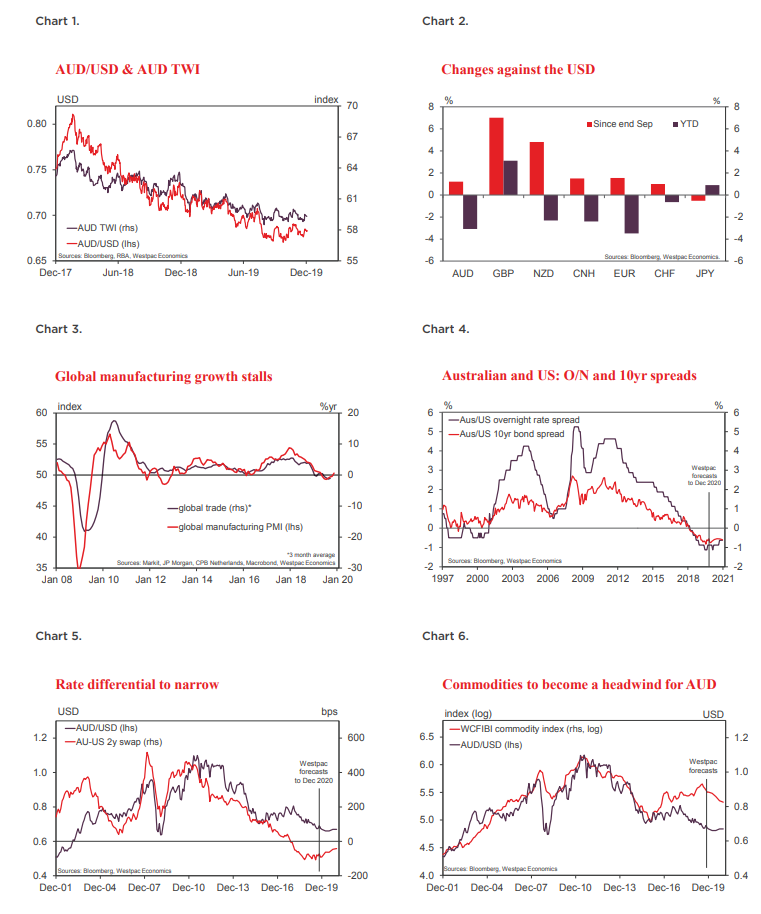

At the time of our November Market Outlook the AUD had lifted from USD0.675 to USD 0.698.

Over the last month it has traded down to as low as USD0.676 and back to USD0.683. Eff ectively the AUD has traded in the USD0.67 to USD0.70 range since late July.

Westpac last changed its AUD call on July 24 when we forecast the AUD would drift down from USD0.695 at the time to USD0.66 by the fi rst half of 2020. That was predicated on a further RBA rate cut in February 2020; ongoing diffi cult global environment which would favour ‘risk–off ’ currencies; and the possible use of unconventional monetary policies by the RBA.

On November 27 Westpac further revised down its forecast for the RBA cash rate with an additional cut to 0.25% by June next year. We also noted the likely adoption of Quantitative

Easing by the RBA after the last rate cut in June. That would be in the form of $2–3 billion of regular monthly purchases of Commonwealth government bonds.

With the RBA making it clear that 0.25% is the eff ective lower bound for the cash rate and given our view that the FOMC will be easing policy during 2020, the risk for the RBA is unwelcome upward pressure on the AUD once it appears that the RBA is ‘done’.

It will be at this point that it will have to adopt an open ended asset purchase policy. However the assets are likely to be limited to Commonwealth Government Securities or semi government securities denominated in AUD.

A policy of unsterilised purchases of foreign currency government bonds, which would be associated with direct sales of AUD is unlikely to be adopted by the RBA, despite it’s likely eff ective impact on AUD. The label ‘currency manipulator’ which is now being levelled at some countries by the US administration and the associated tariff response is something the RBA would avoid.

Lower interest rates and open ended QE can be expected to assert some downward pressure on AUD. But the USD0.66 target for next year is only likely to be achieved if the global environment favours ‘risk off ’ currencies, particularly the Japanese Yen; Swiss Franc; and to a lesser extent, the

USD.

The ‘big four’ issues which, we believe, will be consistent with ‘risk off ’ in 2020 are: a larger than expected slowdown in China; ongoing uncertainty around international trade; volatility in confi dence emanating from a particularly bitter US Presidential campaign; and a slowdown in the US economy.

While the US authorities are likely to respond with rate cuts from the Federal Reserve, and the Chinese authorities will embrace both fi scal and monetary policy measures, these policy responses will be applied carefully to manage the slowdown rather than provide an aggressive boost.

In this regard the approach of the Chinese will be of most signifi cance. China is a student of history. It is acutely aware of the economic disaster that befell Japan after the 1980s when ‘bullied’ by the US to accept the Plaza Accord whereby the Japanese Yen eventually appreciated (between 1985 and 1987) by around 50% relative to the US dollar.

That action constituted a major external shock to the Japanese economy. In response the Japanese authorities sharply boosted liquidity in the domestic economy which fuelled the huge asset bubbles that eventually burst and condemned Japan to ‘lost generations’. China will be mindful not to accede to US demands around its trade surplus with the US and will be careful not to overly boost domestic liquidity in response to the shock.

That means one can expect China to play ‘hardball’ with US trade demands and be careful to avoid over stimulatory liquidity policies.

Bottom line: it seems 2020 will be ‘risk off ’ with markets focussed on slow growth in both China and the US, trade tensions and political uncertainty in the US.

That seems about right to me as the base case. I’m a little more buillish on the US as the labour market supports spending and the fiscal cliff passes, along with the traditional spendathon of the Presidential election, plus a little lift in global activity.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.