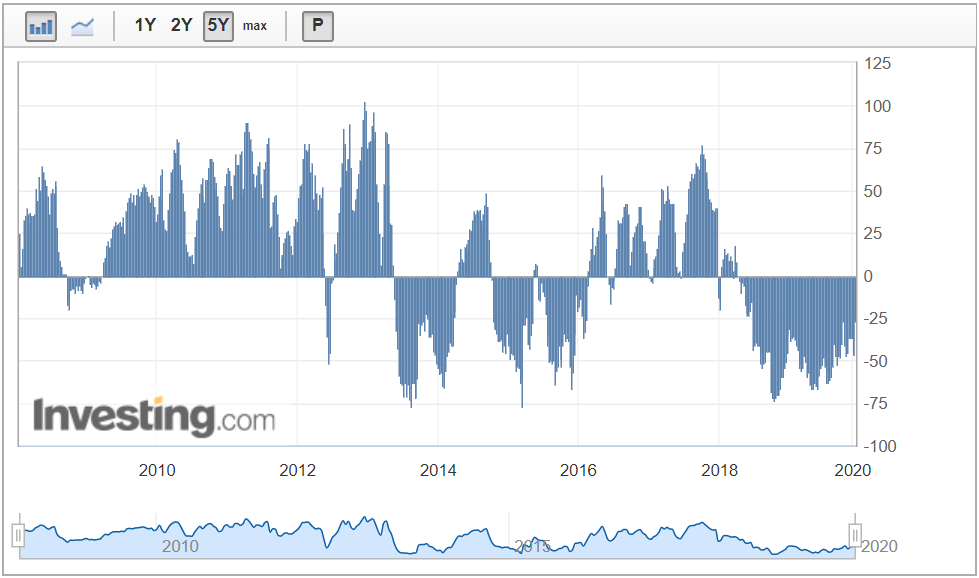

CFTC positioning is back to its lowest net short since in over a year at -27k contracts:

Advertisement

Gold faded:

Oil held on:

Advertisement

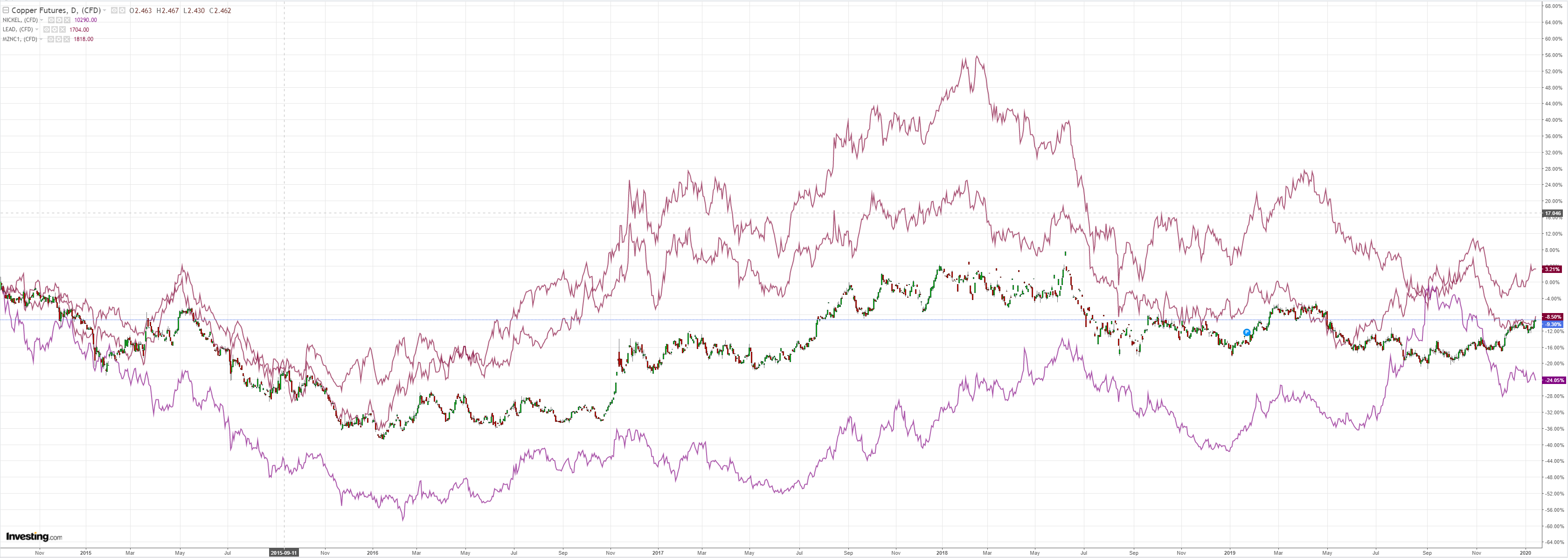

Metals were mixed:

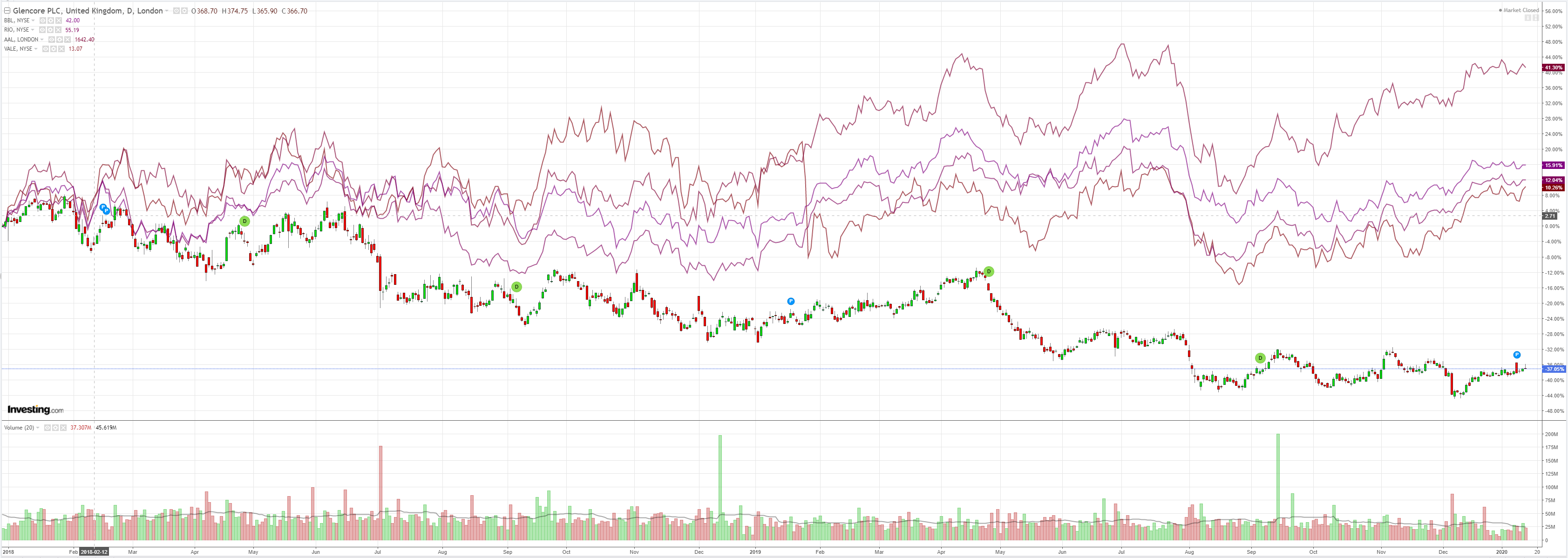

Miners soft:

EM stocks have been partying:

