1. We have a modest ASX 200 target of 7000. At an aggregate level, income, rather than capital growth will likely be the driver of returns.

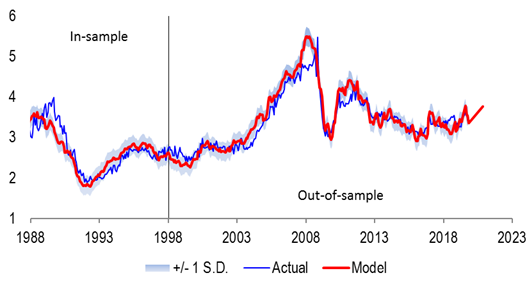

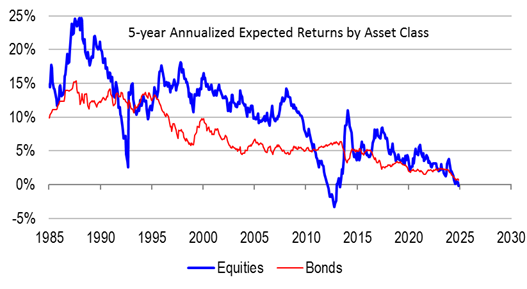

2. We see earnings recovery, but multiple compression. IBES Consensus numbers point to roughly 6% earnings per share (EPS) growth over the next year, with the market currently trading on a forward price-to-earnings (PE) multiple of 17.3x. We think that the earnings growth forecast is quite easily achievable on cyclical recovery in Australia and abroad. But we also think that the market is expensive, trading on a through-the-cycle multiple of 28x. At this level of valuation, equities are priced for 4% annualized returns over the next 10 years, and slightly negative returns over the next 5 years. In contrast, bonds are offering 1% annualized returns over the next 10 years, and 0.7% annualized returns over the next 5 years. On a 5-year horizon, the equity risk premium is effectively negative, consistent with upcoming multiple compression.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.