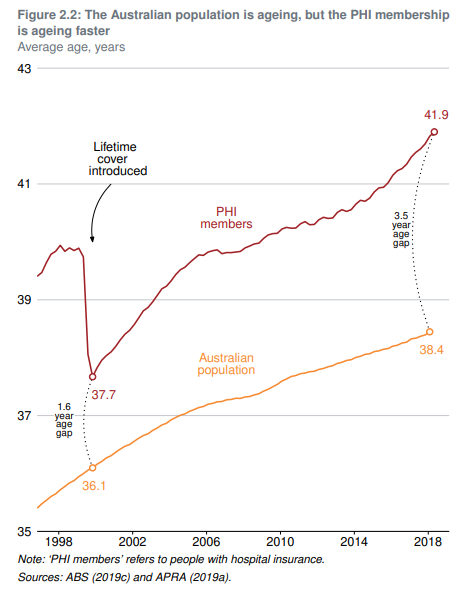

The Grattan Institute has released another report warning that Australia’s private health insurance industry is facing a “demographic death spiral” from an exodus of younger, healthier members, which requires urgent action to resolve.

Below is the report summary, along with key graphics:

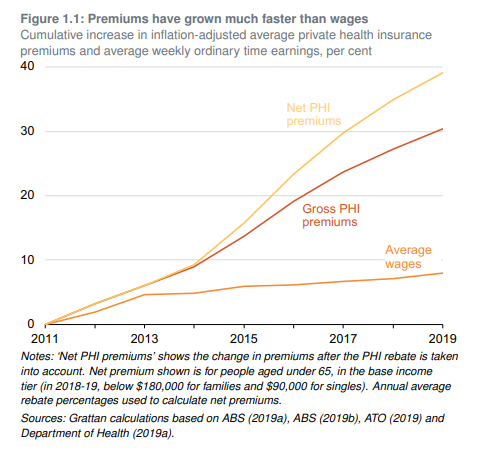

The Australian private hospital insurance system is unsustainable in its present form. The system faces a death spiral – younger and healthier consumers get a bad deal, so they’re dropping their insurance, which means premiums need to rise, so even more young and healthy people drop out, and the cycle continues.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.