Advertisement

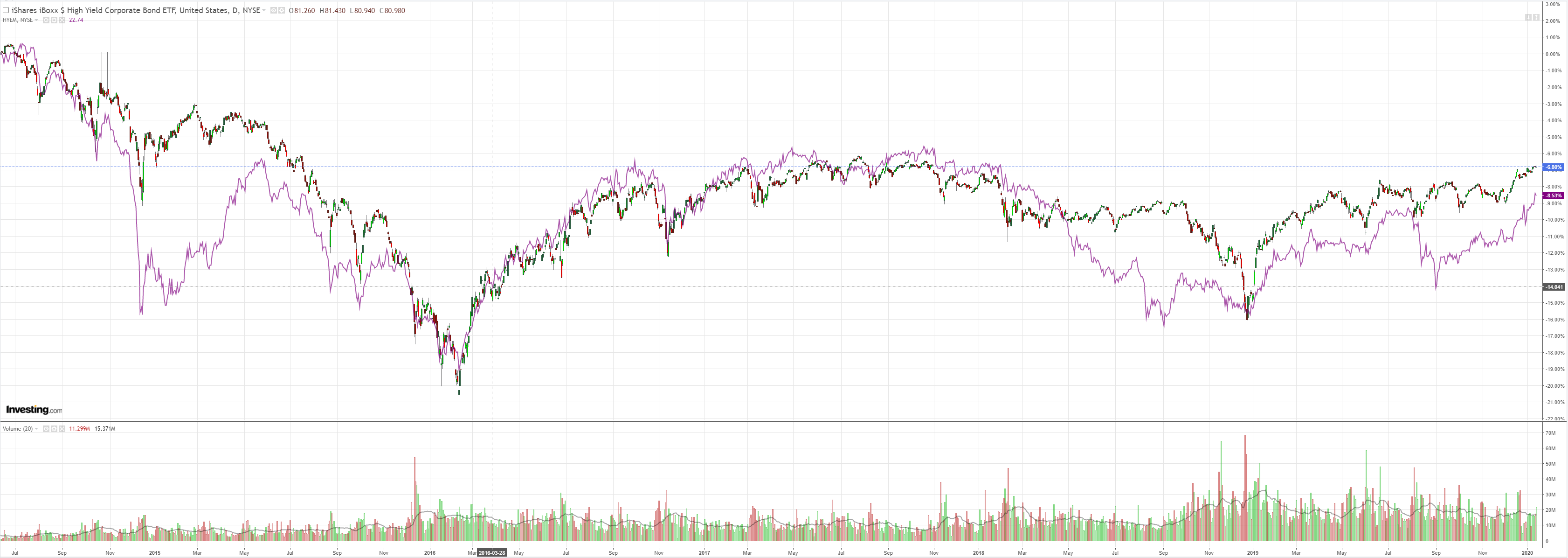

And junk:

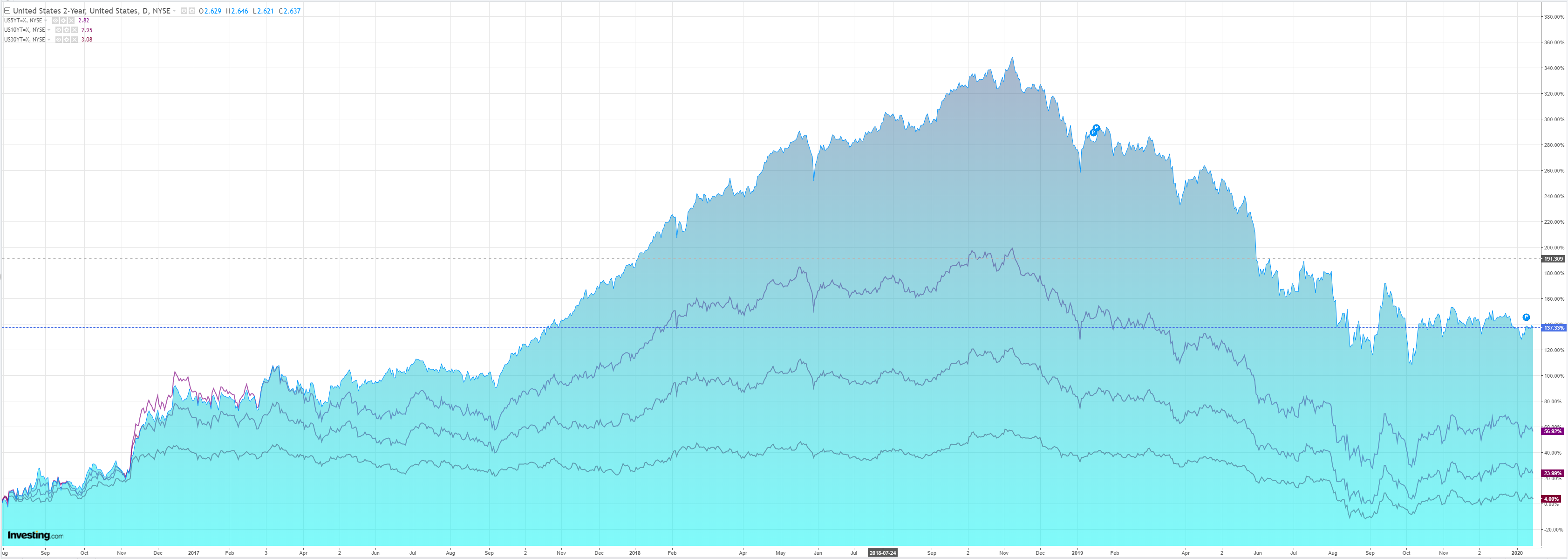

But US yields have turned down:

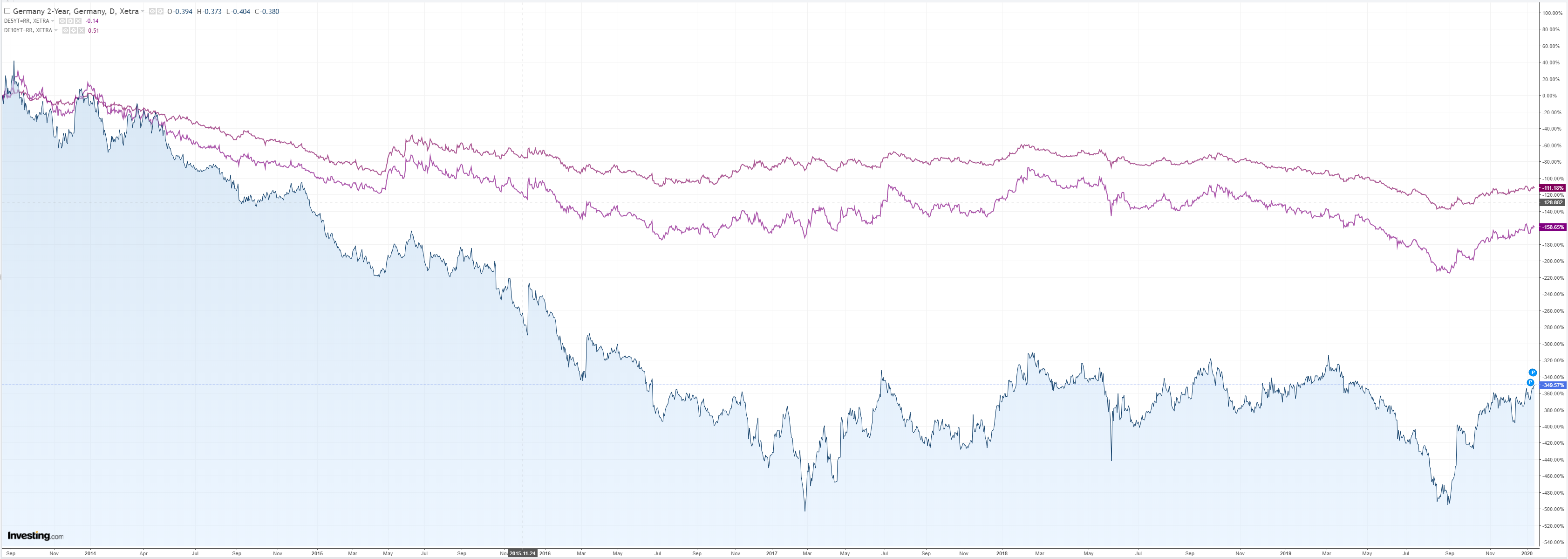

Even as European keep rallying:

Advertisement

Aussie bonds have split the difference:

As stocks enter Nirvana:

Westpac has the wrap:

Advertisement

Event Wrap

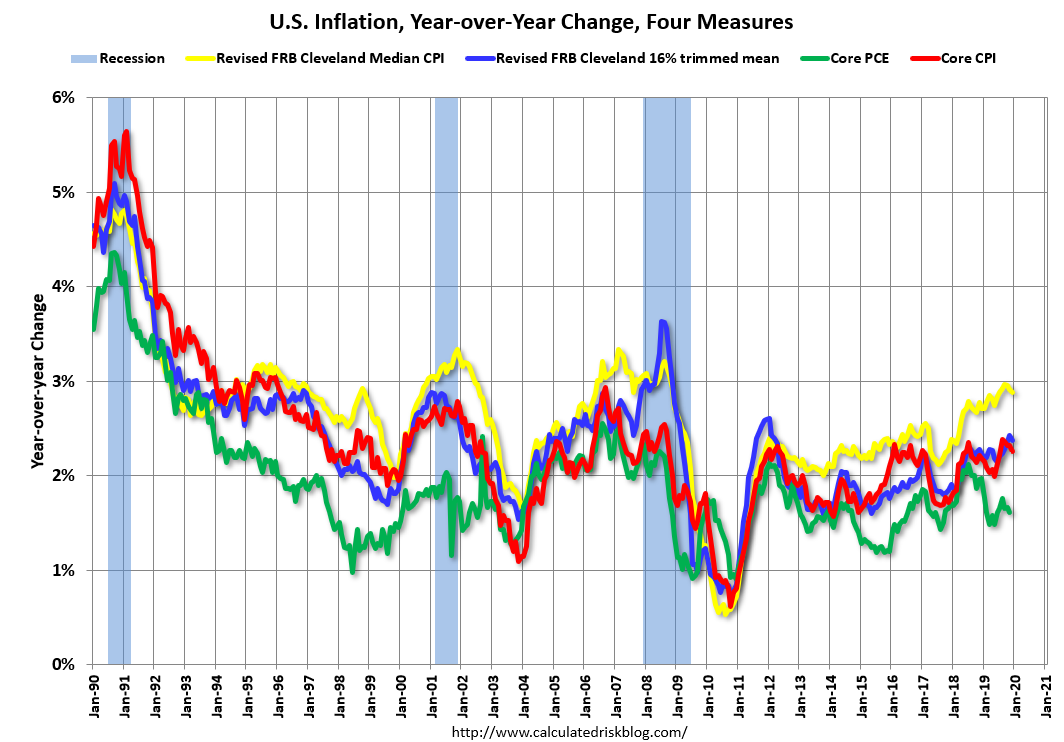

The key data release was US Dec. CPI with both headline and core at +2.3%y/y (estimates were +2.4%y/y headline and core +2.3%y/y). Core CPI gained only +0.1%m/m and its annual level to 3-decimals was +2.259% and so highlighted the benign profile.

US NFIB Dec. survey of small business optimism missed at 102.7 (estimated to be effectively unchanged at 104.6), but remained well within its solid range of the past three years. Although greater uncertainty pulled down the headline, both of the key employment and remuneration components lifted and underscore the underlying stability of the sector.

Event Outlook

NZ Dec. Food prices: Westpac expect an unchanged (m/m) level after Nov. -0.7%m/m (annual inflation has picked up).

NZ REINZ Dec house sales may be released (prior -1.9%y/y)

The initial round of European national (final) CPI releases will be dominated by French and Spain (est. 1.4%y/y and +0.8%y/y respectively) and notably UK CPI (est. headline +1.5%y/y, core +1.7%y/y).

Eurozone Nov. industrial production is expected to rebound +0.4%m/m after slipping -0.5%m/m in Oct.

US Dec PPI is estimated to lift to +1.3%y/y (prior +1.1%y/y). In addition NY Fed’s Jan. Empire survey (est. 3.6) and the broader Fed’s Beige Book (expected to continue to point to a moderate expansion) are released.

Bank of England MPC member Saunders (voted for a cut in Dec.) is due to speak.

Fed’s Kaplan and Harker are scheduled to speak as are ECB’s Holzman and Villeroy.

