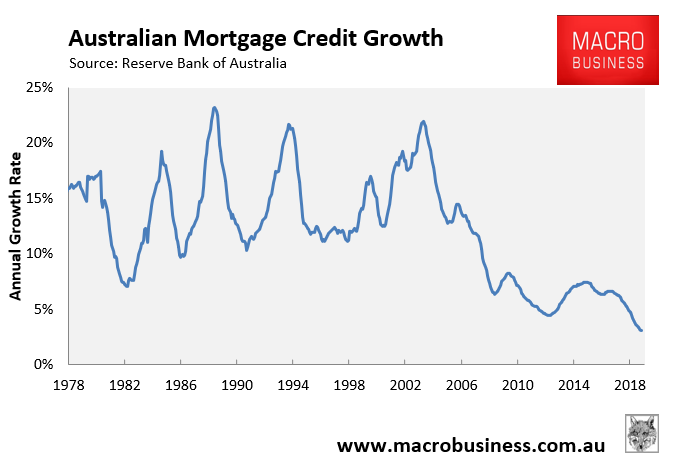

Friday’s mortgage credit data from the RBA revealed that the stock of mortgage debt outstanding grew by only 3.0% in the year to October 2019 – the lowest growth on record:

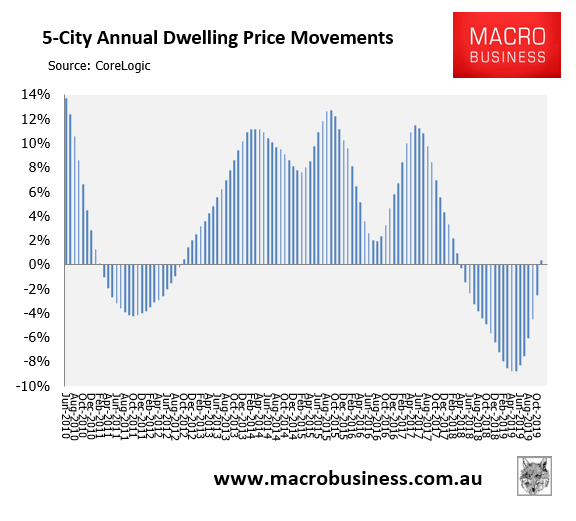

At the same time, yesterday’s dwelling value results for November, released by CoreLogic, continued to rebound, registering 0.4% annual growth:

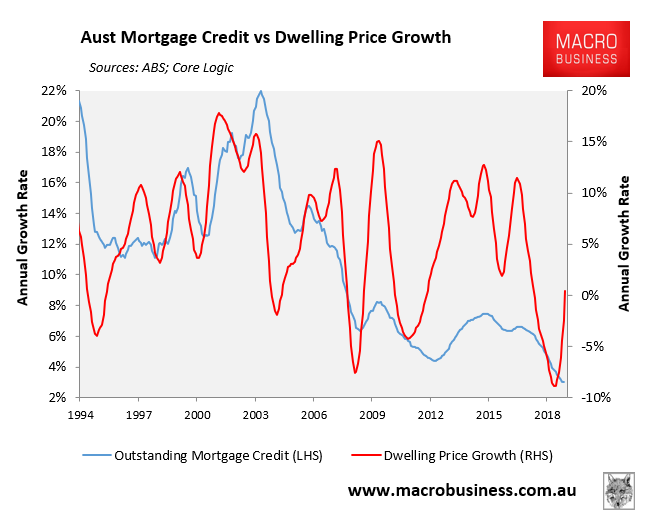

Logically, the stock of mortgage credit should track dwelling value growth, since all buyers borrow to buy property. However, both series are now showing record divergence:

As noted previously, this disconnect is easily explained, since mortgage credit growth measures two separate things: 1) the addition to the mortgage stock from new mortgages taken out by borrowers (increases the stock of debt outstanding); and 2) the repayment of mortgage debt by existing borrowers (reduces mortgage debt).

Only the first point – new mortgages created – actually impacts house prices. The second – mortgage repayments by existing borrowers – does not reflect new housing demand and does not impact prices.

When interest rates are at record lows – as they are currently – we are likely to see mortgage repayments rise, which lowers mortgage credit growth, but doesn’t actually impact house prices.

