Via the excellent George Theranou comes the fruition of Recessionberg:

Q3 GDP slowed to 0.4% q/q after 0.6%; but edged up to 1.7% y/y after 1.6%

Q3 real GDP unexpectedly slowed to just 0.4% q/q (UBS 0.5%; mkt 0.5%), albeit after an upwardly revised 0.6% in Q2 (was 0.5%). Hence, the y/y ticked up to 1.7% (UBS: 1.6%, mkt: 1.7%) – after Q2 was revised up to 1.6% (was 1.4%) – albeit still the ~weakest since the GFC, well below ‘trend’ of ~2½%, & ~flat in per capita terms.

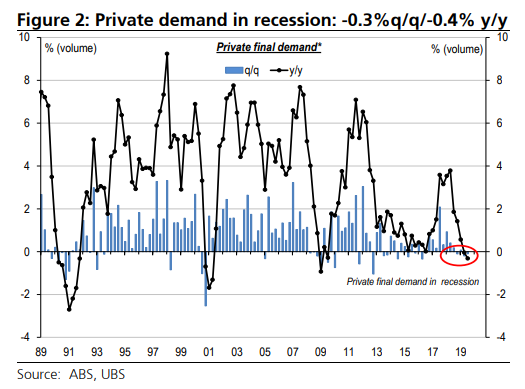

Domestic demand weakened to 0.2% q/q & a 4-year low 0.9% y/y; despite booming public demand (1.7%, 5.2%) adding a very large 0.4%pts & 1.2% y/y to GDP; as public consumption lifted (0.9%, 6.0%), & public investment rebounded sharply (5.4%, 2.1%). Worryingly, private demand fell into recession (-0.3%, -0.4%). Within this, business investment contracted again (-2.1%, -1.7%); as mining relapsed (-7.8%) but non-mining bounced (1.2%). Consumption (0.1%, 1.2%) slumped to the ~worst since the GFC. The housing downturn got worse (-1.7%, -9.6%). Elsewhere, inventories ~steadied (0.1%pts, -0.3%pts); but net exports added solidly (0.2%pts, 1.1%pts).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.