NAB’s new business survey is out and sucks:

Overall, the business survey is consistent with ongoing weakness in GDP growth (especially private demand) and suggests there has been little improvement in Q4 for GDP. With conditions below average and confidence also weak, there is a risk that employment growth slows and that investment will remain weak despite spill-over demand from public sector spending and a stabilisation in mining.

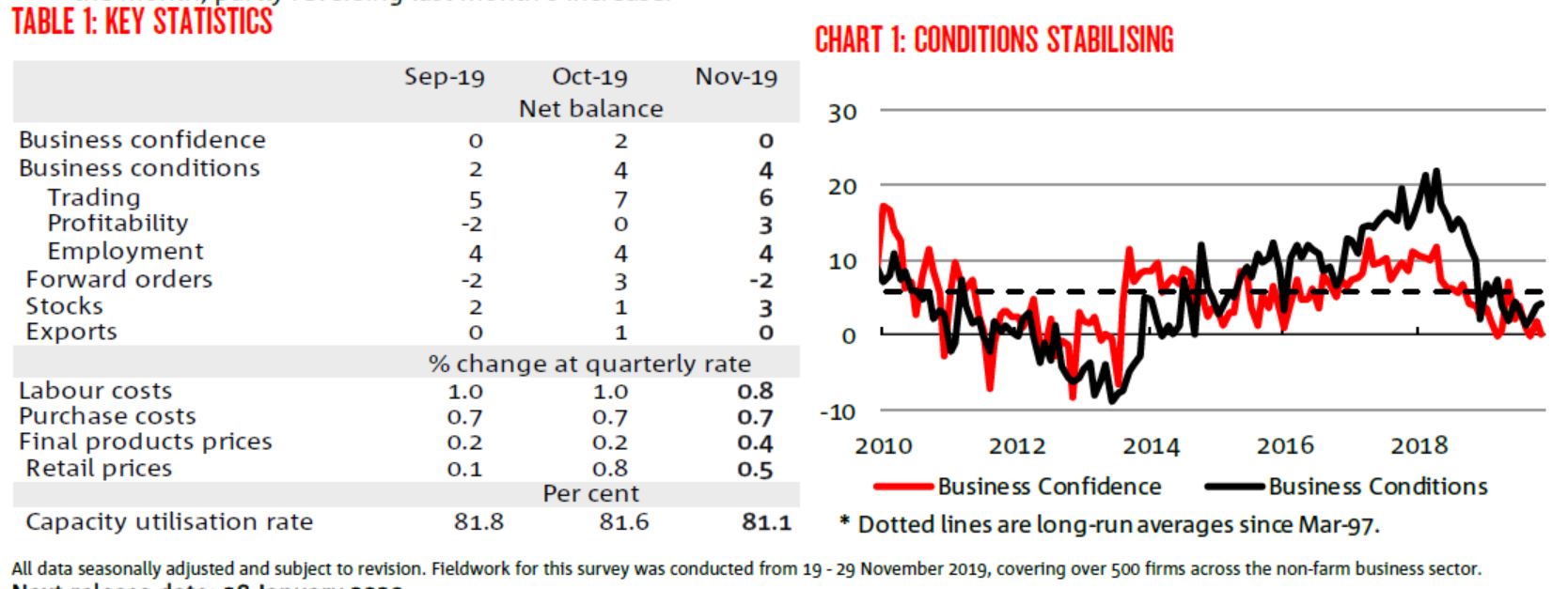

HIGHLIGHTS

• How confident are businesses? Confidence fell 2pts in November to 0 index points – unwinding last month’s increase.

• How did business conditions fare? Conditions were unchanged in the month at +4 index points.

• What components contributed to the result? A pickup in profitability was partially offset by a small fall in trading conditions in the month. The employment index was unchanged – and is the only component currently above average.

• What is the survey signalling for jobs growth? Based on historical relationships, the survey suggests that employment will rise around 18k per month over the next 6 months.

• Which industries are driving conditions? Mining, construction and transport & utilities declined in the month, while rec & personal services edged lower. These declines were offset by an increase in the remaining industries, led by manufacturing; wholesale was flat. In trend terms, conditions are most favourable in the services industries and weakest in retail, wholesale and transport & utilities. Manufacturing and construction rank in the middle.

• Which industries are most confident? Confidence decreased in all industries in the month, except for retail and wholesale which increased slightly. In trend terms, confidence is highest in construction and retail, with wholesale weakest.

• Where are we seeing the best conditions by state? Conditions increased in Vic and Tas in the month and were lower across the other states, with notable falls in NSW and SA. Overall, in trend terms, conditions remain most favourable in NSW and Tas. Qld is weakest and the only state to record negative conditions.

• What is confidence like across the states? Confidence declined across all states except Vic which edged higher. In trend terms, confidence is highest in Tas and WA and weakest in Vic and Qld.

• Are leading indicators suggesting further improvement? Forward indicators softened in the month, after showing some improvement in recent months. Forward orders declined and are again negative, while capacity utilisation is now back around its long-run average.

• What does the survey suggest about inflation and wages? Overall, surveyed price measures suggest ongoing below-target inflation but have shown some building pressure in recent months. In the month, labour costs growth edged lower while other input costs growth was flat. Final products price growth increased, notwithstanding a decline in retail prices growth in the month, partly reversing last month’s increase.

Meh, this was another weak survey. The improvements were all soft indicators and forward indicators weakened. Employment is too low to create enough jobs: