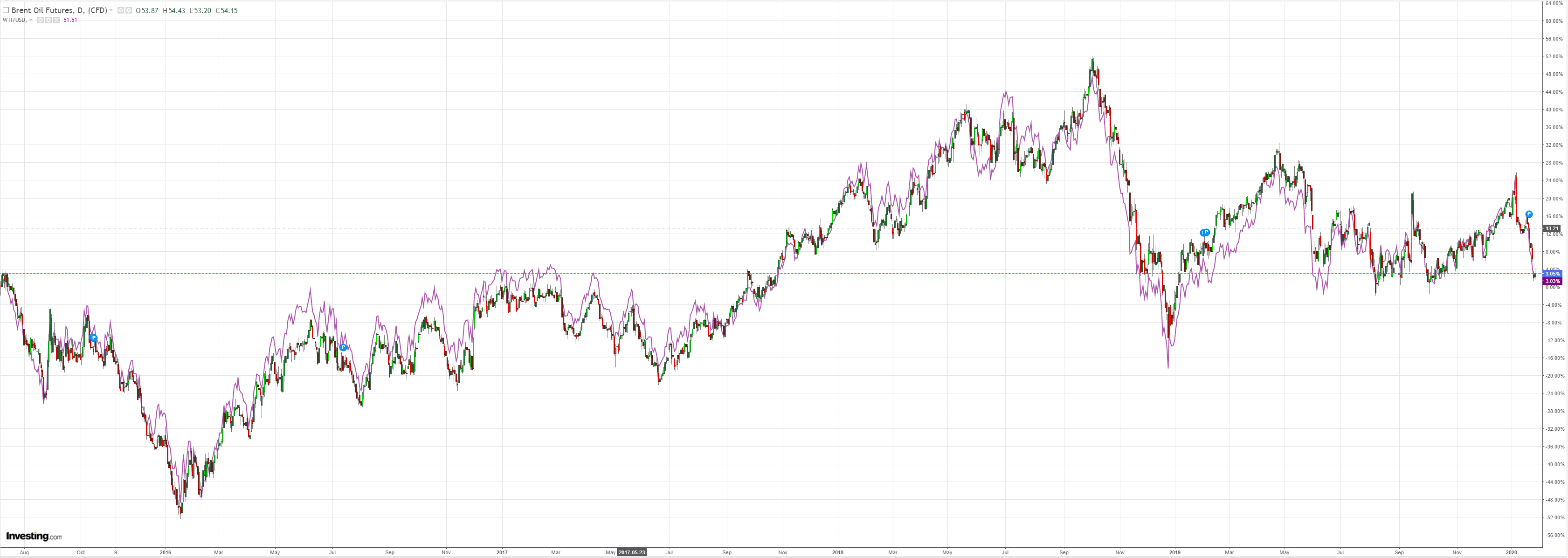

Oil rose a bit:

Metals fell further:

Advertisement

Miners bounced:

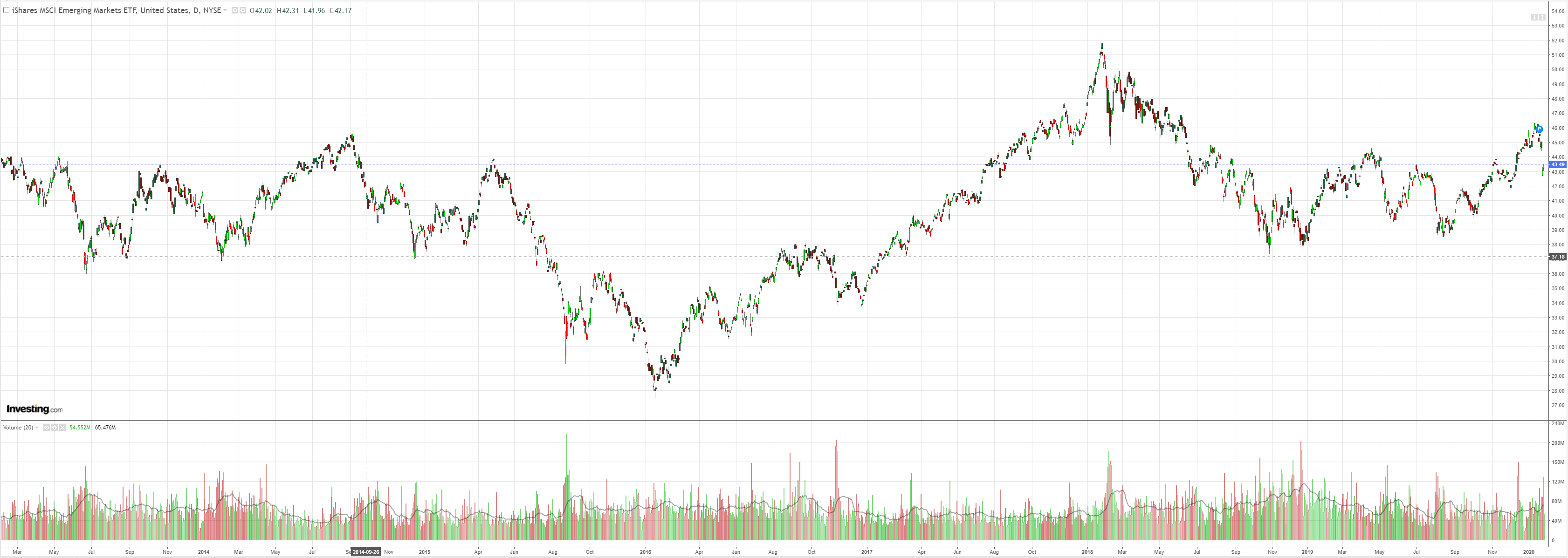

And EM stocks:

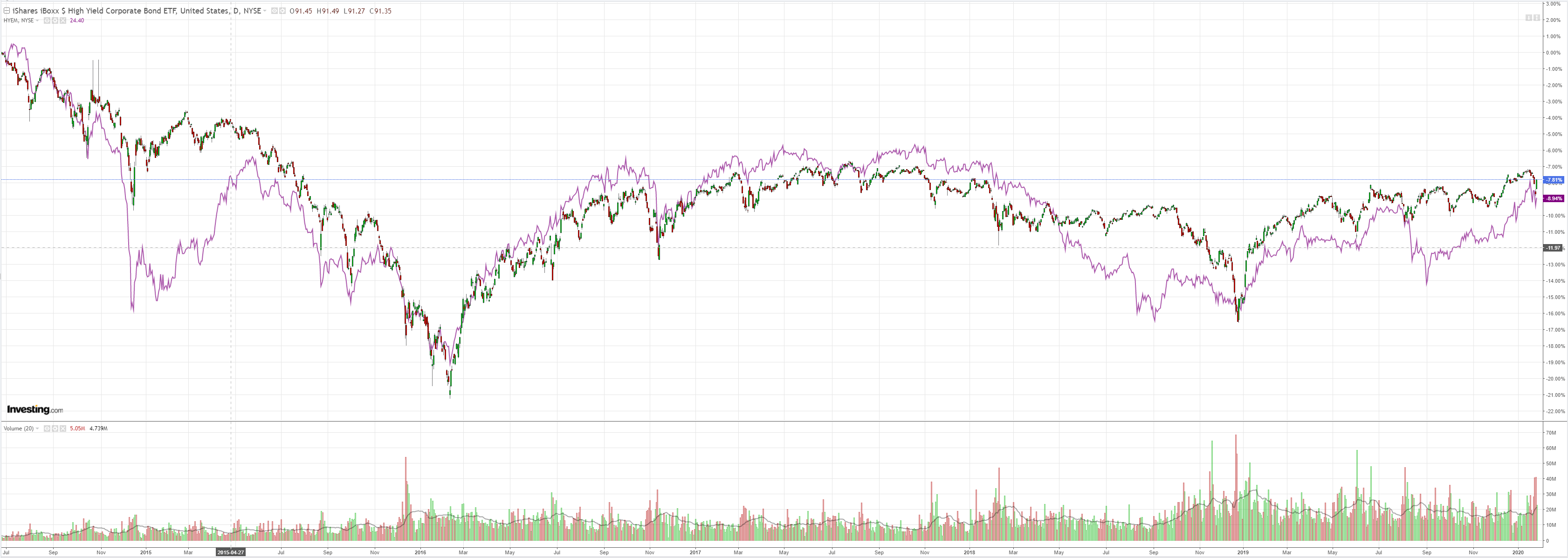

Plus junk:

Advertisement

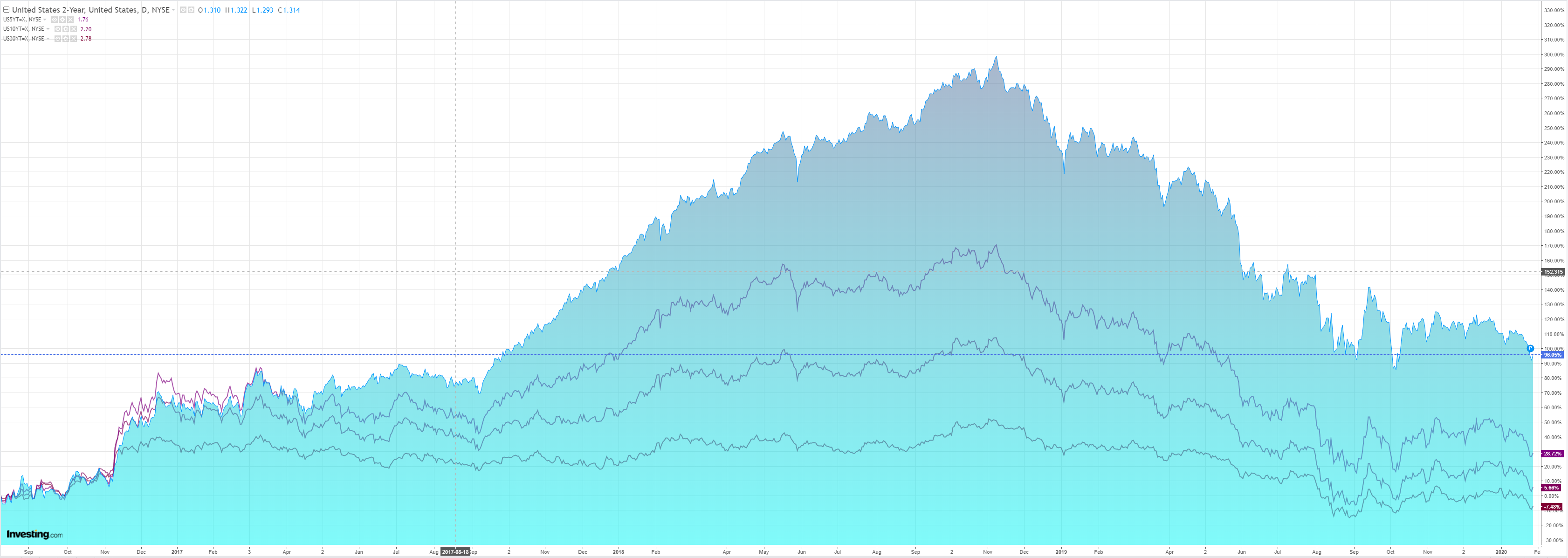

Treasuries eased:

All bonds did:

As stocks declared the virus crisis dead:

Advertisement

Good luck with that. This increased volalility is not reassuring to my mind. It is more typical of a bear not bull market. Westpac has the data wrap:

Event Wrap

US durable goods orders rose 2.4% in Dec (vs 0.3% expected), although the details in the report were less impressive (core measures weaker than expectations). House prices (CoreLogic) in the 20 major cities rose 0.5% in Nov, for a 2.6% annual pace (vs 2.4% expected). Conference Board consumer confidence made a five-month high at 131.6 (vs 128.0 expected). Richmond Fed’s manufacturing survey surged to the highest level since 2018, the strength broad-based and pointing to a solid ISM survey result.

Event Outlook

NZ: RBNZ Assistant Governor Hawkesby speaks in Sydney about how it analyses the global economy.

Australia’s Q4 CPI report is again expected to show a weak underlying inflation trend, the trimmed mean core CPI to print at 0.4%, 1.5%yr. Auto fuel and tobacco will boost headline inflation in the quarter (WBC and market are at 0.6%), but annual headline inflation will remain below the RBA’s 2-3%yr target range, circa 1.8%yr.

Also for Australia, the Westpac-MI Leading Index has now been pointing to below-trend growth for a year. Come December, another weak reading is expected as the components of the index have seen mixed moves over the month.

In the US session, all eyes will be on the FOMC’s communications following their January meeting. On trade and global growth, there is arguably reason for greater optimism than in December following the signing of the stage 1 US/China deal. However, on the domestic front, the past month has provided evidence of a softening US consumer, in line with our view. It is arguably too early to assess the economic implications of the Novel coronavirus 2019 outbreak, though it is likely to be discussed as a risk in the press conference. We continue to look for three cuts from the FOMC in 2020, starting in June.

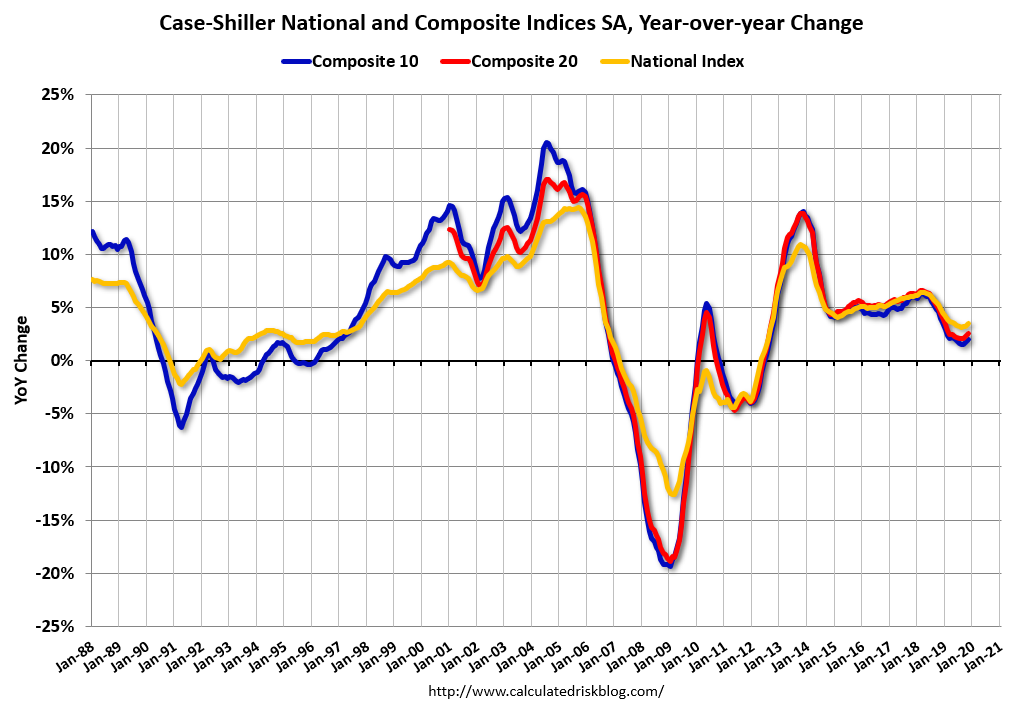

The powerful US housing bounce continues, now in prices:

Advertisement

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.5% annual gain in November, up from 3.2% in the previous month. The 10-City Composite annual increase came in at 2.0%, up from 1.7% in the previous month. The 20-City Composite posted a 2.6% year-over-year gain, up from 2.2% in the previous month.

Phoenix, Charlotte and Tampa reported the highest year-over-year gains among the 20 cities. In November, Phoenix led the way with a 5.9% year-over-year price increase, followed by Charlotte with a 5.2% increase and Tampa with a 5.0% increase. Fifteen of the 20 cities reported greater price increases in the year ending November 2019 versus the year ending October 2019.

…The National Index posted a month-over-month increase of 0.2%, while the 10-City and 20-City Composites both posted a month-over-month increase of 0.1% before seasonal adjustment in November. After seasonal adjustment, the National Index, 10-City and 20-City Composites all posted a 0.5% increase. In November, 13 of 20 cities reported increases before seasonal adjustment while all 20 cities reported increases after seasonal adjustment.

“The U.S. housing market was stable in November,” says Craig J. Lazzara, Managing Director and Global Head of Index Investment Strategy at S&P Dow Jones Indices. “With the month’s 3.5% increase in the national composite index, home prices are currently 59% above the trough reached in February 2012, and 15% above their pre-financial crisis peak. November’s results were broad-based, with gains in every city in our 20-city composite.

“At a regional level, Phoenix retains the top spot for the sixth consecutive month, with a gain of 5.9% for November. Charlotte and Tampa rose by 5.2% and 5.0% respectively, leading the Southeast region. The Southeast has led all regions since January 2019.”

“As was the case last month, after a long period of decelerating price increases, the National, 10-city, and 20-city Composites all rose at a modestly faster rate in November than they had done in October. This increase was broad-based, reflecting data in 15 of 20 cities. It is, of course, still too soon to say whether this marks an end to the deceleration or is merely a pause in the longer-term trend.”

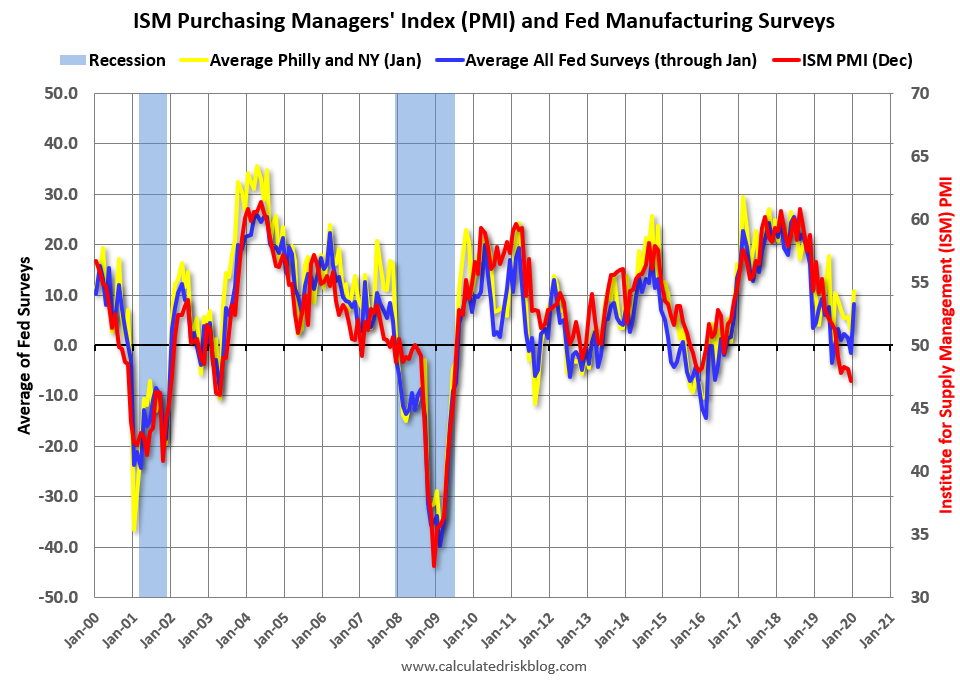

It is feeding through to manufacturing now as well:

Fifth District manufacturing activity rebounded in January, according to the most recent survey from the Richmond Fed. The composite index rose from −5 in December to 20 in January, as all three components— shipments, new orders, and employment— increased. Local business conditions also improved as this index saw its largest increase since February 2013. Manufacturers were optimistic that conditions would continue to strengthen in the coming months

Survey results indicate that both employment and wages rose for survey participants in January. However, firms continued to struggle to find workers with the necessary skills. They expected this difficulty to persist but wages and employment to continue to grow in the next six months.

Without a doubt, the US is the palce to ride coronavirus out. It is the least exposed to the Chinese economy and has a rock solid base of activity in its housing market supporting deleveraged consumers, plus a fiscal pulse.

Advertisement

Meanwhile, Europe and especially Australia are over-exposed to China. The latter has horribly over-streteched consumers as well, and is line for a deteriorating income shock all year, made consierably worse by the virus. While the former will keep DXY strong.

The Australian dollar is now the global coronavirus whipping boy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.