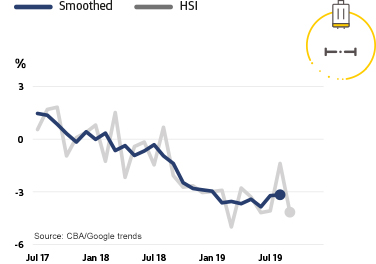

It is logical that the last thing to fall in modern Australia will be house prices! We’ve stopped buying anything else. From CBA’s buying intentions. No food or clothes:

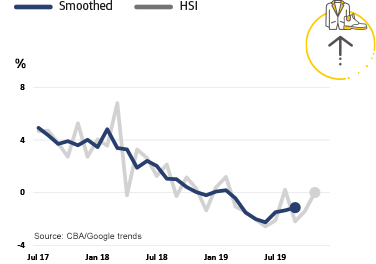

Nor cars:

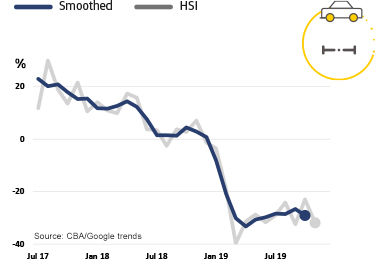

Nor travel:

Advertisement

It is logical that the last thing to fall in modern Australia will be house prices! We’ve stopped buying anything else. From CBA’s buying intentions. No food or clothes:

Nor cars:

Nor travel:

The full text of this article is available to MacroBusiness subscribers