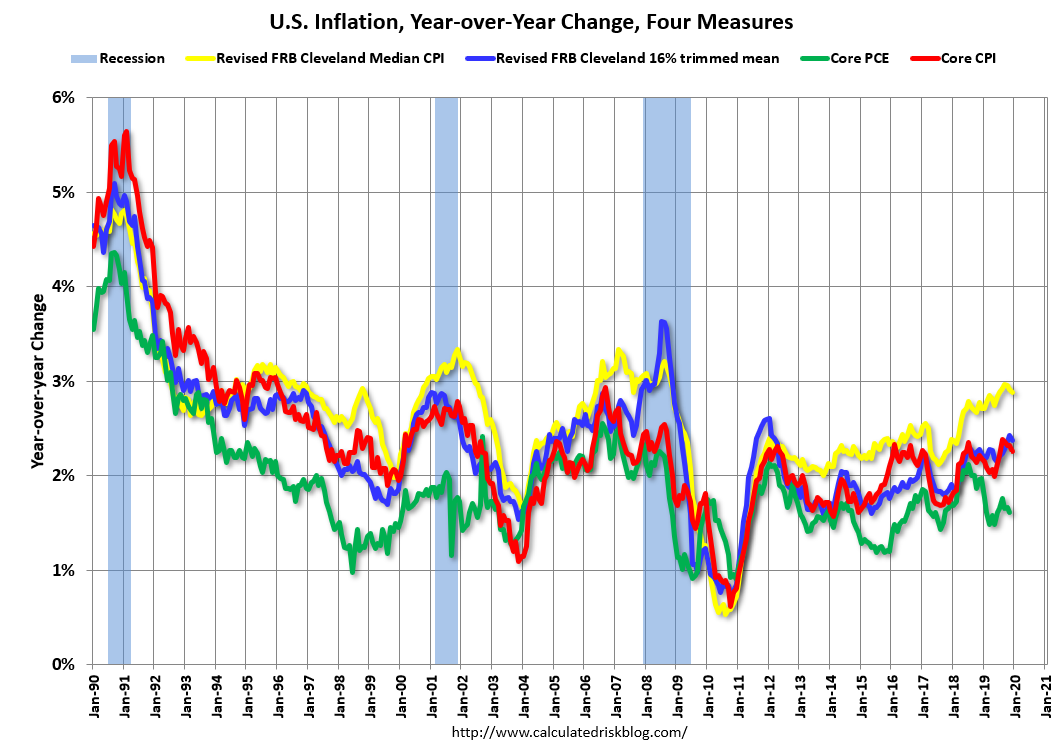

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% (2.1% annualized rate) in December. The 16% trimmed-mean Consumer Price Index rose 0.1% (1.8% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report.

Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers rose 0.2% (2.7% annualized rate) in December. The CPI less food and energy rose 0.1% (1.4% annualized rate) on a seasonally adjusted basis.

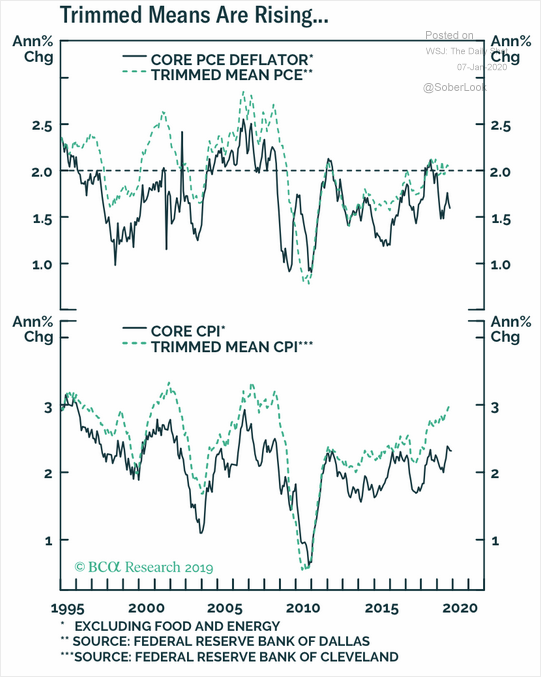

But, there are signs of underlying pressures still:

Advertisement

Which will not be helped by this news, via Bloomie:

Existing tariffs on billions of dollars of Chinese goods coming into the U.S. are likely to stay in place until after the American presidential election, and any move to reduce them will hinge on Beijing’s compliance with the terms of a phase-one trade accord, people familiar with the matter said.

The two sides have an understanding that no sooner than 10 months after the signing of the agreement at the White House Wednesday, the U.S. will review progress and potentially trim tariffs now in place on A$521.35 billion of imports from China, the people said, declining to be identified because the matter is private.

Nothing much has changed over the holiday period. The US is still the growth and inflation leader. The global reflation hope embedded in stock markets is still mostly fantasy. Europe is still struggling greatly and China is still slowing.

Advertisement

I still see only a weak global rebound this year as the damage to Chinese globalisation deepens, Europe only crawls out of virtual recession and the US plods on.

There may be slight growth convergence ahead but I can’t see the US dollar falling far enough to support a fulsome reflation in the fundamentals. The Fed isn’t going to cut unless the stocks bear returns while there is more work for the ECB and PBOC ahead.

With the bushfires charring Australia’s already stalled economy, guaranteeing that Australia sits out what good news there is, leaving the RBA little choice but to keep easing, the AUD can’t get far and the odds favour a reversal down in due course.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

{kind=link}