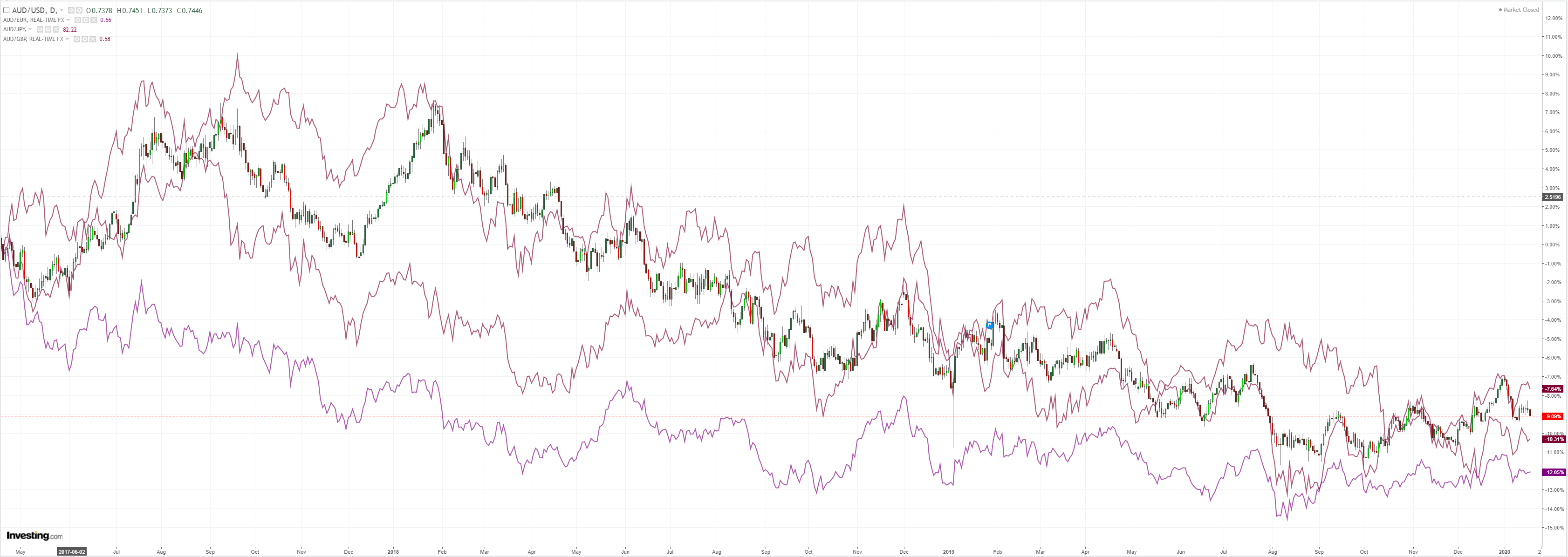

The Australian dollar was belted across the board:

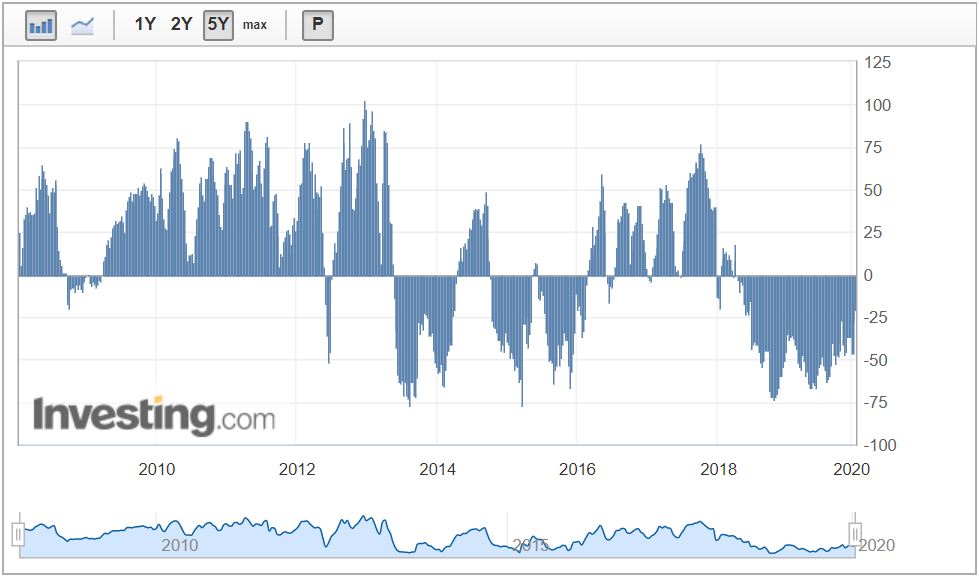

CFTC shorts have cleared to their lowest level in nearly two years at -20k, freeing up downside:

Advertisement

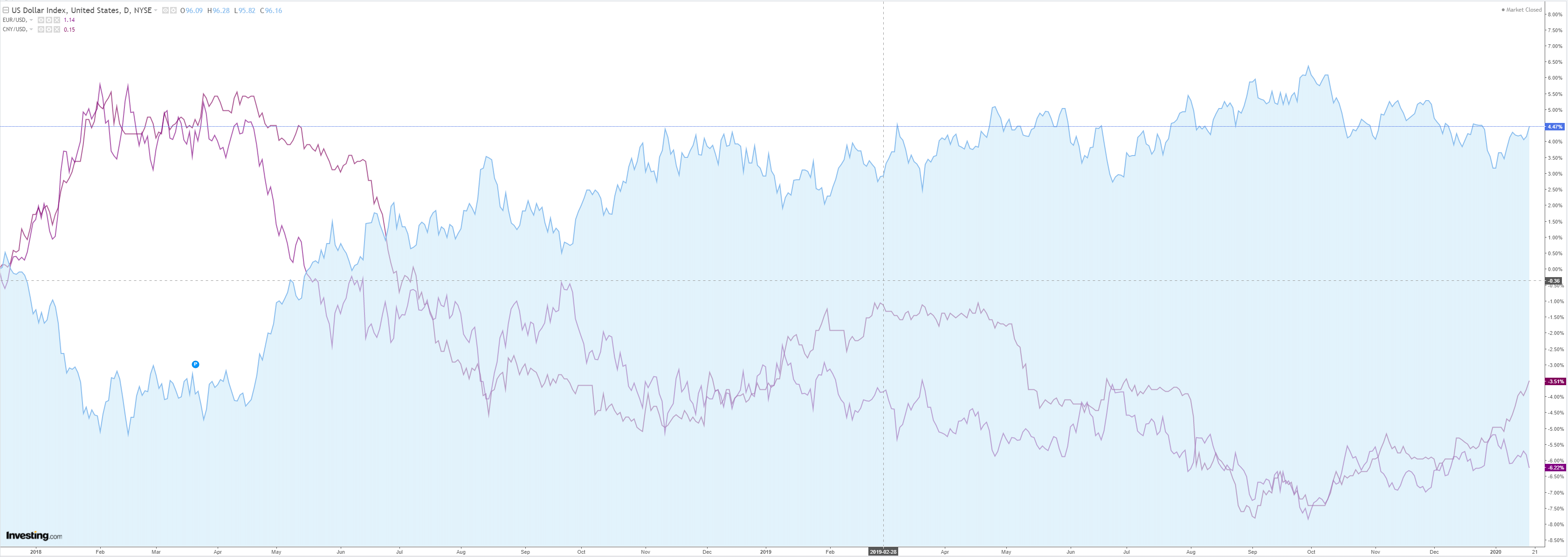

Gold eked out gains despite DXY:

Same with oil:

And metals:

Advertisement

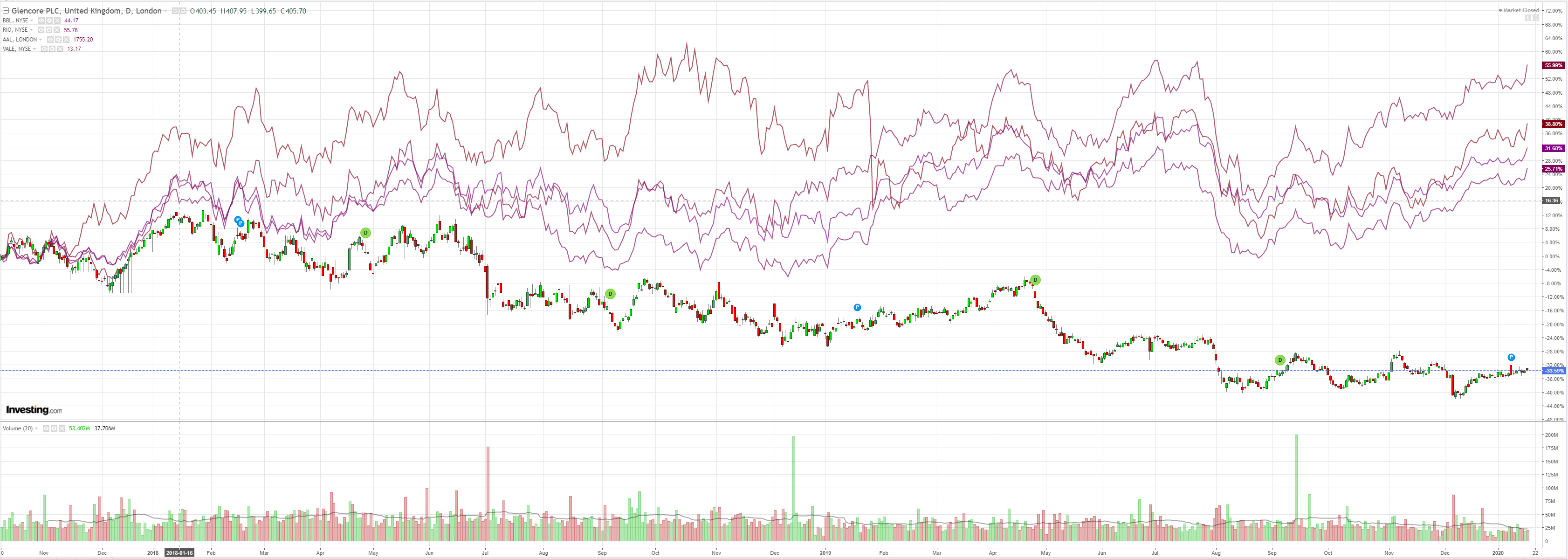

Miners are iron ore incarnate:

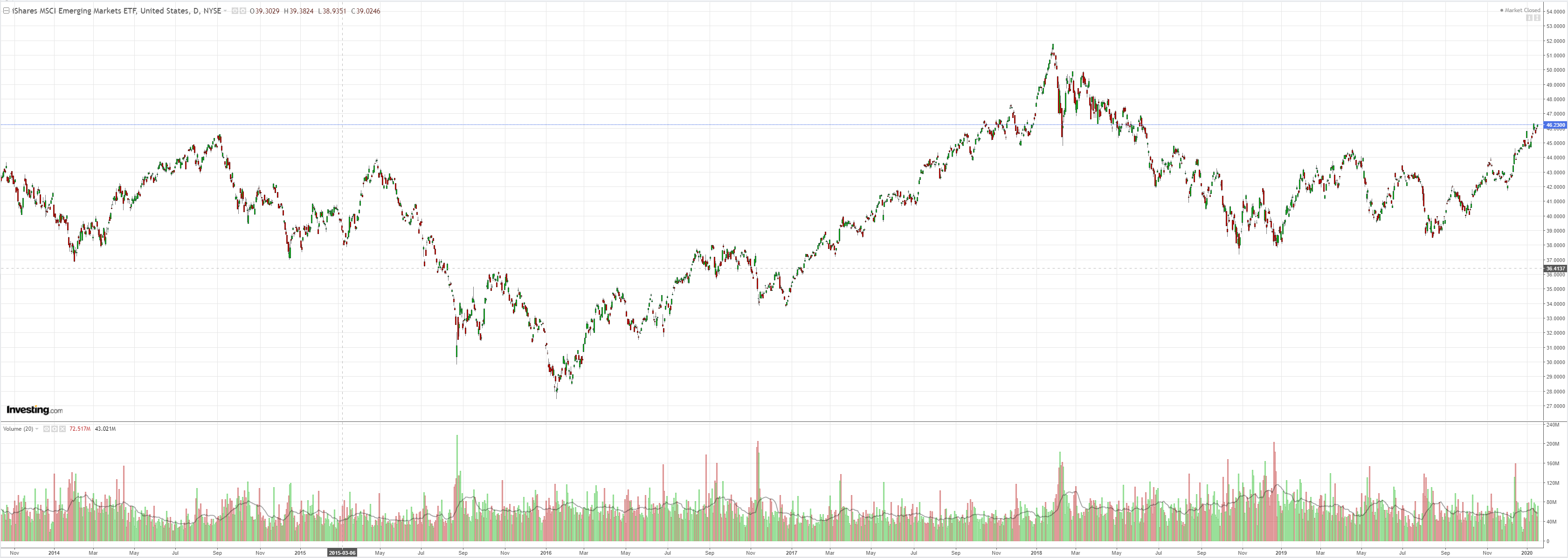

EM stocks flew:

