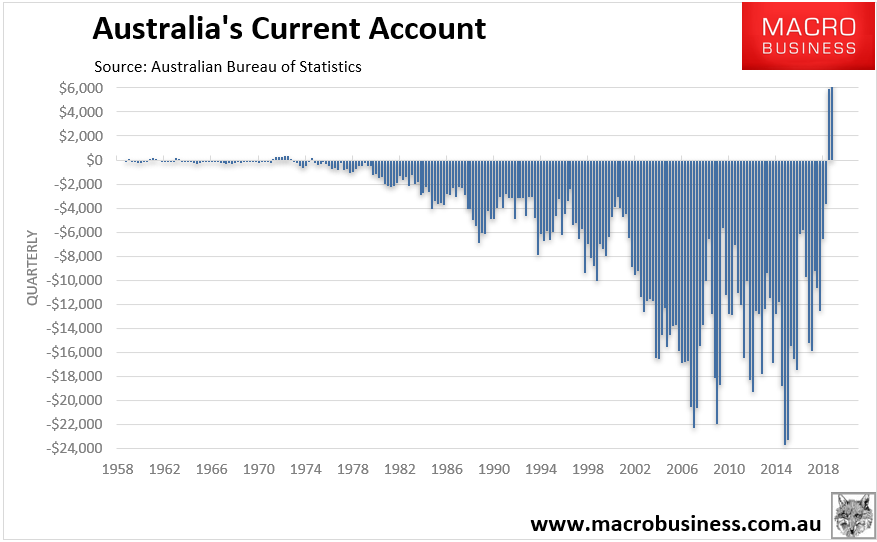

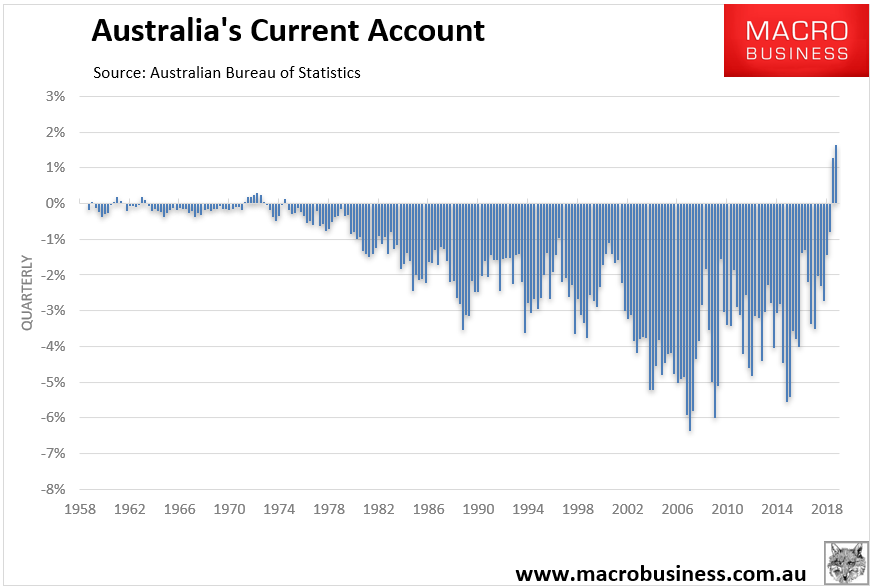

The ABS released September QTR balance of payments yesterday and it threw up the largest quarterly current account surplus on record in both dollar and percentage of GDP terms:

