DXY is back with a safe haven rush:

The Australian dollar was destroyed over the past two days:

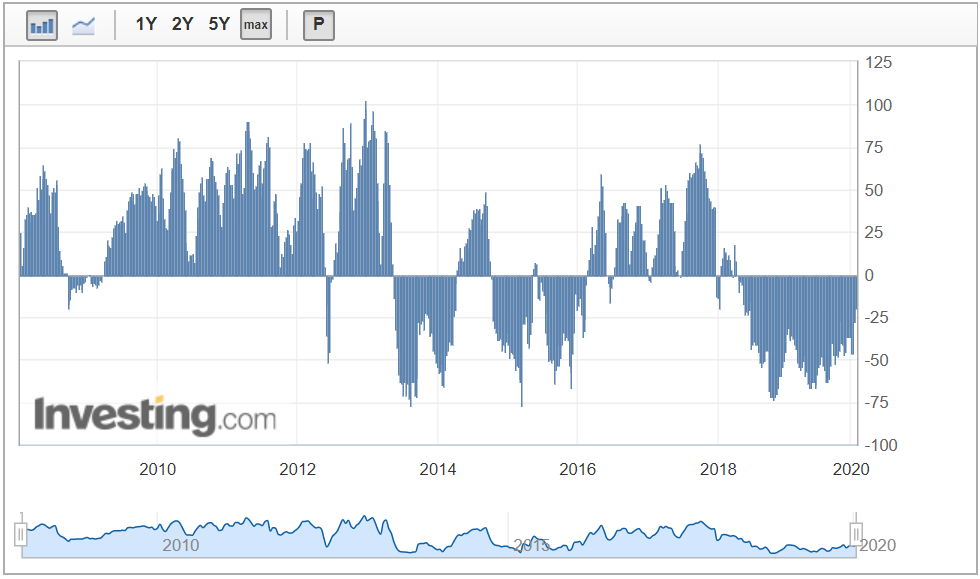

CFTC speculative positions had just moved to their least bearish in two years at -19k. Room now for big downside:

Gold is liking it despite DXY:

Oil is in deep trouble:

So are metals:

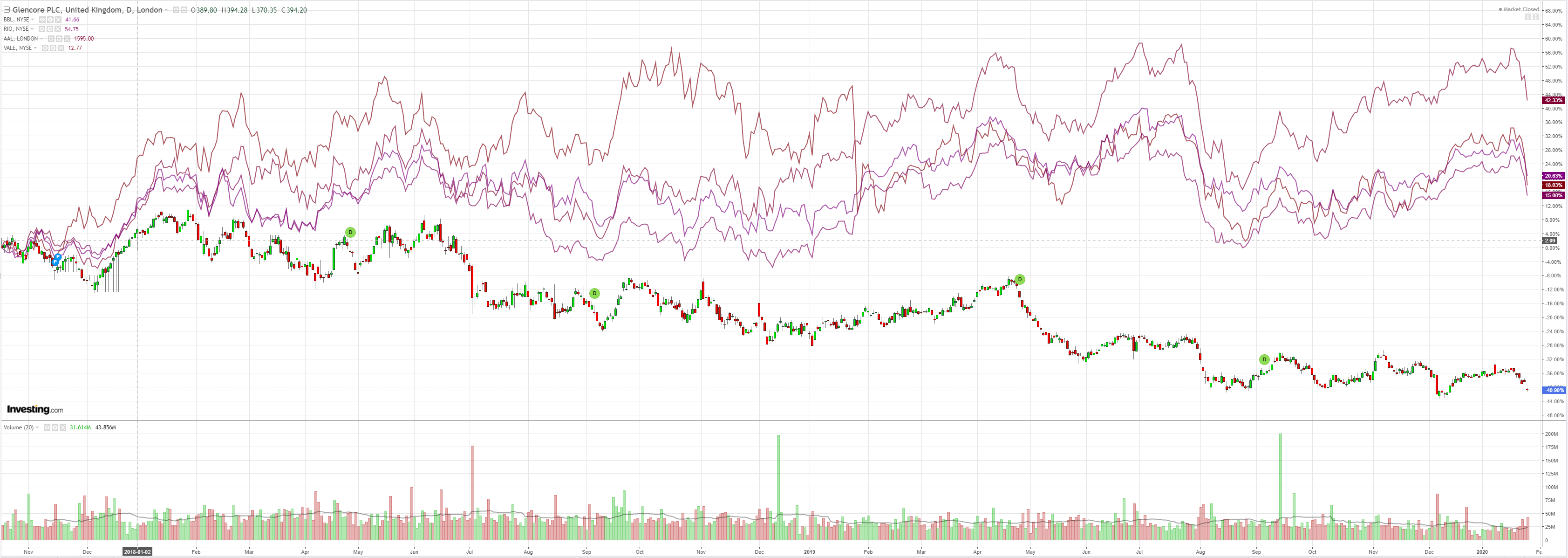

Big miners tumbled but not enough:

EM stocks gapped lower:

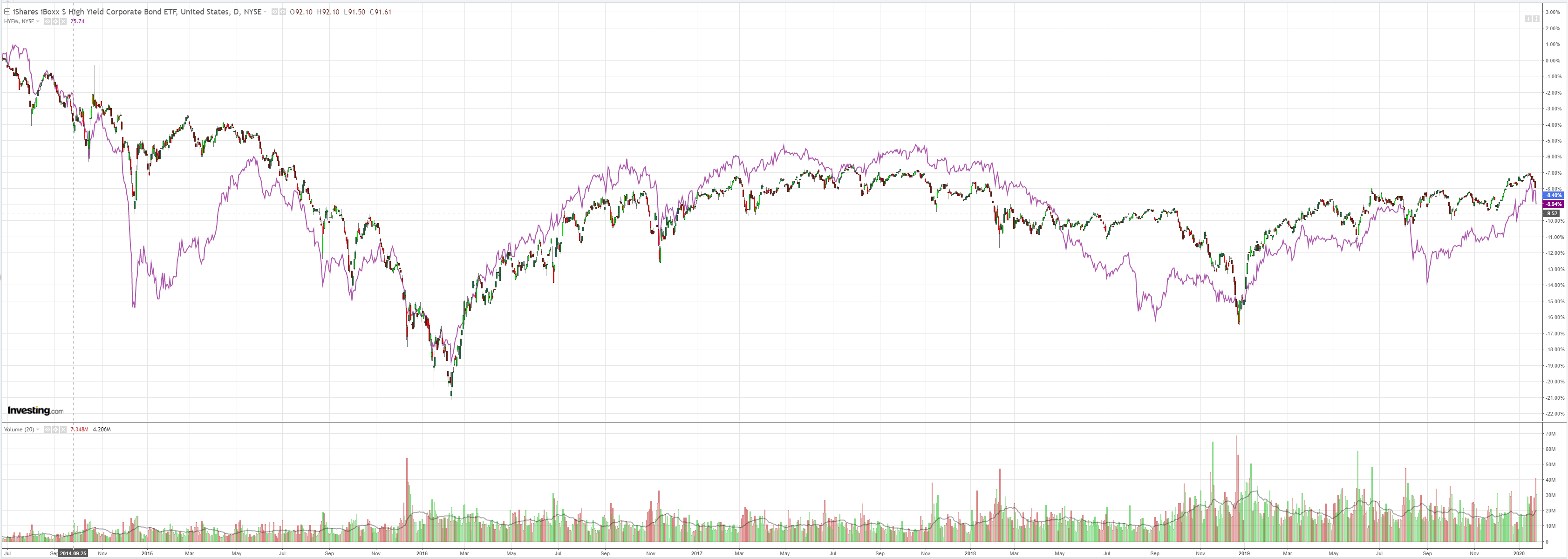

Junk rolled:

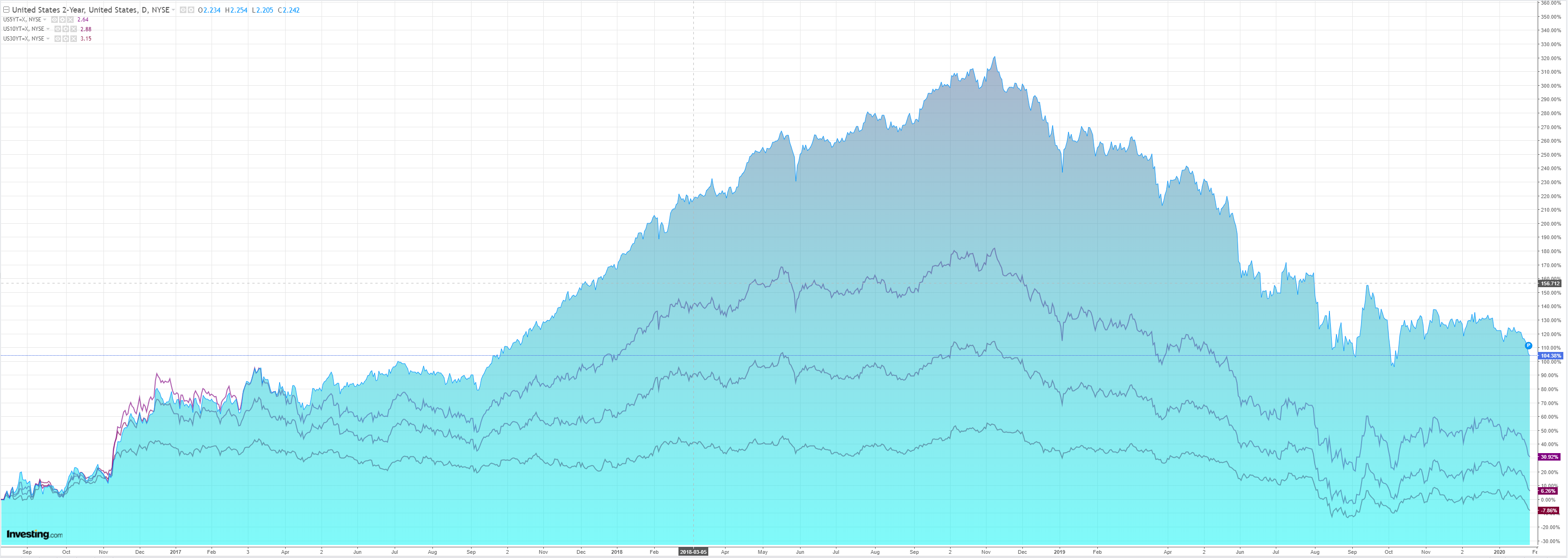

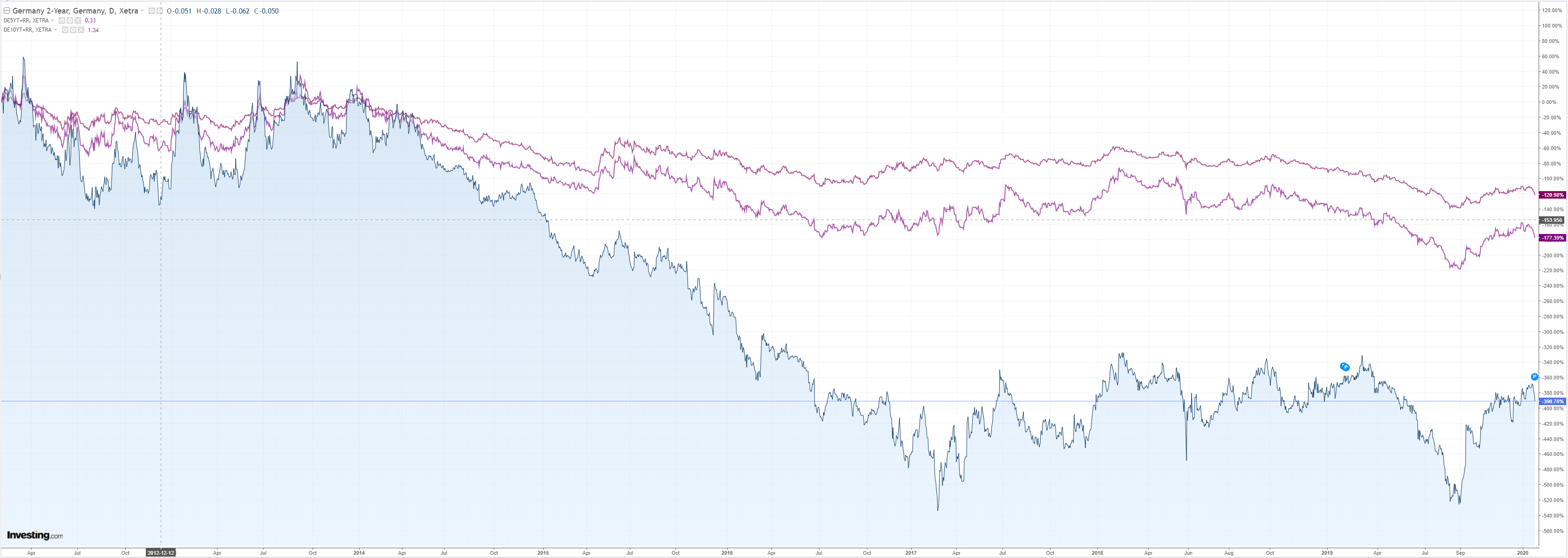

Treasuries roared:

And bunds:

Aussie bonds were afire:

As stocks took sick:

Westpac has the data wrap:

Event Wrap

US new home sales fell 0.4% in Dec, vs expectations of +1,5%, and Nov was revised lower from +1.3% to -1.1%. Dallas Fed’s manufacturing survey beat depressed expectations (+0-.2 vs -2.0).

Germany’s IFO business confidence disappointed expectations at 95.9 vs 97.0.

The coronavirus epidemic has so far resulted in 82 deaths and 2700 confirmed cases in China. Outside China, 50 cases have been confirmed, with at least 5 in the US.

Event Outlook

The Australian December NAB business survey is due today. In November, conditions were soft and confidence was weak.

In the US, December durable goods orders will again highlight persistent weakness in business investment. Also out today are S&P Case-Shiller house prices for November as well as January’s consumer confidence and Richmond Fed surveys. Of late, house price gains have moderated to a subdued pace below wage growth, while consumer confidence has continued to print above average.

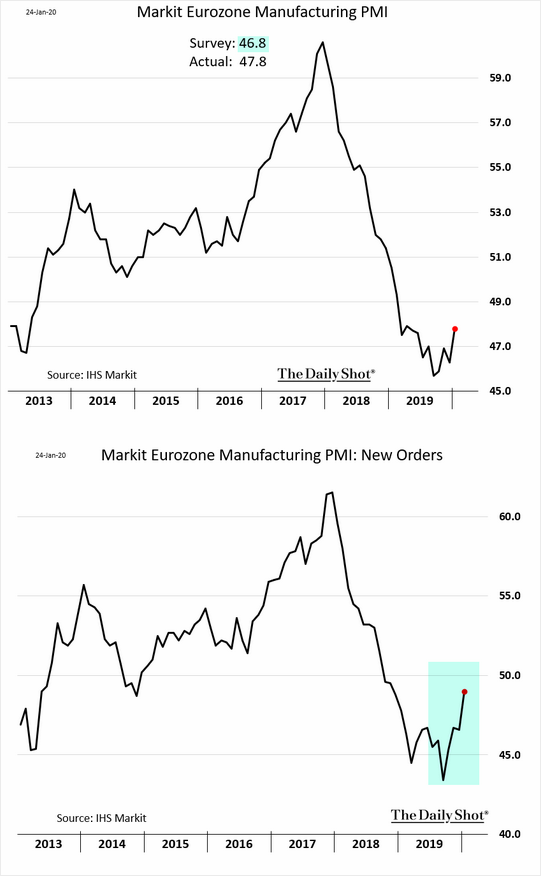

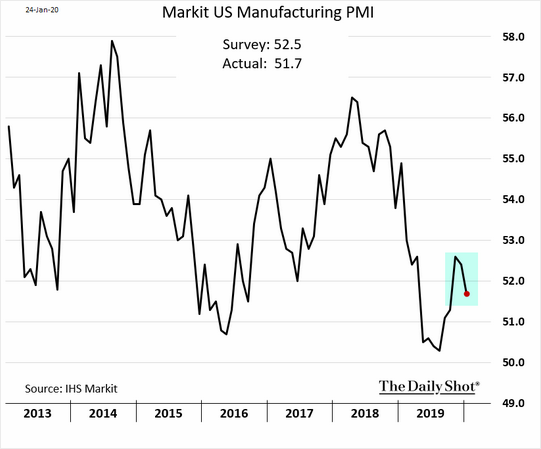

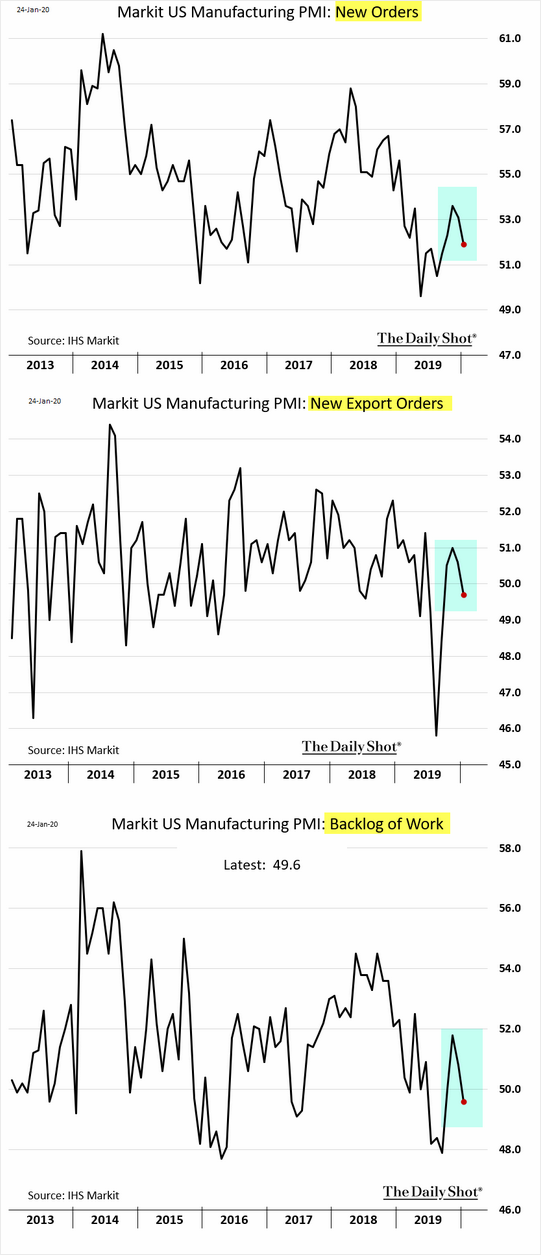

PMIs favoured Europe over the US:

But none of that matters now. Coronavirus is not priced into anything given it has suddnely morphed into a clear threat for global recession.

The destruction of the Australian dollar has only just begun.