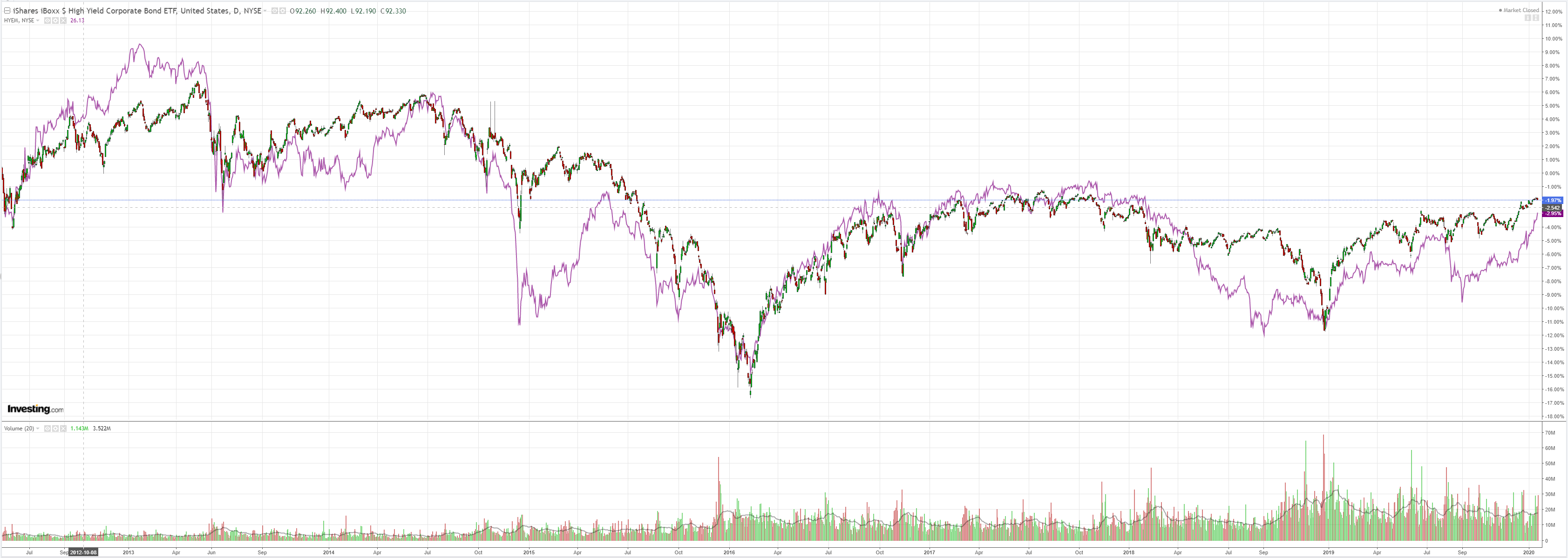

It’s a global junk party:

Advertisement

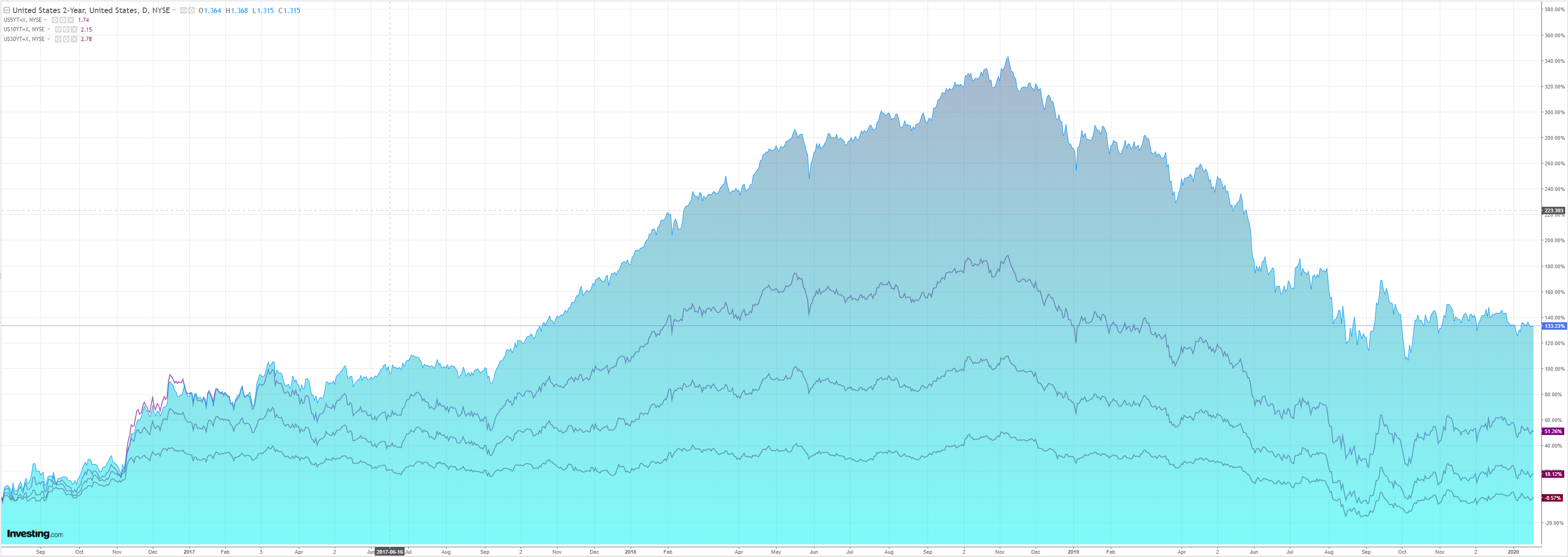

Treasuries steepened a little:

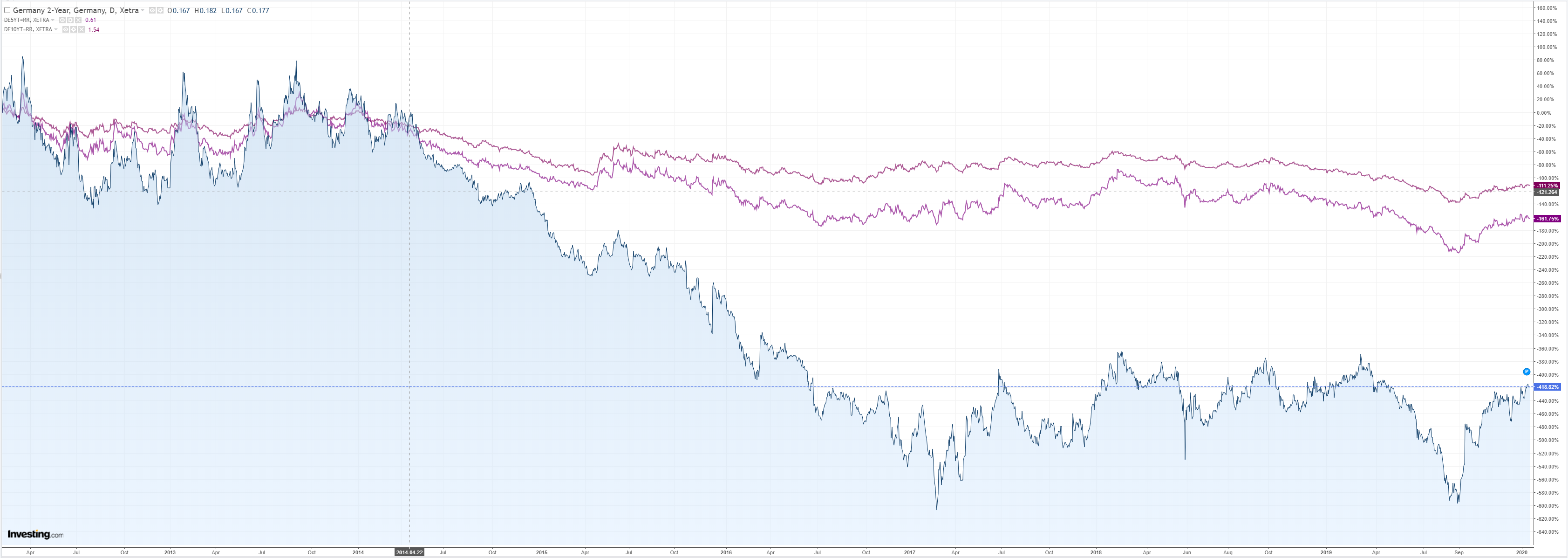

Not bunds:

Or Aussie bonds:

Advertisement

Stocks wow:

Data on the evening was focussed on the US and was mixed. JOLTS fell but remains trong. Industrial production is falling.

