The greatest capital misallocation in the history of human civilisation continues today with China’s November data dump.

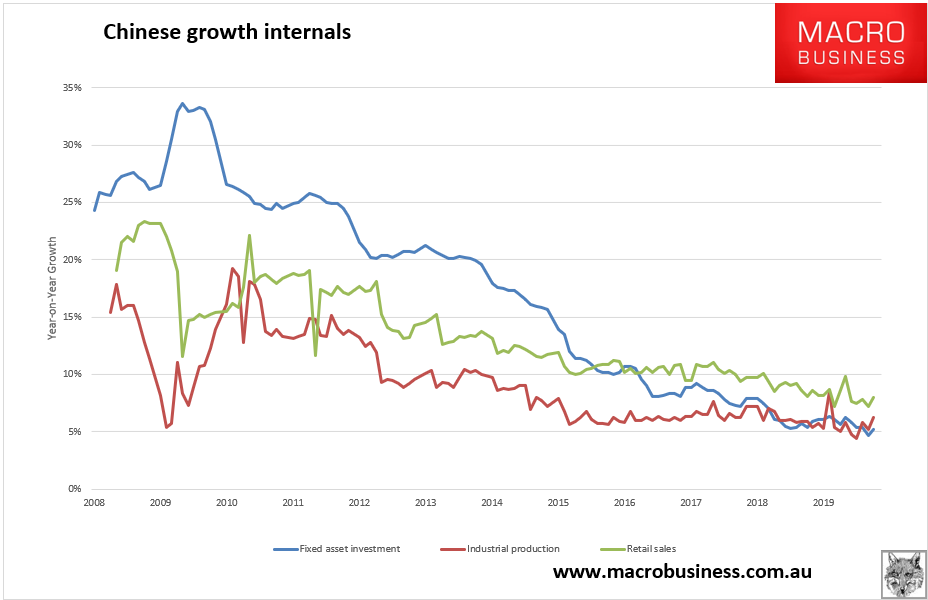

On the surface, all appears well as data beat expectations comfortably. Industrial production was in at 6.2%. Retail sales at 8% and fixed asset investment at 5.2%:

However, I am neither impressed nor comforted. The story of 2019 has been an industrial slump offset by an empty apartment construction boom. There is little to suggest that any lift in manufacturing is enduring but plenty to suggest that realty is on the slide.

Advertisement