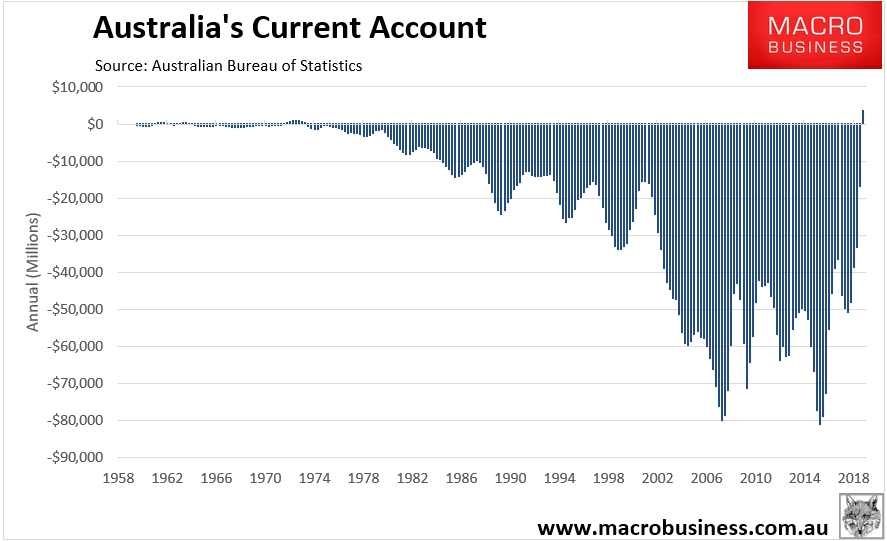

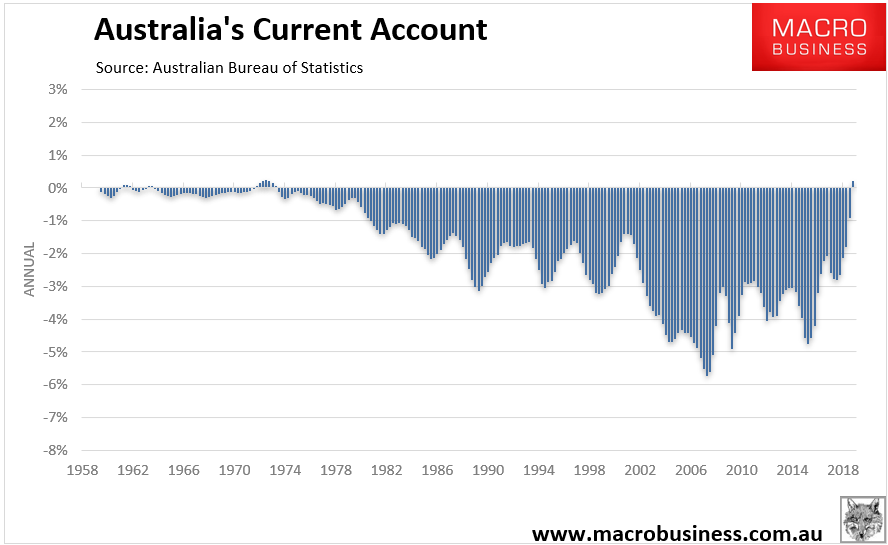

Even the annual figure turned positive:

Advertisement

Though is less impressive (so far) in annual terms:

It will likely also set recrods in the December quarter though the headwinds are building as house prices will boost consumption at the margin and the terms of trade shock will begin in the next quarter:

Preliminary estimates for November indicate that the index decreased by 3.5 per cent (on a monthly average basis) in SDR terms, after decreasing by 6.6 per cent in October (revised). The non-rural subindex decreased in the month, while the rural and base metals subindices increased. In Australian dollar terms, the index decreased by 3.7 per cent in November.

Over the past year, the index has decreased by 5.0 per cent in SDR terms, led by lower coal, LNG and alumina prices. The index has increased by 0.2 per cent in Australian dollar terms.

Advertisement

I expect the current account surplus will last about as long as the last one!

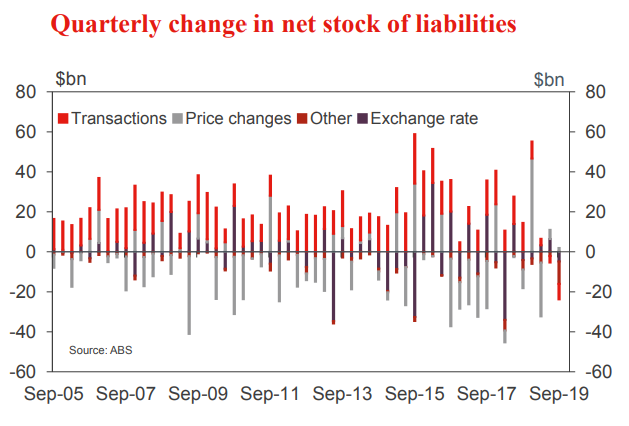

Westpac also points out some interesting developments:

In contrast to foreign investors’ enduring interest in Australia, Australian firms’ have continued to hold back from expanding offshore. Through both 2018 and 2019, foreign investment by Australian firms has been broadly unchanged. Indeed the detail points to a repatriation of capital freed up from asset sales ($5bn in 2018 and $9bn annualised in 2019) which has been offset by other firms reinvesting prior period earnings offshore.

Turning to portfolio investment. Australian firms continue to see little reason to materially increase their use of offshore debt markets (according to the RBA’s bond data). After net issuance of $17bn in the first half of 2015, the outstanding stock was reduced by $15bn between July 2015 and June 2017. Australian non-financial corporates then raised $12bn to June 2018 before the stock was again reduced over the six months to December, circa $6bn. To date in 2019, Australian corporates look to have taken advantage of low global rates and high liquidity, increasing outstanding debt by $10bn ($13bn annualised). With Australian investment growth soft and firms appetite for offshore expansion limited, further sustained gains seem unlikely in the near term.

Foreign investors’ appetite for Australian portfolio debt securities (primary and secondary) has been decidedly stop/start since mid2018. Over the year to June 2018, a $115bn gross inflow was seen.

Since then however, a net outflow of $9bn has been reported amid considerable quarterly volatility. Holdings of government paper and debt securities issued by non-financial and non-bank financial firms have increased, while positions in bank paper have been reduced after previously being built up.

Foreigners’ appetite for Australian equities turned in 2018 after more than a decade of robust inflows. In the past year, demand has been weak, with just $1.1bn in gross inflows. At the same time, Australian investors have continued to expand their foreign portfolio equity assets, with $72bn in gross outflows seen.

That is up from $44bn over the year to September 2018, and $22bn in the year to September 2017.

The point to highlight here is that Australian investors, both institutional and retail, are looking to diversify their asset base by sector and market in search of sustainable, robust returns.

Given Australia’s growth outlook as well as the limited depth of domestic markets, this trend is likely to persist. The potential for the Australian dollar to depreciate further also argues for the allocation of capital to foreign markets.

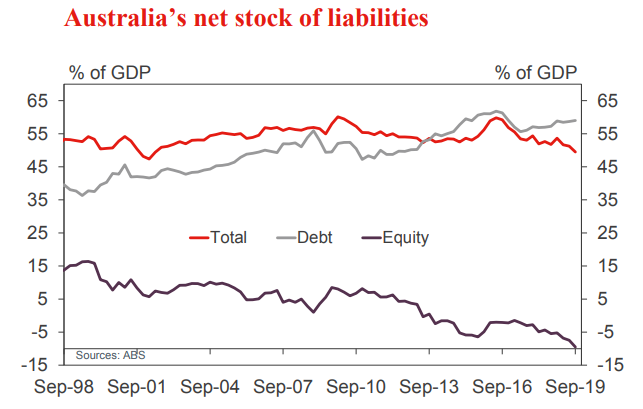

This will get worse as China slows, the terms of trade fall, and the cracks in Australia’s broken economic structure widen.

Advertisement

David Llewellyn-Smith is Chief Strategist at the MB fund and MB Super which is overweight international shares that will benefit from a falling Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.