But both are going to firm ahead as tearaway US housing indicates a brighter future:

Advertisement

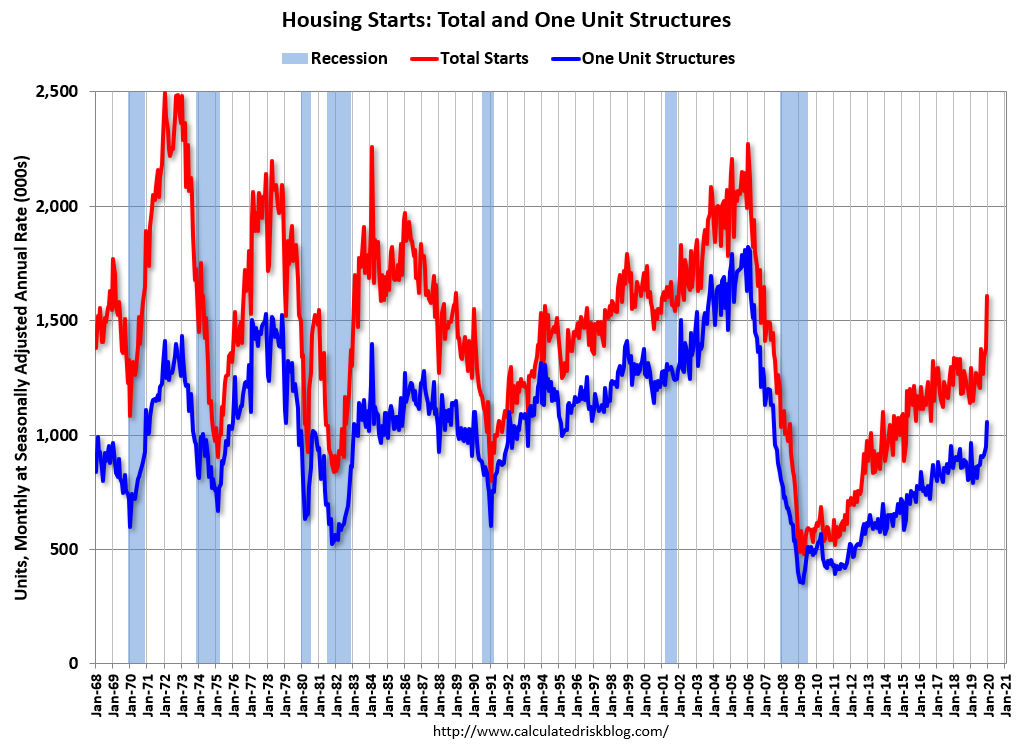

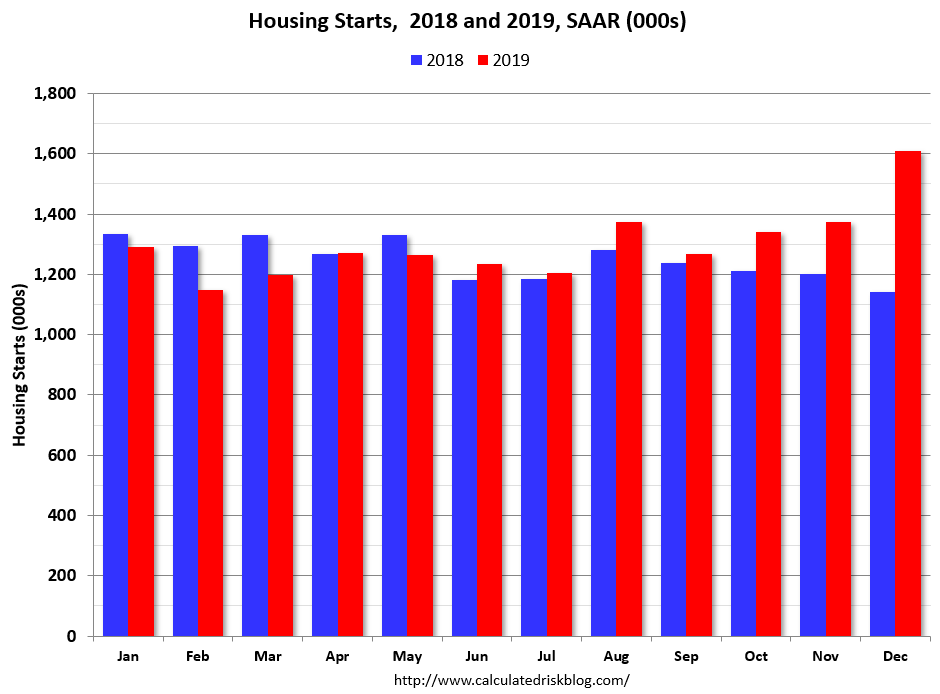

Housing Starts:

Privately‐owned housing starts in December were at a seasonally adjusted annual rate of 1,608,000. This is 16.9 percent above the revised November estimate of 1,375,000 and is 40.8 percent above the December 2018 rate of 1,142,000. Single‐family housing starts in December were at a rate of 1,055,000; this is 11.2 percent above the revised November figure of 949,000. The December rate for units in buildings with five units or more was 536,000.

An estimated 1,289,800 housing units were started in 2019. This is 3.2 percent above the 2018 figure of 1,249,900.

Building Permits:

Privately‐owned housing units authorized by building permits in December were at a seasonally adjusted annual rate of 1,416,000. This is 3.9 percent below the revised November rate of 1,474,000, but is 5.8 percent above the December 2018 rate of 1,339,000. Single‐family authorizations in December were at a rate of 916,000; this is 0.5 percent below the revised November figure of 921,000. Authorizations of units in buildings with five units or more were at a rate of 458,000 in December.

An estimated 1,368,800 housing units were authorized by building permits in 2019. This is 3.9 percent above the 2018 figure of 1,317,900.

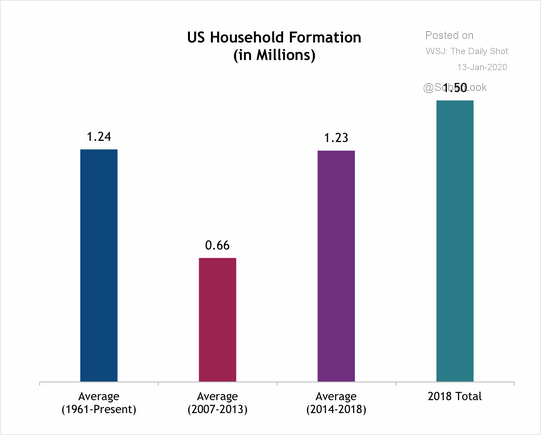

Finally, a decade on, the US housing market has returned to normal level of construction. And there is more ahead. Household formation is rebounding:

Advertisement

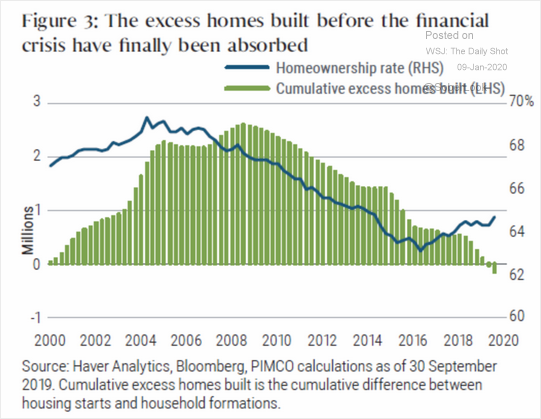

And the property glut is finally cleared:

The foundations of US households are strong. There’s more relief coming as we head into the Presidential election year. Either via Trump tax cuts or student debt write-offs from Democrats. And the consensus on tarrifs and the war on China ensures a greater proportion of the activity will remain at home than in the last several cycles, albeit also driving weaker global growth.

The comparison with Australia is stark where massive household debt is only at the beginning of a decade long shakeout as China goes ex-growth and the commodity income is crushed. Household formation is in trouble as income falls. An excess of property will prove very difficult to shift as these factors play out, notwithstanding the population ponzi.

Advertisement

Short, medium and long there is no upside to owning the AUD over the USD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.