Similarly, many investors have been forced to switch from interest-only mortgages to principal and interest, meaning they are now lowering the stock of mortgage debt outstanding (other things equal) without adding to housing demand.

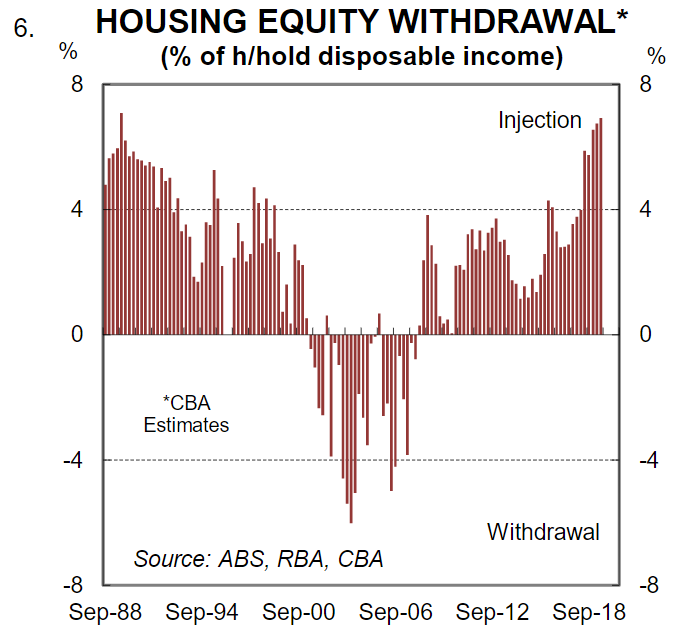

Gareth Aird, senior economist at CBA, has made similar observations, noting that the rate of housing equity injection presently sits at a 30-year high, reflecting higher repayments:

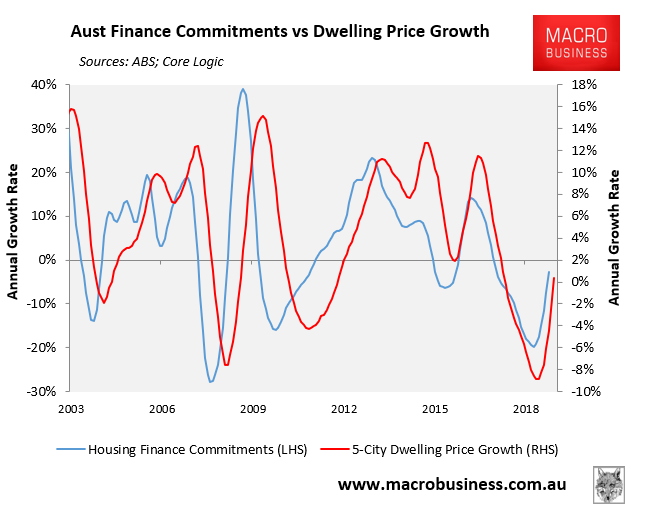

For these reasons, MB prefers to look at the value of housing finance commitments (excluding refinancings), which only measures new mortgages and leaves out the noise generated by repayments:

As you can see, the correlation between housing finance and house prices has historically very strong, with housing finance typically leading prices.

However, because of the long lags in receiving housing finance data, we usually find out that the market has turned after CoreLogic’s daily index has already been reported.

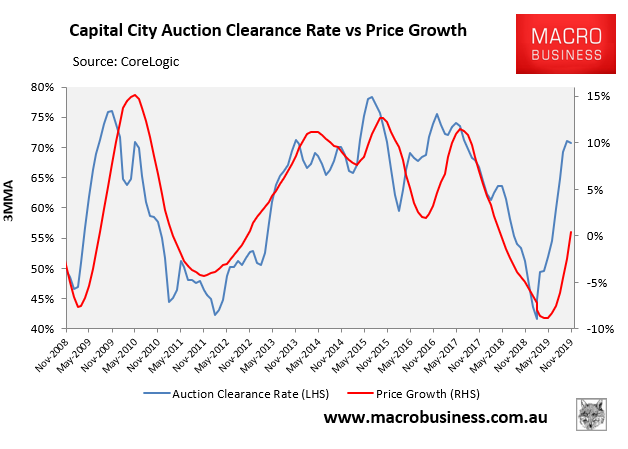

Accordingly, we also look at auction clearance rates, since they provide a more timely indicator and also show a strong correlation with dwelling prices: